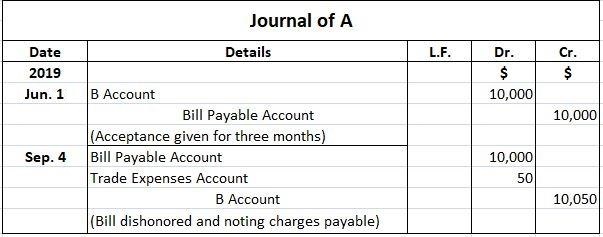

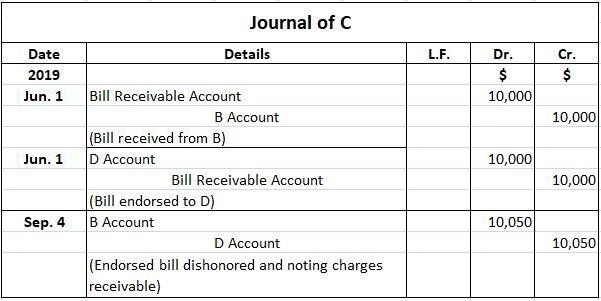

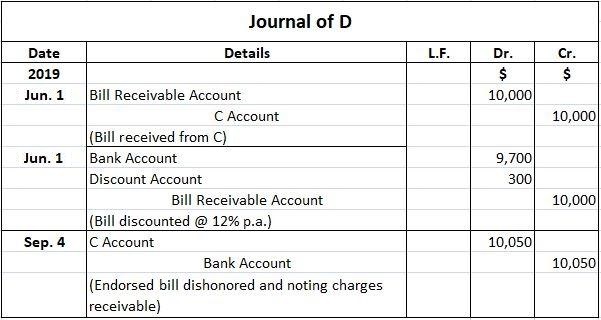

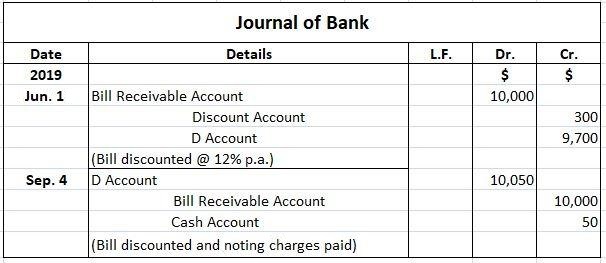

Accounting for bills of exchange starts when the drawer draws a bill and the drawee accepts it. The drawee returns the bill to the drawer after accepting. Now, the drawer is the holder of the bill. Once the drawer is the holder of the bill, they can use the bill in several ways: The drawee is liable to meet the drawer's acceptance, but sometimes they fail to do so and dishonor the bill. Accounting for bills of exchange involves making journal entries and preparing ledger accounts in the books of the drawer and drawee. It is better to learn about journal entries under each of the above cases, after which a detailed accounting treatment will be given. 1. When goods are sold and purchased 2. When the bill is drawn and accepted 3. If the bill is honored on due date 4. If the bill is dishonored on due date 5. When the bill is discounted 6. If the discounted bill is met on due date 7. If the discounted bill is dishonored 8. When the bill is endorsed (the endorsee is the person to whom the bill is endorsed) 9. If the endorsed bill is met on due date 10. If the endorsed bill is dishonored 11. When the bill is sent for collection 12. When the bill sent for collection is met 13. If the bill sent for collection is dishonored Sometimes, the drawee pays the bill before the due date and receives a rebate. This is known as retirement of the bill. In other cases, the drawee may ask the drawer to cancel the bill and draw another bill for an extended period. This is known as renewal of the bill. The drawee pays an additional amount as interest for the extended period. Journal entries under these cases are as follows: 14. If drawee retires the bill (drawee pays the bill before due date), bill is with drawer 15. If the bill is canceled (for renewal purposes) 16. If a partial amount is received from the drawee 17. If interest is charged to the drawee 18. If interest is received in cash The drawer has different options in terms of how they can use a bill of exchange. So far, we have learned about different journal entries for bills of exchange, and now we will discuss the accounting treatment of bills of exchange under each option. Sometimes, the drawer is not in immediate need of cash. They retain the bill until the due date and present it for payment. On the due date, if the bill is paid by the drawee, the bill is said to be honored. If the bill is not paid by the drawee, the bill is said to be dishonored. In January 2019, Mr. A sold goods to Mr. B for $20,000 on credit. On the same day, Mr. A drew three months bills on Mr. B who accepted them and returned the same to Mr. A. The bill was for $20,000. On the due date, the bill is honored by Mr. B. Required: Pass journal entries in the books of Mr. A and Mr. B. Mr. Y purchased goods on credit from Mr. X for $15,000 in April 2019. Mr. X drew a bill of exchange on Mr. Y on the same day for the same amount, which was duly accepted by Mr. Y and returned to Mr. X. On the due date, Mr. X presented the bill to Mr. Y, who returned the bill dishonored. Required: Pass journal entries in the books of both parties. The act of selling a bill of exchange to the bank in consideration of small charges (discount) is called discounting of bill of exchange. As the term of the bill of exchange is drawn for a specific time period, it can be paid only on the due date. If the bill's holder needs cash before the due date, they can ask the bank to discount the bill. When the bank discounts a bill of exchange, it deducts interest from the amount of the bill, and