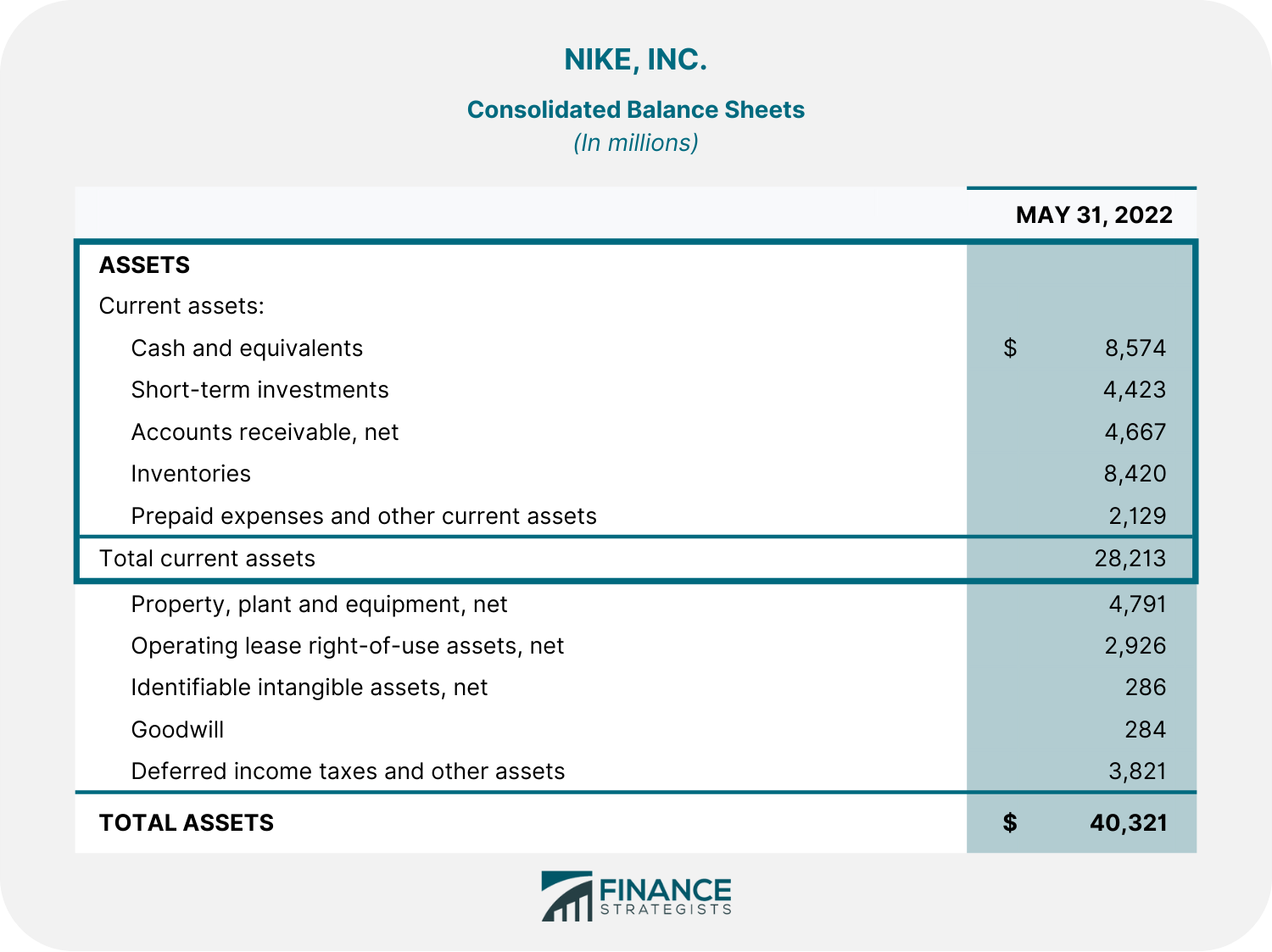

Current assets are assets that are expected to be converted into cash within a period of one year. This includes products sold for cash and resources consumed during regular business operations that are expected to deliver a cash return within a year. Current assets include, but are not limited to, cash, cash equivalents, accounts receivable, and inventory. Current assets reveal the ability of a company to pay its short-term liabilities and fund its day-to-day operations. Current assets are typically listed in the balance sheet in the order of liquidity or how quick and easy it is to turn them into cash. They are arranged from the most liquid, which is the easiest to convert into cash, into the least liquid, which takes the most time to turn into cash. To determine the total current assets, assets under this category are summed up using the formula below: Assets that fall under current assets on a balance sheet are cash, cash equivalents, inventory, accounts receivable, marketable securities, prepaid expenses, and other liquid assets. This is the most liquid form of current asset, which includes cash on hand, as well as checking or savings accounts. It also covers all other forms of currency that can be easily withdrawn and turned into physical cash. It is spendable and requires no conversion. Cash equivalents are short-term investment securities with 90 days or less maturity periods. These include treasury bills, bank certificates of deposit, commercial paper, banker’s acceptances, and other money market instruments. Inventory items are considered current assets when a business plans to sell them for profit within twelve months. These can include raw materials, merchandise, work-in-progress, and finished products. When items have a history of being sold to consumers quickly, they are also referred to as fast-moving consumer goods (FMCGs). The value of these items are summed up and listed on the balance sheet under the inventory category. Inventory is considered more liquid than other assets, such as land and equipment but less liquid than other short-term investments, like cash and cash equivalents. Accounts receivables are any amount of money customers owe for purchases of goods or services made on credit. These outstanding customer balances are expected to be received within one year. Marketable securities are short-term liquid securities that can be quickly sold on a public stock or bond exchange without any loss in their value. It is different from cash equivalents since marketable securities are those securities that tend to mature within a year or less, while cash equivalents mature within three months. To illustrate, treasury bills that mature in three months or less are considered cash equivalents. On the other hand, treasury bills that mature for longer than three months but less than a year are considered marketable securities. Prepaid expenses are advance payments made for goods or services to be received in the future. This includes leased office equipment or insurance coverage. Although prepaid expenses are not technically liquid, they are listed under current assets because they free up capital for future use. Prepaid expenses are first recorded as current assets on the balance sheet. Then, when the benefits of these assets are realized over time, the amount is then recorded as an expense. Other liquid