A cash flow statement (CFS) is a financial statement primarily intended to provide information about the cash receipts and cash payments of a business during the period of time covered by the income statement. It is vital to keep track of cash flows on a continuing basis in order to keep a business healthy. Cash is a company’s most liquid asset; it is the lifeblood of operations. Without adequate cash, and regardless of the long-term assets that may be owned, a business cannot pay employees, creditors, taxes, dividends, or expenses. So, it naturally follows that investors, creditors, and other interested parties would want to know as much as possible about a company’s cash receipts and cash payments. The cash flow statement (CFS) shows much more about cash than do other financial statements. For example, the balance sheet simply reports how much cash is held as of a specific date. By comparing cash as reported on a current balance sheet with cash as reported on the balance sheet at the end of the preceding year, we can see how much cash changed—but not why it changed. The statement of cash flows analyzes cash receipts and payments to show how cash was acquired and spent during the accounting period. A company’s cash flow statement shows the movement in cash items that takes place over a given financial period. The aim of preparing a cash flow statement is to reconcile the company’s opening cash position with its closing cash position. This is achieved by providing a fairly detailed—and itemized—list of sources from which additional cash was generated during the period and the use to which such cash was put. A secondary objective of the statement of cash flows is to provide information about the financing and investing activities of a business. This statement shows various causes of variances in cash balance. Like the fund flow statement, this statement also shows the inflow and outflow of cash between two time periods—generally from January to 31 December. A statement of cash flows must be included in all financial reports that contain both a balance sheet and an income statement. The cash flow statement replaced the statement of changes in financial position as the fourth required financial statement. Cash flow reflects only the total cash inflow and closing cash at the end of the accounting period. As such, it speaks about the short-term financial positions of a company. It focuses on the speed of cash being collected from debtors, stock, and other current assets, as well as the use of cash in paying current liabilities. A cash flow statement is a brief statement that shows: A cash flow statement is also a detailed statement that shows: The statement of cash flows is classified into the following three separate categories of cash flows: The procedure is the same as with a fund flow statement. The left-hand side records various sources of cash inflows and the right-hand side records the use or outflows of cash. 1. Cash inflows: Opening cash, cash from operations, issue of share capital, issue of debentures, issue of long-term loans, sales of fixed assets, and capital profits (profit on the sale of fixed assets) 2. Cash outflows: Cash lost in operations, redemption of preference shares, redemption of debentures, repayment of long-term loans, purchase of fixed assets for cash, and payment of liabilities. The main objectives of the cash flow statement are to provide information and knowledge about the following key areas: 1. Knowledge of cash inflows and outflows: The cash flow statement shows the various sources of cash inflow into the businesses, as well as where cash has been applied. 2. Knowledge of trading profits: The statement offers insights into how cash is generated and where it is being used, as well as what the balance is and whether it is in excess or not. 3. Knowledge of increase or decrease in share capital: The cash flow statement highlights the changes in share capital (whether it has increased or decreased). 4. Knowledge of purchase or sale of fixed assets: The statement provides useful information about the purchase or sale of fixed assets. 5. Knowledge of increase or decrease in long-term loans: The statement shows why long-term loans were raised or, if a loan is paid, what the source of the payment was. 6. Knowledge of increase or decrease in cash balance: The statement highlights the exact position of whether the cash in the business has increased or decreased over a specific period. 7. Knowledge of tax and dividends paid: This statement is useful in helping to learn about the amount that a business usually pays for taxes and dividends. From the following balance sheet of Star Mills Ltd., prepare a cash flow statement. Additional information is given as follows: Cash from operations Cash flow statement 1. Tax paid 2. Machinery purchased 3. Business premisesCash Flow Statement: Definition

To Understand Cash Flow, Let’s First Understand "Cash"

Cash Flow Statement: Explanation

Classification of Cash Flows

Steps to Prepare the Cash Flow Statement

Format/Specimen of Cash Flow Statement

Cash Inflow Amount Cash Outflow Amount 1. Opening cash

xxxx

Payment of:

