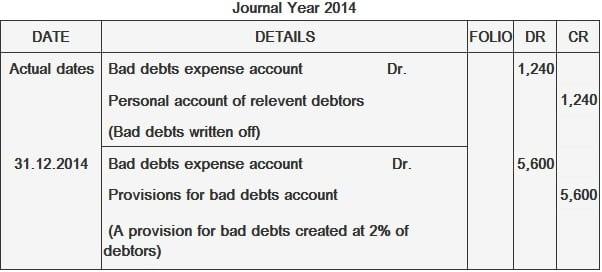

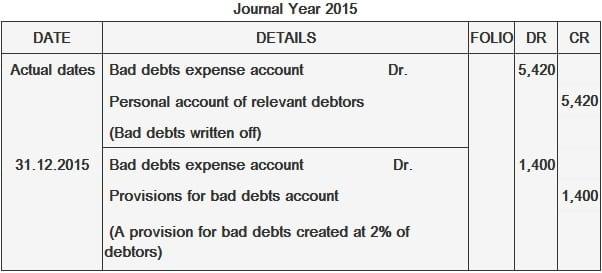

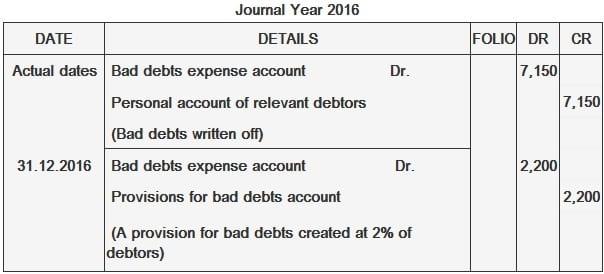

Bad debt is an amount of debt that a business fails to recover from its debtors. At the end of each financial year, most businesses that offer credit to their customers have significant amounts owed to them by their debtors. From experience, all managers know that not every amount shown in the balance sheet as trade receivables (or debtors) will be recovered in the next financial period. Some debtors will invariably fail to pay the amounts due. It is almost impossible to say, with any great degree of accuracy, which debtor will lead to bad debt. However, to assess a year's profit or loss, it is important to charge an amount against that year's profit and loss account to cover both the bad debts that have actually been written off during the year and those that will be known only next year, but that arose from the present year's sales. To clarify, consider the example of Mr. David. During 2014, Mr. David wrote off $9,200 as bad debt, specifically as amounts due from various debtors who either died or declared bankruptcy. On 31 December 2014, Mr. David's debtors stood at $280,000 (after writing off $9,200). He estimates that out of this $280,000, approximately 2% will prove to be bad debt in 2015. It is important to note that Mr. David has suffered two losses. Firstly, the loss of $9,200, which was already written off and appears as a debit balance in the bad debts acocunt. Secondly, there is another almost certain loss of 2% of $280,000 ($5,600), which will need to be written off in 2015. However, this debt (or these debts) arose from sales made in 2014. Therefore, it would be incorrect to charge it as a bad debt to the profit and loss account for 2015. Instead, it must be charged against the profit and loss account for 2014. At the end of 2014, it is not known as to which specific debtor will fail to pay his debts in 2015, though it is known, out of past experience, that some debtors will certainly fail to pay. For this reason, it will not be appropriate to credit the personal account of any particular debtor at the end of a financial year for expected bad debts. To this end, a new account is opened in the books called provisions for bad debts account, or provisions for doubtful debts account. When this account is first opened (typically at the end of a financial year), the following entry is made: At the end of each subsequent financial year, the balance of the provision for bad debts account is adjusted to the correct level of expected bad debts for the next year. It is important to note that the provisions for bad debts account is used only to maintain a provision. It is adjusted at the end of each year; it is not used to record the actual write-off of bad debts, which must pass through the bad debts account. The following information was taken from the books of Mr. David, a wholesaler: Mr. David wishes to maintain a provision for bad debts at 2% of trade debtors. Required: Prepare Mr. David's provisions for bad debts account, bad debts written off account, the relevant portions of the profit and loss account for 2014, 2015, and 2016, and the relevant portion of the balance sheet at the end of each year. Bad debts written off are $1,240. Debtors at the end of the year are $280,000. Provisions for bad debts at 2% of this amount would come to $5,600. Journal entries to record these facts are given as follows: Bad debts actually written off in the year are $5,420. Debtors at the end of the year are $350,000. Provisions for bad debts at 2% of this amount would come to $7,000. However, since there is already an existing provision for $5,600, which is brought forward from the previous year, we need to create a further provision of only $1,400 (i.e., $7,000 less $5,600). It is quite possible that out of the bad debts written off in 2015 (i.e., $5,420), some may relate to the previous year's sales. But having already debited the entire amount of $5,420 to Year 2015's profit and loss account, we need only to adjust the previous year's provisions for bad debts to the desired level at the end of the current year by making an entry for the difference. Theoretically speaking, the correct way to handle bad debts written off in a year, which are known to have arisen in the previous year, would