assets include any other assets which can be converted into cash within a year but cannot be classified under the above components. These may also include assets that are not intended for sale, such as office supplies. Since this may vary per company, details about these other liquid assets are generally provided in the notes to financial statements. Below is a consolidated balance sheet of Nike, Inc for the period ending May 31, 2022. The following items comprise the total current assets of Nike, Inc.: Adding these all up, we get the total current assets of $28,213,000. There are several ways businesses use current assets. The most common ways are to: Current assets are used to finance the day-to-day operations of a company. This includes salaries, inventory purchases, rent, and other operational expenses. Knowledge about current assets helps in the management of working capital, which is the difference between the current assets and current liabilities of a company. Managing working capital is vital for business growth and helps avoid cash flow problems. When the working capital is managed well, it can help the business increase its profits, value appreciation, and liquidity. Positive working capital shows that the company has enough current assets to pay off its current liabilities. A negative working capital, on the other hand, means that the company does not have enough current assets to pay its current liabilities. If needed, a company can increase its working capital in several ways. Among other things, it can improve inventory management, negotiate better payment terms with suppliers, or establish a penalty for late payments. Liquidity ratios provide important insights into the financial health of a company. Current assets play a big role in determining some of these ratios, such as the current ratio, cash ratio, and quick ratio. Several ratios use current assets as part of their calculation. Some of the most common ones are: The cash ratio indicates the capacity of a company to repay its short-term obligations with its cash or near-cash resources. As shown in the formula below, it is calculated by dividing cash and cash equivalents by current liabilities. For instance, Company A has cash and cash equivalents of $1,000,000 and current liabilities of $600,000. Its cash ratio would then be 1.67. Company A = $1,000,000/ $600,000 = 1.67 Similar to the example shown above, if the cash ratio is 1 or more, the company can easily meet its current liabilities at any time. On the other hand, if the cash ratio is lower than 1, the company has insufficient cash to pay off its short-term debts. A low cash ratio is not necessarily bad because there might be situations that skew the balance sheets of a company. This can include long credit terms with its suppliers or very little credit extended to its customers. The cash ratio is a more conservative and rigorous test of a company’s liquidity since it does not include other current assets. The quick ratio evaluates a company’s capacity to pay its short-term debt obligations through its most liquid or easily convertible assets. The assets included in this metric are known as “quick” assets because they can be converted quickly into cash. Unlike the cash ratio, it does not just consider cash and its equivalents but also includes accounts receivable and marketable securities. The quick ratio is computed using the