2. Cash from operations

xxxx

1. Dividends

xxxx

3. Long-term loans

xxxx

2. Tax

xxxx

4. Increase in share capital

xxxx

3. Long-term loans

xxxx

5. Sale of fixed assets

xxxx

4. Decrease in preference share capital

xxxx

6. Issue of debentures

xxxx

5. Fixed assets purchase

xxxx

6. Redemptions of debentures

xxxx

7. Cash closing balance

xxxx

Objectives of the Cash Flow Statement

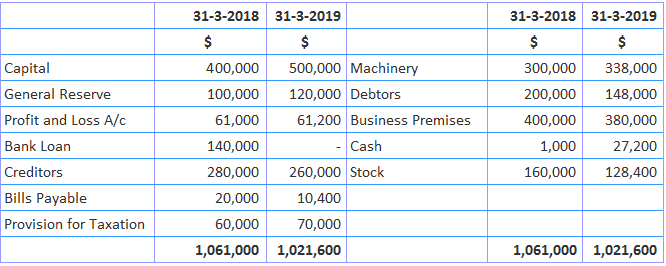

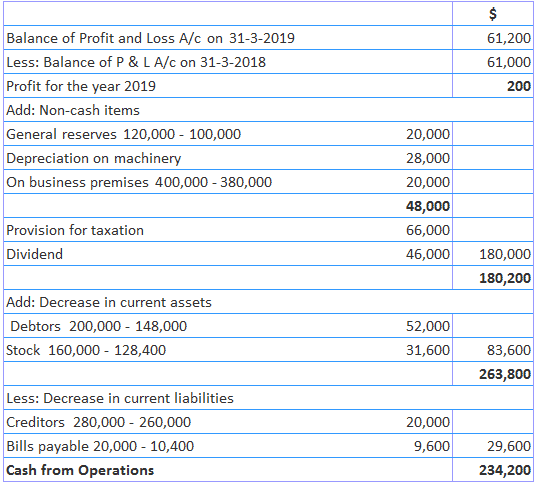

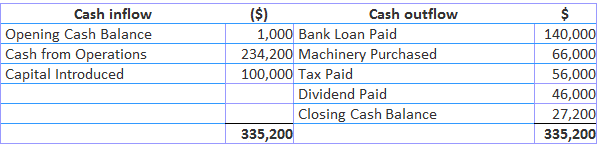

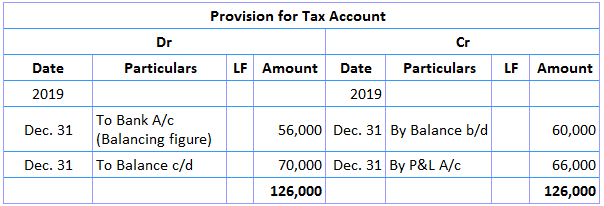

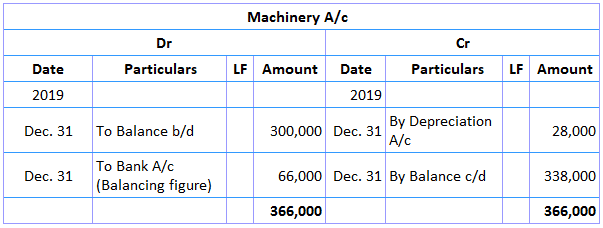

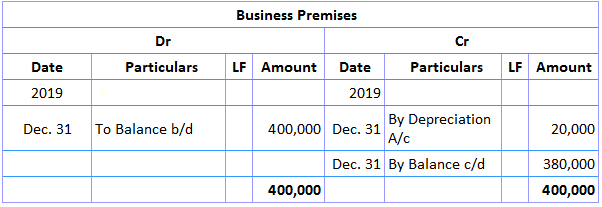

Example

Solution

Working notes

Cash Flow Statement (CFS) Preparation FAQs

A Cash Flow statement (CFS) is a Financial Statement primarily intended to provide information about the cash receipts and cash payments of a business during the period of time covered by the income statement.

The statement of Cash Flows is classified into the following three separate categories of Cash Flows: Cash Flows from operating activities, Cash Flows from investing activities and Cash Flows from financing activities.

Cash inflows: Opening cash, cash from operations, issue of share capital, issue of Debentures, issue of long-term loans, sales of Fixed Assets, and capital profits (profit on the sale of Fixed Assets)

Cash outflows: Cash lost in operations, redemption of preference shares, redemption of Debentures, repayment of long-term loans, purchase of Fixed Assets for cash, and payment of liabilities

The main objectives of the Cash Flow statement are to provide information and knowledge about the following key areas: Knowledge of cash inflows and outflows, Knowledge of trading profits, Knowledge of increase or decrease in share capital, Knowledge of purchase or sale of Fixed Assets, Knowledge of increase or decrease in long-term loans, Knowledge of increase or decrease in cash balance and Knowledge of tax and dividends paid.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.