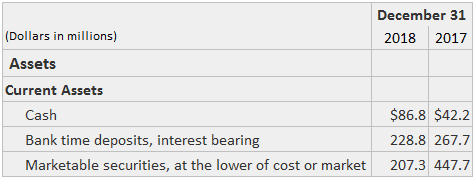

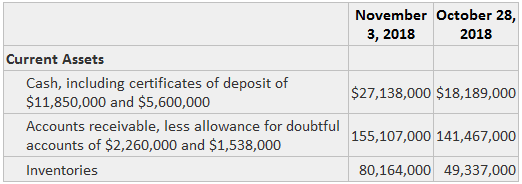

When reporting on cash equivalents, accountants must consider: The carrying value is the original amount invested plus accrued income. Depending on the amount of detail needed or desired for a financial report, highly liquid savings accounts or money market fund holdings can be combined with cash into a single item on the balance sheet. Since their carrying value is determined differently, significant investments in marketable equity securities should not be combined with cash and cash equivalents. If Sample Limited transfers $10,000 from the First National Bank checking account to a savings account at First Federal Savings and Loan, this entry would be recorded: At the balance sheet date, if 3% interest has been earned, the following entry would be made: Two ways to disclose cash equivalents are shown below. In the first example, Xerox Corporation has chosen to separate cash equivalents from cash. On the other hand, in this example, Tyson Fresh Meats, Inc. has combined cash and cash equivalents in a single item.

Example

Cash Equivalents FAQs

Cash equivalents are highly liquid investments that can be converted into cash easily. However, cash is currency on hand or in banks, including notes and coins, checking accounts, savings accounts, money market funds, etc.

Adjusting Entries are used to adjust Financial Statements for transactions that occur after the balance sheet date.

As of 2016, no authoritative guidance has been issued on this topic. However, in 2014 the AICPA formed a task force to consider changes to ASC 860. The task force's final recommendation was not to make any changes.

Adjusting Entries are used to adjust Financial Statements for transactions or other events that occur after the balance sheet date.

The adjusted carrying value is equal to the carrying value plus interest earned. As of 2016, no authoritative guidance has been issued on this topic.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.