the balance amount is credited to the account of the person who gets the bill discounted. Interest is the rent of money lent by the bank, which is justified by the bank because it has to wait for the bill's due date. Here, interest is known as discount. Discount is an expense for the person who gets the bill discounted and a form of income for the bank. The discounted amount is based on the current rate of interest and the time period (i.e., from the date of discounting to the date of maturity). Study Note: Banks will not discount bills of exchange if the holder has an overdraft balance. On 1 January 2019, John sold goods to David for $25,000 and drew a four-month bill on the latter. David accepted the bill and returned it to John. On 3 February, John got the bill discounted at 6% p.a. The bill was duly met on the due date. Required: Pass journal entries in the books of John, David, and the bank. Study Note: As the drawer has already received the amount of the bill by way of discounting, the drawee will therefore pay the amount of the bill to the bank. Therefore, no entry will be made in drawer's books when the drawee meets the bill. Study Note: No entry is made in the drawee's books on 3 February (when the drawer discounted the bill) because the drawee is liable to pay the bill on the due date. Whatever the drawer does to the bill before the due date is not their concern. When a drawer discounts the bill with their bank, it is the drawee's responsibility to pay the amount of the bill to the bank on the due date. If the drawee fails to do so, the discounted bill is said to be dishonored. This is the person who is appointed by the central government to administer oaths, certify documents, attest to the authenticity of signatures, and perform other official acts. The actions of the notary public, such as the noting of re-presentments of bills, facts, and reasons for dishonor of the bill itself (or a slip of paper attached to the bill) is called noting. Noting is merely a record of dishonor on the face of the bill or on a slip of paper attached to the bill. Protest is a formal certificate of dishonor of bill, issued by the notary public to the bill's holder. The set of issuing certificates is called protesting. A small fee received by the notary public from the holder of the bill for noting and protesting is known as noting charges. Noting charges are paid by the holder of the bill and ultimately recovered from the drawee. Now, if a bill's holder sues for the recovery of the amount, noting and protest would be strong legal evidence. Study Tip: Discounted and Endorsed Bill - A Contingent Liability: After a bill is discounted or endorsed, the drawer has no more responsibility. However, their accounting records are affected if the drawee dishonors the bill on the due date. Therefore, until the bill's due date, it remains the drawer's contingent liability. P bought goods from Q for $5,000 on 1 March 2019. Q drew a three-month bill on P, who accepted it and returned it to Q. Q immediately got the bill discounted with Metropolitan Bank Ltd. at 10% p.a. However, on the due date, P dishonored the bill and the bank paid $100 for noting charges. Required: Pass journal entries in the books of Q, P, and the bank. Study Note: Noting charges are the drawee's expense (i.e., the person who dishonored the bill, not the holder who paid the amount). Study Note: Noting charges are paid by bank deducted from Q's Account and ultimately will be recovered from P. It is an expense of P; that's why Trade Expenses A/c is debited only in P's books. This is another use of the bill of exchange by the drawer. A bill of exchange is easily transferable from