A double column cash book, also known as a two column cash book, consists of two columns on each side to record cash and bank transactions. Rather than separating cash and bank accounts, a double column cash book enables accountants to maintain the two accounts side by side. This allows for greater convenience when recording transactions. In particular, we can quickly see overall balances. Simply by adding a bank column to both sides of a single column cash book, we can turn it into a double column (or two column) cash book. Compared to single column cash books, double column cash books have the following advantages: The format of a double column cash book is similar to a single column cash book. The exception is that an additional column is included on both sides to record cash discount. An overview of the format of a double column cash book, which is commonly used by organizations to account for their cash transactions, is shown below. The following procedure is used to post entries from a double column cash book to ledger accounts: Prepare a double column cash book using the following transactions, and post the entries, therefore, to ledger accounts. For the year 2016, the transactions are as follows:Advantages of Double Column Cash Book

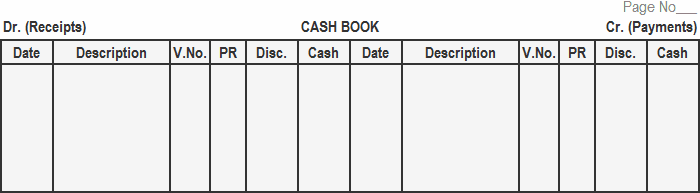

Format/Specimen of Double Column Cash Book

Posting the Double Column Cash Book

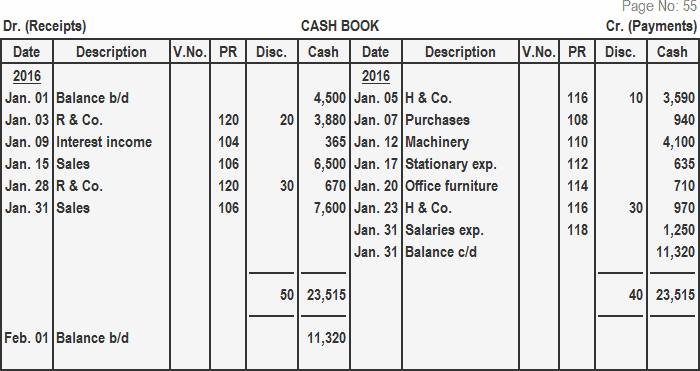

Example

Solution

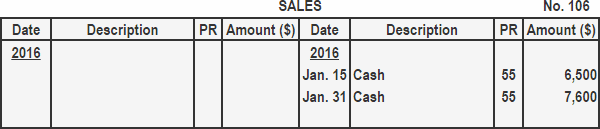

General Ledger

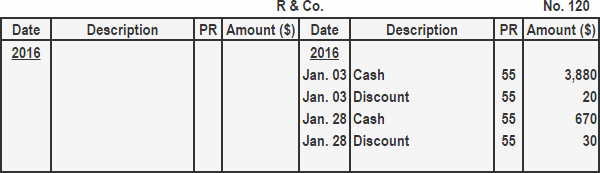

Accounts Receivable Ledger

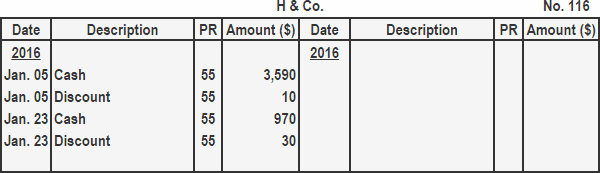

Accounts Payable Ledger

Cashbook Exercises

Double Column Cash Book FAQs

Rather than separating cash and bank accounts, a double column cash book enables accountants to maintain the two accounts side by side. This allows for greater convenience when recording transactions. In particular, we can quickly see overall balances.

Convenience: cash and bank accounts are kept side by side in one place and cost– and time-effective: no separate bank account needs to be maintained.

The format of a double column cash book is similar to a single column cash book. The exception is that an additional column is included on both sides to record cash discount.

The chief difference between the two types of cash books is their structure. Double-column cash books, for example, have two money columns: cash and bank. Triple-column cash books, on the other hand, have three money columns: cash, bank and discount.

A single-column cashbook records only transactions involving the exchange of actual cash in hand. A double-column cashbook records both cash and bank transactions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.