formula below. For example, if Company B has $800,000 in quick assets and current liabilities of $600,000, its quick ratio would be 1.33. Quick ratio = $800,000/ $600,000 = 1.33 The quick ratio can be interpreted as the cash value of liquid assets available for every dollar of current liabilities. Thus, a quick ratio of 1.5 implies that for every $1 of Company B’s current liabilities, it has $1.50 worth of quick assets which can cover its short-term obligations if needed. The current ratio evaluates the capacity of a company to pay its debt obligations using all of its current assets. Unlike the cash ratio and quick ratio, it does not exclude any component of the current assets. Thus, the current ratio is computed in the following way: Let us take the case of Company C as an example. With its current assets of $1,000,000 and current liabilities of $700,000, its current ratio would be 1.43. Current Ratio = $1,000,000/ $700,000 = 1.43 When the current ratio is less than 1, the company has more liabilities than assets. Should all of its current liabilities suddenly become due, the value of its current assets would not be enough to cover the needed payments. Conversely, when the current ratio is more than 1, the company can easily pay its obligations and debts because there are more current assets available for use. On the other hand, investors and analysts may also view companies with extremely high current ratios negatively because this could also mean their assets are not being used efficiently. The assets section on the balance sheet is divided into two: current assets and noncurrent assets. Current assets are more short-term assets that can be converted into cash within one year from the balance sheet date. Current assets usually appear in the first section of the balance sheet and are often explicitly labelled. Within this section, line items are arranged based on their liquidity or how easily and quickly they can be converted into cash. Noncurrent assets, on the other hand, are more long-term assets that are not expected to be converted into cash within a year from the date on the balance sheet. While current assets are often explicitly labeled as part of their own section on the balance sheet, noncurrent assets are usually just presented one by one. The most common noncurrent assets are property, plant, and equipment (PP&E), intangible assets, and goodwill. The sum of current assets and noncurrent assets is the value of a company’s total assets. Below is a table summarizing the differences between current assets and noncurrent assets: Current assets are assets that can be quickly converted into cash within one year. These assets, once converted, can be used to fulfill current liabilities if needed. The key components of current assets are cash and cash equivalents, marketable securities, accounts receivable, inventory, prepaid expenses, and other liquid assets. It excludes noncurrent assets such as property, plant, and equipment, intangible assets, and goodwill. Current assets differ from noncurrent assets in a lot of ways. However, the most notable difference is that noncurrent assets are not expected to be converted into cash within one year. Current assets indicate a company’s ability to pay its short-term obligations. They are an important factor in liquidity ratios, such as the quick ratio, cash ratio, and current ratio.What Are Current Assets?