one person to another. This is because bill of exchange is a negotiable instrument. The negotiability of a bill of exchange makes it transferable by mere physical delivery, which increases its usefulness. The act of transferring bill of exchange from one person to another for the settlement of debts is called endorsement of bill. The person who transfers or endorses the bill is called the endorser and the person to whom the bill is transferred or endorsed is called the endorsee. On 1 January 2019, John sold goods worth of $12,000 to David on credit. John drew a three-month bill on David on the same date for the amount. John then bought goods from Harry for $15,000. On 4 February 2019, John endorsed David's bill to Harry to settle his debt, paying the balance in cash. On the due date, David met the bill. Required: Record the transactions in the books of all the parties. Study Note: Since John purchased goods from Harry, John is already a debtor of Harry. Entries to record sale & purchased b/w John and Harry are not required. On 1 June 2019, A owed B $10,000 and accepted a bill for three months drawn on him by B. In turn, B settled his debt by endorsing A's bill to C. C endorsed the bill to his creditor D, and D got the bill discounted by his bank at 12% p.a. On the due date, the bill was dishonored by A and the bank paid $50 for noting charges. Required: Pass journal entries in the books of A, B, C, D, and the bank. Study Note: The fact that A owes B means A is already B's debtor. The recording of sales and purchases has already been done. Therefore, there is no need to pass an entry for sales and purchases between B and A. Study Note: Noting charges are paid by the bank, deducted from D's account, and ultimately will be recovered from A. It is an expense of A, which is why Trade Expenses A/c is debited in A's books only. Sometimes a drawer has many bills receivable at a time. It becomes difficult for the drawer to keep the bills safely and to present them to their respective drawee. To overcome this difficulty, the drawer can send the bills to the bank for safety and collection purposes. The act of a drawer sending a bill of exchange to the bank for safety and collection purposes is called bill sent for collection. Bill sent for collection should not be confused with discounting of bill. In discounting, the bill is sold to the bank, whereas in bills sent for collection, the bill is taken into the custody of the bank for safekeeping and convenient collection. John sold goods to Harry for $20,000. Later, John drew a three-month bill on Harry for the amount. Harry accepted the bill and returned it to John, who sent the bill to his banker for collection. On the due date, the bill was met by the drawee and the bank deducted collection charges of $100. Required: Pass journal entries in the books of John, Harry, and the bank. Study Note: It should be noted that bank does not make journal entry in its books of accounts in respect of bill received by bank for collection. However, bank records all particulars of the bill in a Memorandum Book. Bank for collection account does not show bank balance, like a bank account does. Instead, it is a temporary account showing that bills of exchange are kept in a bank. This account is closed on the due date of the bill, when the bill is either met or dishonored. On 1 September 2019, John drew a three-month bill on Harry for $5,000. Harry accepted the bill and returned it to John. On 15 September, John sent the bill to the bank for collection. On the due date, the bank presented the bill to Harry, who returned the bill dishonored. Required: Prepare journal entries in the books of John and Harry.

