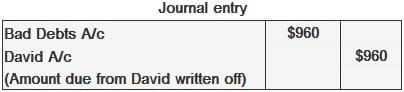

Bad debt is an amount owed to a business that is considered—or proves to be—irrecoverable. There are several reasons why a debtor may fail to pay an amount due, including death, bankruptcy, insanity, and others. Once a business is convinced that an amount due from a debtor is no longer recoverable, it is prudent to remove the amount from the books so that the figures in the books of accounts and balance sheet truly represent the amount due. The entry required to write off bad debt is as follows: Bad debts account is a nominal account and represents a normal business expense. At the end of each financial year, the balance on this account is transferred to the profit and loss account. John has learned that David, who owed him $960, has died and left no estate behind. John decides to write off this amount as a bad debt. Required: Show the journal entry. The effect of the above entry is:Example

Bad Debts FAQs

A bad debt is an amount of money that is owed but cannot be collected by the creditor. It can arise from delinquent payments, fraud or insolvency of the debtor.

The responsibility for writing off bad debts lies with the company's accounting department or financial institution who lent out the money.

Yes, legal implications may exist depending on the circumstance in which the debt was incurred and/or not paid back. It is important to seek professional advice if you think this applies to your situation as it could have serious legal consequences for both parties involved.

The best way to avoid or manage bad debts is by thoroughly vetting a customer’s financial stability, conducting regular credit checks and ensuring that collections are enforced promptly when payments become overdue. It can also be beneficial to have policies in place for debt repayment and/or restructuring of loans owed.

In some cases, businesses may be able to claim losses associated with bad debts as tax deductions, however this will depend on the circumstances of the debt and local laws governing taxation. It is recommended to seek professional advice before attempting any such claims.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.