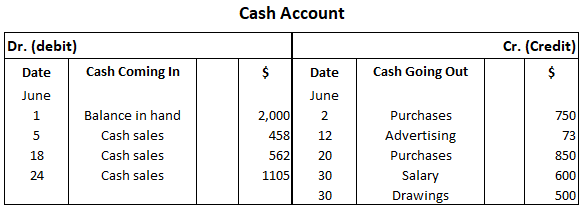

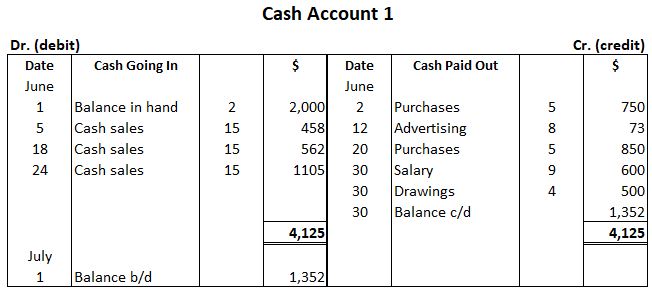

In accounting courses, the cash account is usually first explained as part of the ledger system. Some students may already be familiar with the simple recording of receipts and payments of money. The main rule for all cash accounts is that you debit cash coming in and credit cash paid out. Assume that you start in business (a small retail shop) on 1 June with $2,000 cash as your starting capital. At present, we will only deal in currency notes and coins: checks and bank transactions will be explained later. During the month of June, all your business dealings are for cash. The details of your trading transactions are listed below. These transactions are entered or "posted" in your cash account for the month of June as the first stage of a bookkeeping exercise involving the receipt and payment of money only. Note that at this stage there are no credit transactions. The cash account is now made up for the month of June, all money received being debited, and all money paid being credited. Note the one-word description for all the credit entries, as well as the complete absence of the words "cash" and "paid" on this side. This is because all these entries refer to cash payments. 1. The cash in hand, a debit balance at 1 June, is your starting capital in this instance, being the sole asset and property possessed by the business on this date. In later exercises, it will be seen that business property in money is normally only part of the proprietor's capital. 2. Cash takings or cash sales refer to the normal and continuous "across the counter" sales of the small retailer. This is in contrast to any credit sales where the possession of the goods passes from vendor to buyer at the time of the sale (deferring settlement and payment until later). In these early exercises, we are concerned only with cash purchases and cash sales. 3. The narrow column on the left of each cash column is used for cross-referencing to the appropriate and corresponding account of the double entry. 4. Goods and merchandise bought by the business to be re-sold are called purchases. This cost is distinguished from the other many and varied trading expenses, and also to show a clear distinction between this basic trading expense and the cost of property and assets such as machinery and fixtures. 5. The one-word description for each entry, to the greatest possible extent, is important; it serves to identify the opposite and corresponding double entry, which is normally in another ledger. 6. The posting of all amounts entering an account on the debit side, and all amounts leaving an account on the credit side avoids the need for continual addition and subtraction until the balancing-up stage, generally at the end of the month. 7. The shape formed by the line running across the top of the account and the line running down between the credit and the debit side is the reason why these are popularly known as T-Accounts. 1. Center the heading of the cash account and leave a blank space between the heading and details within the account. 2. The name of the month does not need to be repeated after it is placed at the top of the date column, but the date of each transaction must be given. 3. The $ sign need only be shown at the top of each cash column, and should not appear against the individual receipts and payments. 4. As far as possible, use a single one-word explanation for the entry in the details part of the account. 5. The words "received" and "paid" are superfluous in the details section, and the word "cash" need only appear on the debit side to distinguish cash sales from any sales on credit (which are not posted to the cash account). 6. The correct and vertical alignment of the figures in the money columns will make additions easier at the balancing-up stage. In bookkeeping, balancing simply means adding up the debit and credit sides of an account and deducting the smaller side (of less total value) from the larger side. The difference between the two sides is called the balance of the account. Later it will be seen that the cash account is kept in a special ledger called the cash book. In practice, this would probably be balanced weekly, and certainly at the end of every month. The cash account above is reproduced here and balanced up in an ordinary way. Study the table below and then read the following instructions on balancing. The payments shown are after any discount allowed. It is worth noting that there are fewer items on the debit side of this cash account. Spaces have been left blank to allow for neatness and to ensure that the corresponding totals are on the same horizontal level. The folio or page numbers relating to the opposite and corresponding double entry have been inserted in the narrow folio column in front of each amount, prior to posting the double entry in the separate ledger accounts. For clarity, the folio or page number is shown in brackets after the name of each ledger account in these early stages. The balance of cash in hand on 30 June ($1,352.00) is the difference between the debit total of $4,125.00 and the total of the payments ($2,773.00). This balancing figure of $1,352.00 is inserted as an additional item on the credit side above the total. The two totals now agree and are ruled off in the manner shown. The total of the payments ($2773.00) before balancing may be noted in pencil but is not inked-in as a permanent feature. The difference or balance on an account should never be left suspended in mid-air. In the case of the cash account, the balance will be entered as the last item on the credit side above the total, and then brought down below the debit total on the opposite side. The two totals are ruled off neatly on the same horizontal level, the lower line of the total being double-ruled. The abbreviations c/d and b/d signify "carried down" and "brought down." Balances or totals are sometimes carried forward from one folio to another, the abbreviations c/f and b/f denote "carried forward" and "brought forward." Regarding cash account balancing, remember this: 1. First, make your additions in pencil and ink-in afterward. In balancing, remember to deduct the total of the payments from the total of the receipts, only inserting the difference (i.e., balance) on the credit side above the total on the right-hand side of the cash account. 2. Bring down the same amount shown on the credit side above as a debit balance now below the total on the left-hand side of the account. This debit balance is simply the excess receipts overpayments. 3. Cash account totals must be on the same horizontal level, and the lower line should be double-ruled to indicate a total. 4. With a little concentration, these simple cash book exercises will quickly teach you how to record elementary cash transactions, leading to the routine of ledger posting.Cash Account: Definition

Setting Up a Cash Account

June

$

2

Goods bought for resale

750

5

Money received for goods sold

458

12

Paid for classified advertising

73

18

Cash takings (i.e., cash sale)

562

20

Bought further goods for cash

850

24

Cash sales

1105

30

Paid salary to temporary assistant

600

Withdrew cash for private use (i.e., drawings)

500

Explanatory Notes

Focal Points When Preparing a Cash Account

Balancing the Cash Account

The physical cash balance must always be a debit balance because money can only be paid out of an available fund or balance in hand. You must never have a credit cash balance.

Key Points

Cash Account FAQs

The physical cash balance must always be a debit balance because money can only be paid out of an available fund or balance in hand. You must never have a credit cash balance.

You should bring down the same amount shown on the credit side above as a debit balance now below the total on the left-hand side of the cash account. This debit balance is simply the excess receipts overpayments.

A cash receipt is an inflow of cash, while a cash payment is an outflow of cash.

A credit balance means that there are more credits than debits, while a debit balance indicates that there are more debits than credits.

A cash overpayment is an inflow of money that exceeds the amount that was expected or budgeted.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.