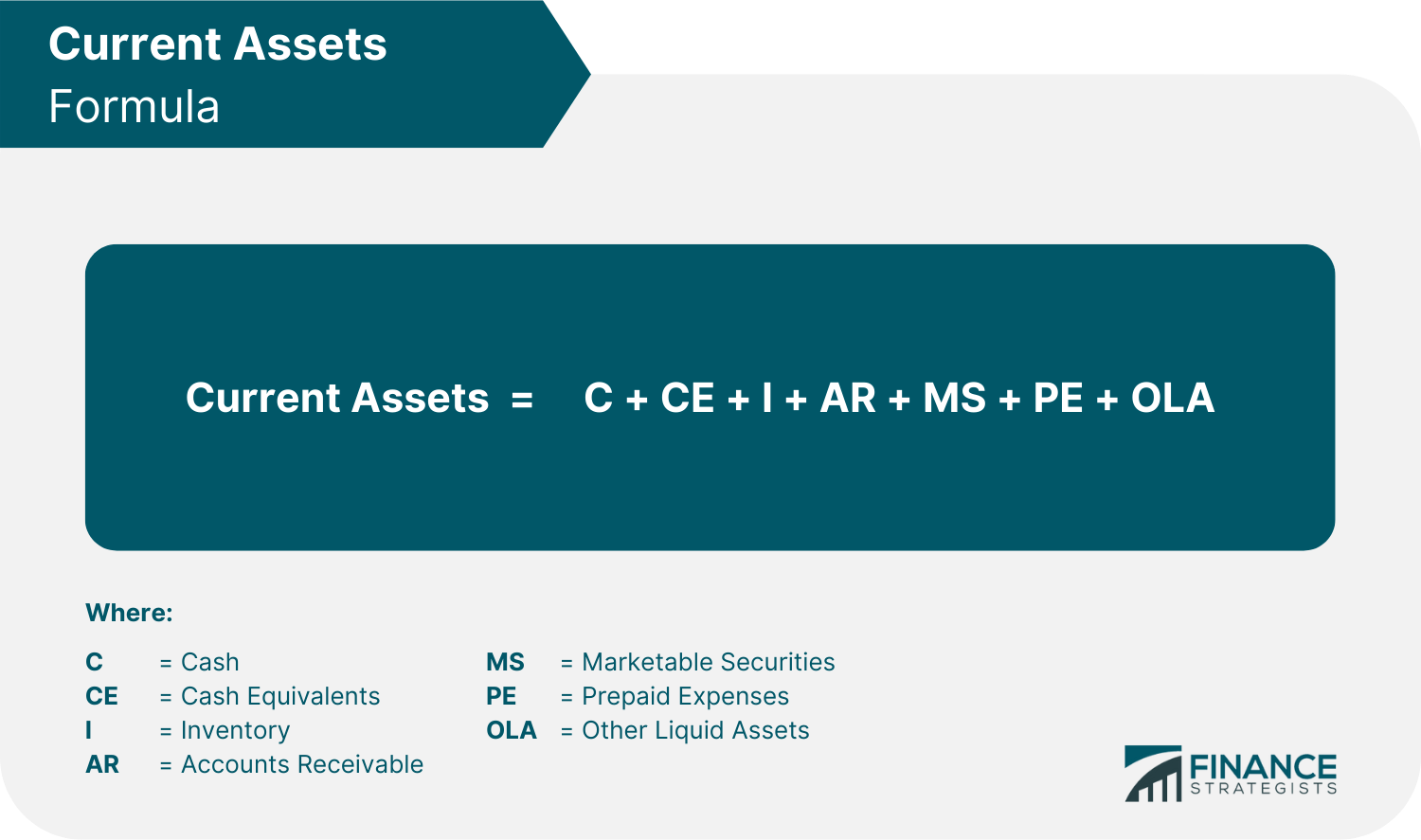

Current Assets Formula

Key Components of Current Assets

Cash

Cash Equivalents

Inventory

Accounts Receivable

Marketable Securities

Prepaid Expenses

Other Liquid Assets

Current Assets Example and Calculation

Uses of Current Assets

Finance Day-to-Day Operations

Manage Working Capital

