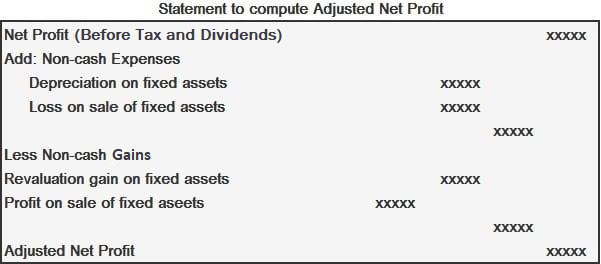

Adjusted net profit (ANP) is a useful number to check a business' worth or its financial strength. This figure is especially useful when a business is being sold to another. In which case, potential buyers prefer looking at the business value as an acquired asset through its adjusted net profit, rather than considering only its net profit. Net profit is often an accounting concept more useful for the business owner instead of potential buyers of the business. Net Profit is simply the result of deducting the cost of goods sold and other expenses from sales. Adjusted net profit, on the other hand, is net profit plus non-cash expenses less non-cash gains. Non-cash expenses may include depreciation on fixed assets or losses on the sale of fixed assets. Non-cash gains include revaluation gain on fixed assets and profits on the sale of fixed assets. Adjusted net profit provides a better idea of a company's performance from its usual operations by taking into account non-cash items. If a company issues fresh shares during the year, the amount of cash received against such an issue is clearly a source of cash. However, the following two points need attention here: 1. Issue of shares against cash at par, premium, or discount If a company issues shares for cash at par, the amount of cash received will be equal to the increase in paid-up share capital. This is relatively simple to handle: the amount of increase in share capital is shown as a source of cash in the Cash Flow Statement. If the company issues shares for cash at a premium, the amount of cash received will be more than the increase in paid-up share capital. There will therefore also be an increase in the amount of Capital Reserves or Share Premium Account. The total of these two increases (i.e., increase in paid-up share capital and increase in share premium account) represents the amount of cash inflow on account of the issue of shares. This can be shown in the Cash Flow Statement as two separate items, or just as one item. It is preferable to show them as two items (namely, share capital and share premium) to avoid confusion. While it is theoretically possible to issue shares at a discount, this is a very rare occurrence. The way to handle the issue of shares at a discount in a Cash Flow Statement is to: If a company issues shares as bonus shares, the entries made are a debit to the Profit & Loss Appropriation Account and a credit to the Share Capital Account. No cash is involved and, therefore, no entry passes through the cash account. For this reason, the issue of bonus shares does not represent any cash inflow. It should, as a consequence, not be reported in the Cash Flow Statement.What Is Adjusted Net Profit?

Net Profit vs Adjusted Net Profit

Format of Statement to Compute Adjusted Net Profit

Increase in Share Capital as a Source of Cash

2. Issue of shares as bonus shares

Adjusted Net Profit FAQs

There is only one format for calculating adjusted net profit. However, the calculation method differs depending on the accounting policy (i.E., Full absorption or partial/modified absorption) of a company.

The adjusted net profit in the case of partial or modified absorption accounting policies is equal to the amount arrived at by deducting the non-cash expenses (i.E., Depreciation and exchanges) from (1) minus (2). (1) + Interest expense - any one-time income/expense items - , (2) = adjusted net profit

The ratio that should be used for calculation of adjusted net profit is 1:1 (i.E., It has no effect on the final result).

The only difference between devolved and segregated gross Fixed Assets is in the way revenues and expenses are distributed among different levels of organization. For both kinds of gross Fixed Assets, Depreciation is charged at the same rate for similar reasons. Neither method affects net profit or Cash Flow statement items.

All debit balances should be deducted from the gross revenue. This includes: (1) other incomes and (2) provisions and other deductions, as well as any one-time income/expense items recognized by a company.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.