Journal Entries for Bills of Exchange

A. When Drawer Holds Bill Until Due Date (Option 1)

B. When Drawer Discounts Bill (Option 2)

C. When Bill Is Endorsed to Third-party Endorsee (Option 3)

D. When Bill Is Sent to Bank for Collection (Option 4)

Options Available to Drawer in Using Bill of Exchange

Option 1: When Drawer Holds the Bill Until Due Date

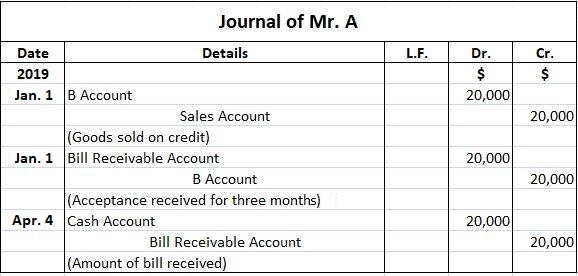

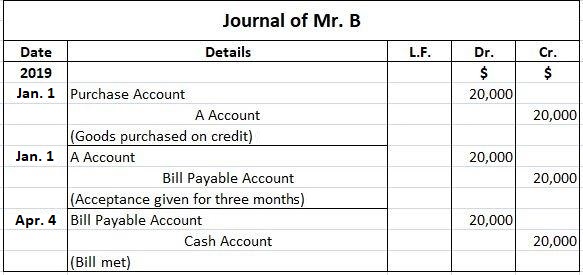

Example 1: Bill Retained by Drawer, Bill Met

Solution

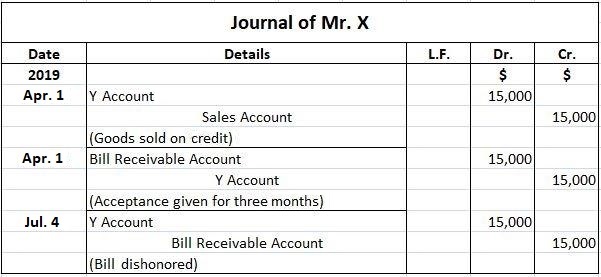

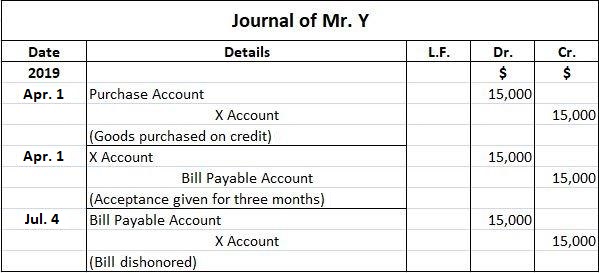

Example 2: Bill Retained by Drawer, Bill Dishonored

Solution

Option 2: When Drawer Discounts Bill

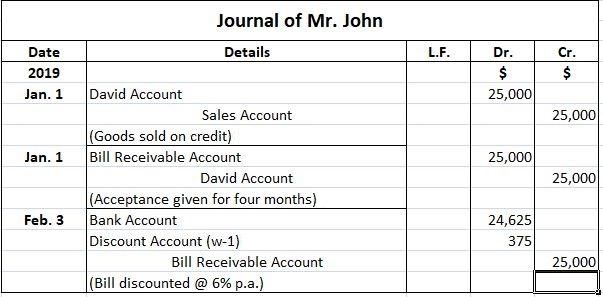

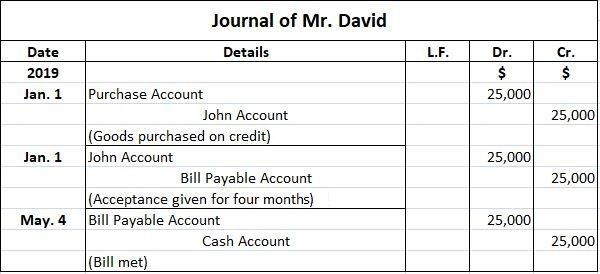

Example 3: Discounted Bill Met

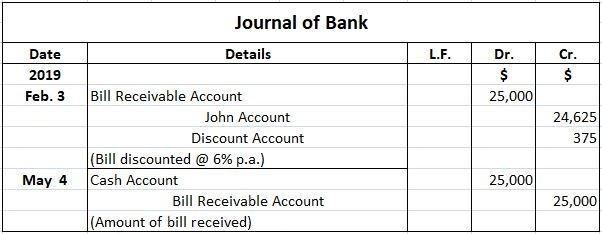

Solution

Discounted Bill Dishonored

Notary Public

Noting

Protest

Noting Charges

Example 4: Discounted Bill Dishonored

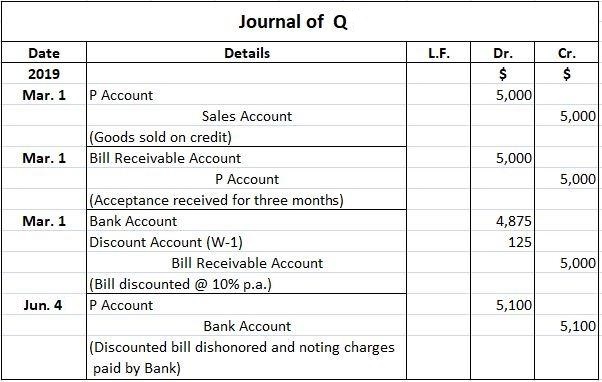

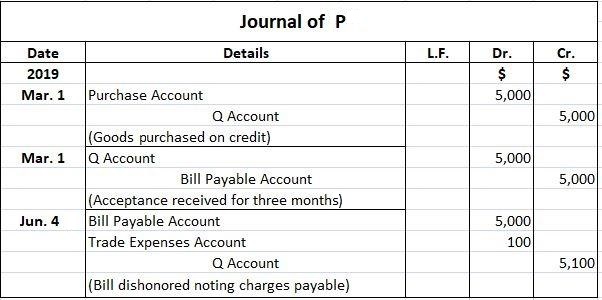

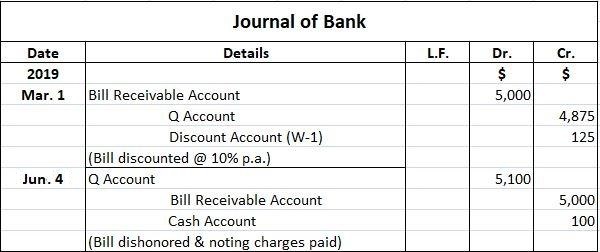

Working

Option 3: When Bill Is Endorsed to Third-party Endorsee

Example 5: Endorsed Bill Met

Solution

Example 6: Endorsed Bill Dishonored

Solution

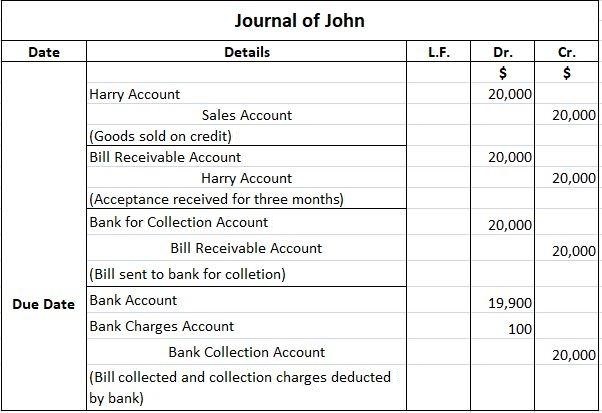