Determine Liquidity Ratios

Ratios That Use Current Assets

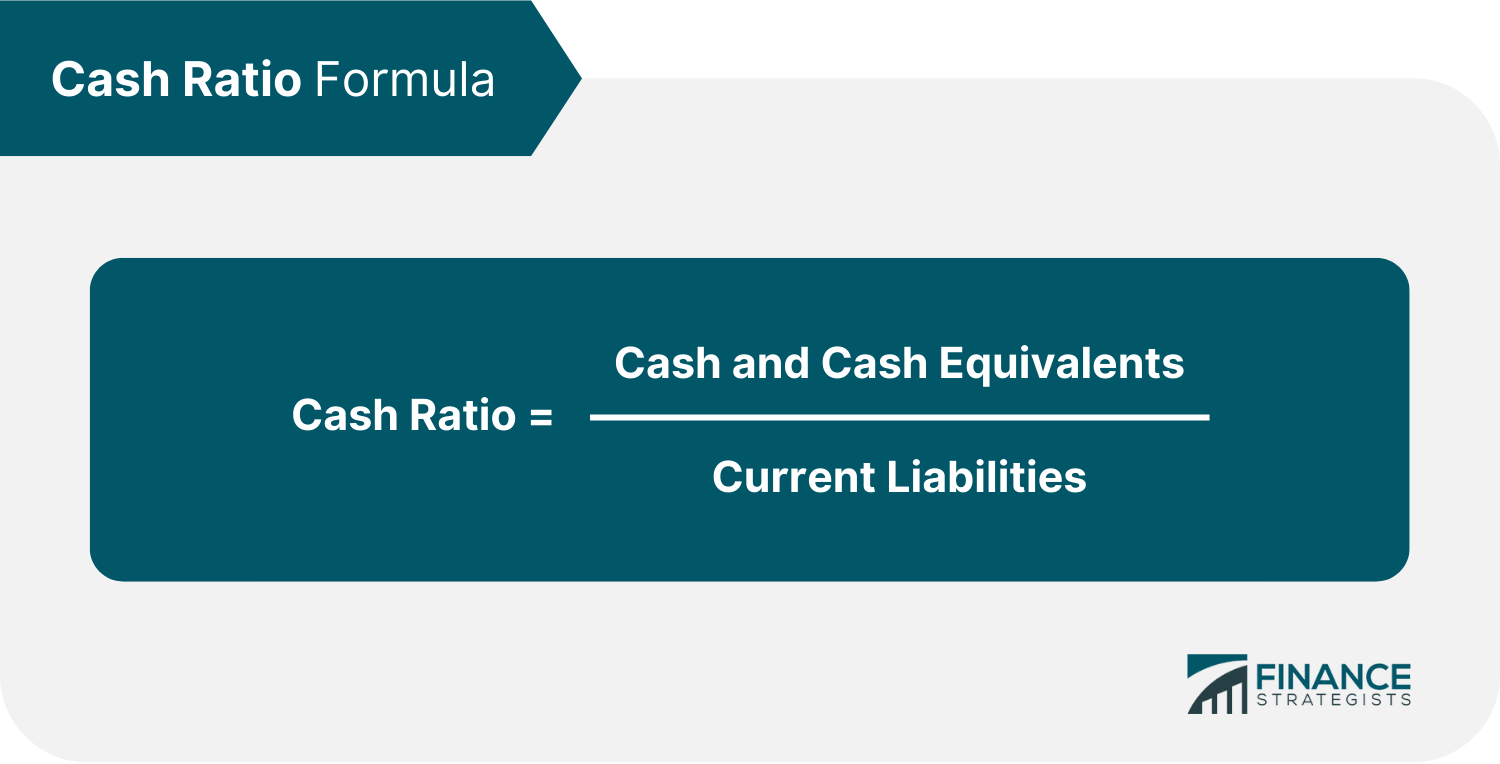

Cash Ratio

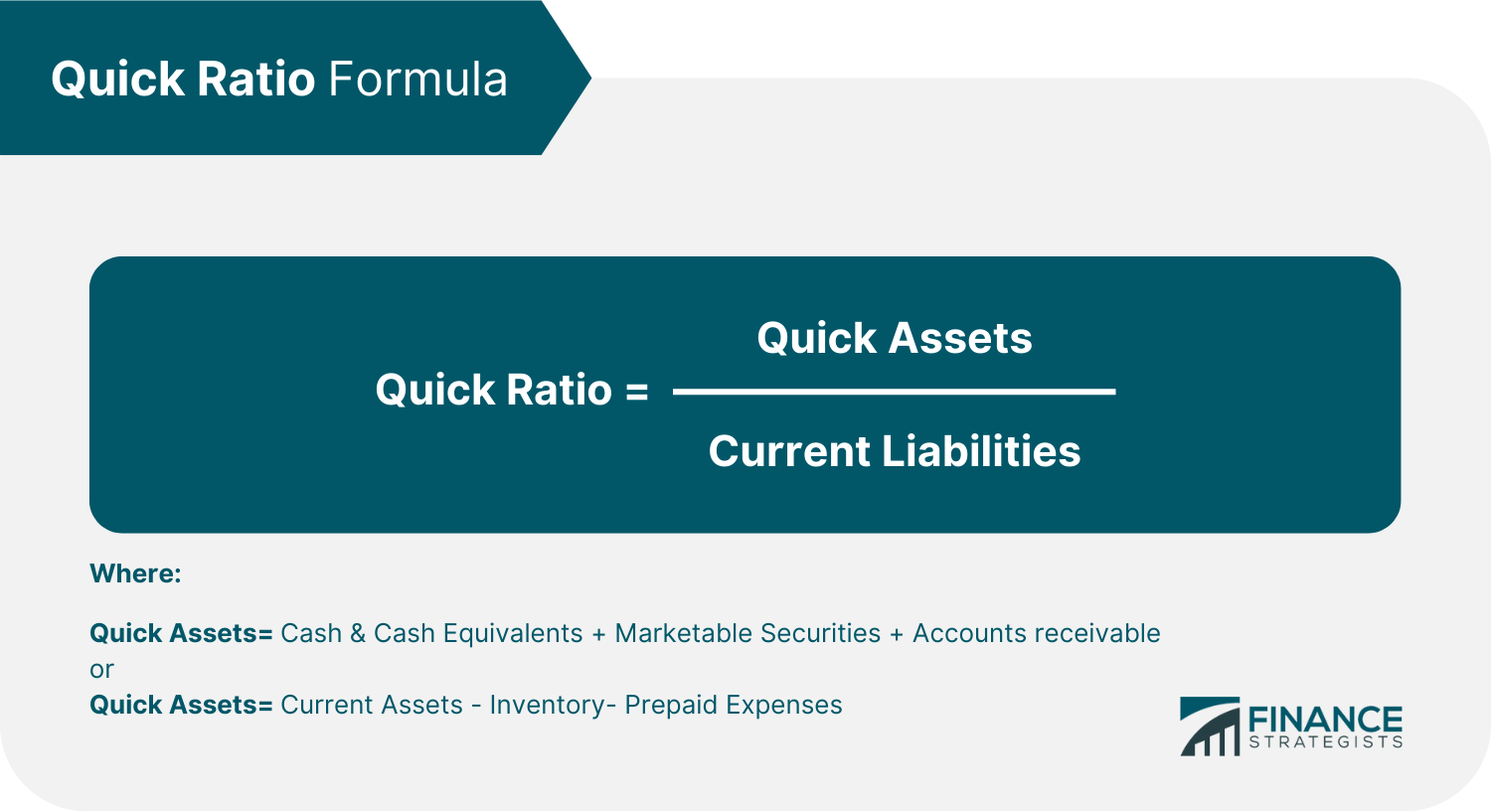

Quick Ratio

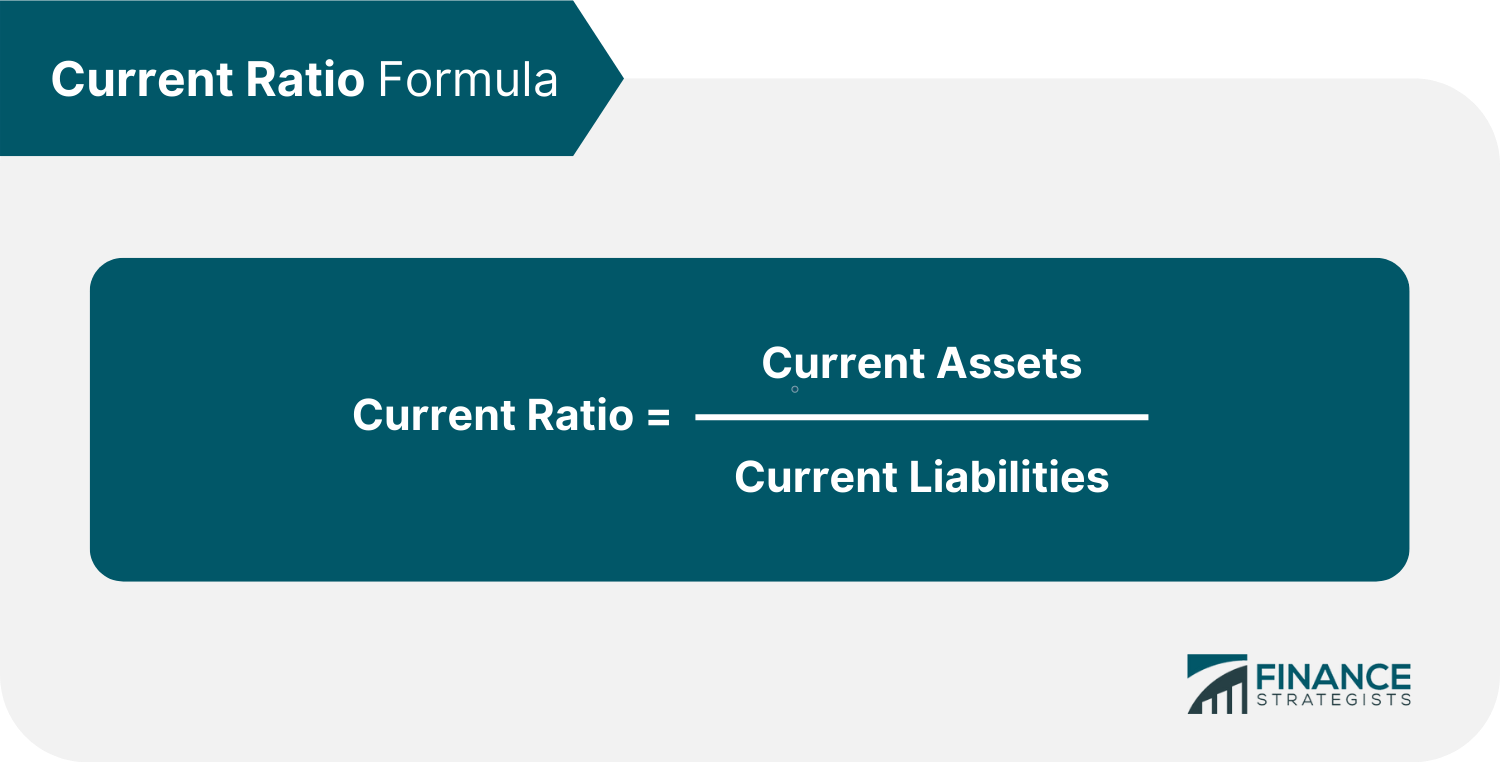

Current Ratio

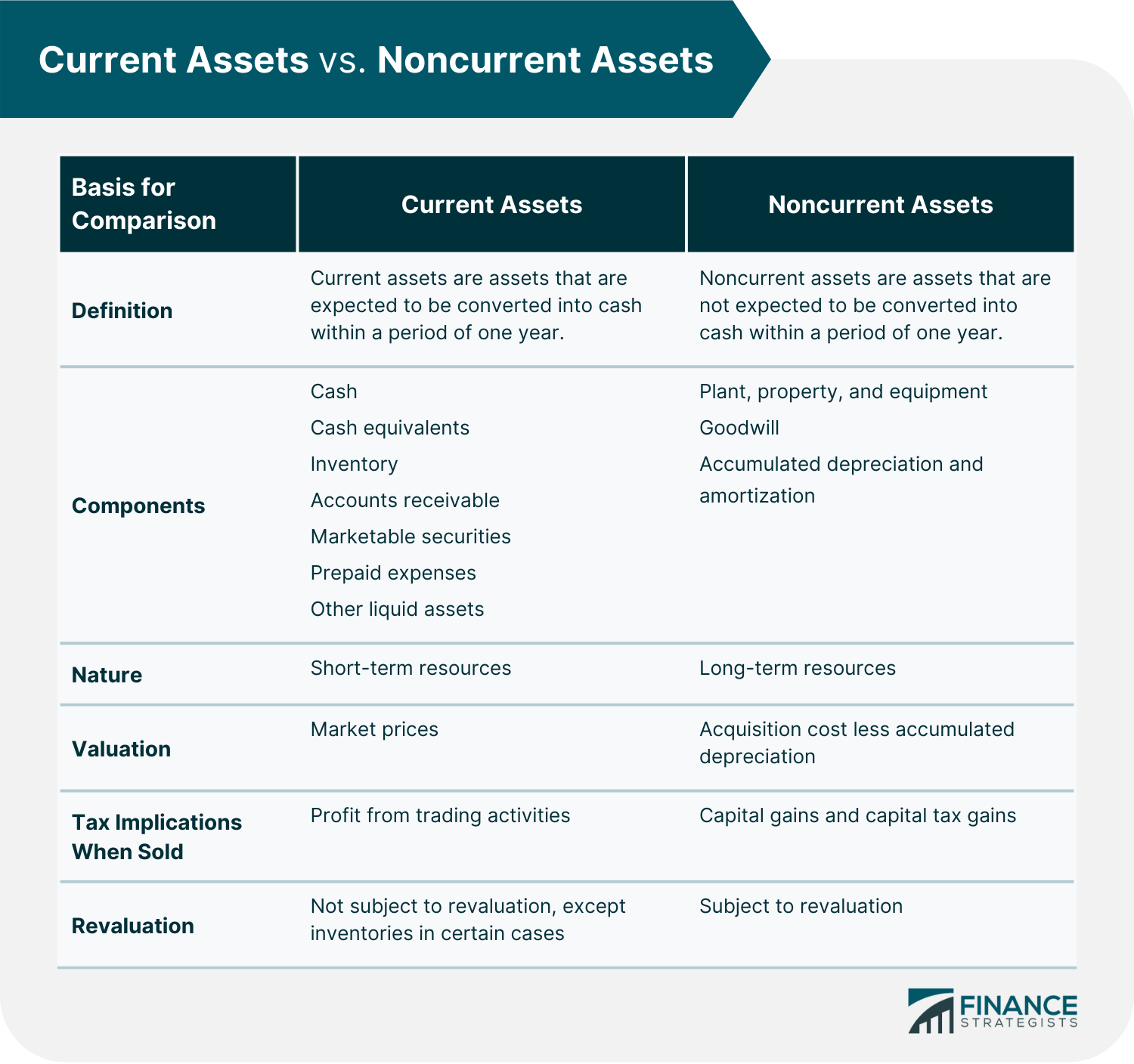

Current Assets vs. Noncurrent Assets

The Bottom Line

Current Assets FAQs

Current assets are referred to as current because they are either cash or can be converted into cash within one year.

Current assets are those assets that can be converted into cash within one year. Fixed or noncurrent assets, on the other hand, are those assets that are not expected to be converted into cash within one year.

It depends on the type of investment. If it is a short-term investment, such as a money market fund, then it would be classified as a current asset. It would be classified as a noncurrent asset if it is a long-term investment, such as a bond.

If a company receives cash from a loan, the amount received is considered a current asset. However, the balance sheet also adds the loan amount to the liability section. If the loan can be repaid within one year, it may become a current asset. Otherwise, it is not considered a current asset.

Current Assets = Cash + Cash Equivalents + Inventory + Accounts Receivable + Marketable Securities + Prepaid Expenses + Other Liquid Assets

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.