be to make the following entries: Understandably, such a bad debt should not be debited to the bad debts expense account. This is because that account was debited in the previous year. The effect of the above entry is that the credit balance on the provisions for bad debts account would decrease. Now, at the end of the current year, a fresh provision will need to be created to bring the provisions account back to the desired level of the given percentage. This means that the debit entry that will pass through the current year's profit and loss account will have to be larger. To understand this statement, let's consider an example. Suppose that out of $5,420 written off as bad debts in Year 2015, $4,100 is related to Year 2014. This means that only $1,320 ($5,420 less $4,100) is related to Year 2015. Now, if we debit Year 2015's bad debt expense account with only $1,320 and debit the provisions for bad debts account with $4,100, this will bring down the provisions account balance to $1,500 (Balance b/f $5,600 less $4,100). At the end of Year 2015, since we need to raise the provisions for bad debts to 2% of debtors (i.e., $7,000), we will need to debit Year 2015's bad debts expense account with $5,500 (i.e., $7,000 less $1,500). Therefore, the total debit to Year 2015's profit and loss account in respect of bad debts would be $1,320 (written off as bad debts) plus $5,500 (increase in provisions for bad debts), amounting to $6,820. Compare this to the following treatment. When a bad debt is incurred, regardless of when it arose, the bad debt expense account should be debited. At the end of the year, we should simply adjust the provision for bad debts to the required level. Under this accounting treatment, $5,420 would be written off as bad debt, and provisions for bad debts would increase from $5,600 to $7,000. That is to say, an additional provision would be made for only $1,400. Therefore, the total debit to the profit and loss account for Year 2015 would amount to $6,820 ($5420 + $1,400). This is the same figure we arrived at under the previous (and more complex) treatment. With the above in mind, at the end of 2015, it is not necessary to create a fresh provision for bad debts at the full 2% of the debtors outstanding. We need only to increase the provision from $5,600 to $7,000. The net effect of this adjustment is that Year 2015's profit and loss account gets charged for the true bad debts for the Year 2015. Journal entries to record these two facts are shown below. Bad debts actually written off in the year are $7,150. Debtors at the end of the year are $460,000. Provisions for bad debts at 2% of this amount would come to $9,200. However, since there is already an existing provision for $7,000 brought forward from the previous year, we need to create a further provision of only $2,200 (i.e. $9,200 less 7,000). Journal entries to record these two facts are given as follows:What Is Bad Debt?

Why Do Businesses Need Provisions for Bad Debts?

Example

For the year 2014

For the year 2015

For the year 2016

Provisions for Bad Debts FAQs

Bad debt is an amount of debt that a business fails to recover from its debtors. At the end of each financial year, most businesses that offer credit to their customers have significant amounts owed to them by their debtors.

A provision for a bad debt account holds an amount, in addition to the actual written off bad debts during a year, that will be known to be due and payable in respect of bad debts next year. The balance in this account does not belong to any specific debtor or creditors but is held as general provisions.

To assess a year’s profit or loss, it is important to charge an amount against that year’s profit and loss account to cover both the bad debts that have actually been written off during the year and those that will be known only next year, but that arose from the present year’s sales.

When a bad debt is incurred, regardless of when it arose, the bad debt expense account should be debited. At the end of the year, we should simply adjust the provision for bad debts to the required level.

If the provision for bad debts account is not kept at a certain level, then the net result would be that the provision for bad debt must be increased by an amount equal to the actual written off bad debt.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.