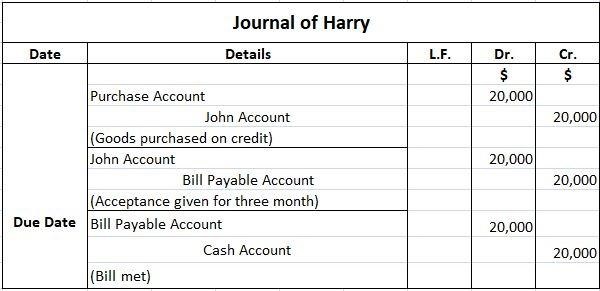

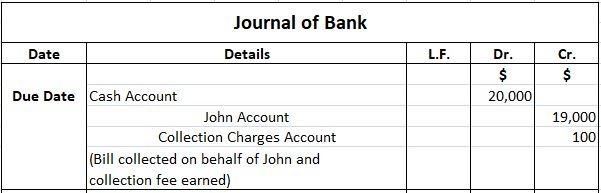

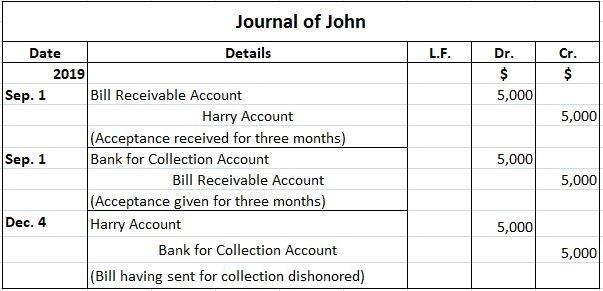

Option 4: When Bill Is Sent to Bank for Collection

Example 7: Bill Sent For Collection Met

Solution

Bank for Collection Account

Example 8: Bill Sent For Collection, Dishonored

Accounting for Bills of Exchange FAQs

Accounting for bills of exchange starts when the drawer draws a bill and the drawee accepts it. The drawee returns the bill to the drawer after accepting it. Now, the drawer is the holder of the bill.

By holding the bill till due date, by discounting the bill, by endorsing the bill, by sending bill to bank for collection

When goods are sold and purchased and when the bill is drawn and accepted.

Option 1: when drawer holds the bill until due date, option 2: when drawer discounts bill, option 3: when bill is endorsed to third-party endorsee and option 4: when bill is sent to bank for collection

A bill of exchange is a written order by one party (the "drawer") to another party (the "drawee") to pay a specified sum of money at a certain time. A bill of exchange is typically used in international trade to make payments between two parties, and can be traded or sold to third parties.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.