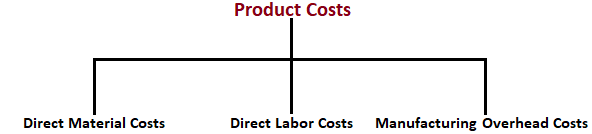

In a manufacturing organization, an important difference exists between product costs and period costs. Product costs (also known as inventoriable costs) are costs assigned to products. These costs are identified as being either direct materials, direct labor, or factory overheads, and they are traceable or assignable to products. Product costs only become an expense when the products to which they are attached are sold. Product costs are also related to manufacturing activities. Examples of product costs include the cost of raw materials used, depreciation on plant, expired insurance on plant, production supervisor salaries, manufacturing supplies used, and plant maintenance. Period costs are expired non-product costs. They are identified with measured time intervals and not with goods or services. Period costs can be defined as any cost or expense items listed in the firm’s income statement. Examples of period costs include selling costs and administrative costs. Both of these costs are considered period costs because selling and administrative expenses are used up over the same period in which they originate. In other words, period costs are related to the services consumed over the period in question.Product Costs

Period Costs

In a manufacturing organization, an important distinction exists between product costs and period costs.

Difference Between Product Costs and Period Costs FAQs

Product costs are all the costs that are related to producing a good or service. They are either direct materials, direct labor or factory overhead. These items are directly traceable or assignable to the product being manufactured. Product costs only become an expense when they are sold and become period costss. Period costss are all the costs that are expired non product costs. They are all the expenses/costs listed in a firm's income statement.

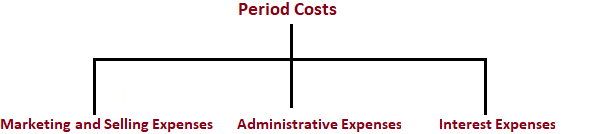

Period costs are expired non-product costs. They are identified with measured time intervals and not with goods or services. Period costs can be defined as any cost or expense items listed in the firm’s income statement. Examples of period costs include selling and administrative expenses. Both of these types of expenses are considered period costs because they are related to the services consumed over the period in question.

An example of a product cost would be the cost of raw materials used in the manufacturing process. Product costs also include Depreciation on plant, expired insurance on plant, production supervisor salaries, manufacturing supplies used, and plant maintenance.

The main benefit of classifying costs as either product or period is that it helps managers understand where their costs are being incurred and how those costs relate to the production process. This information can be used to make decisions about where to allocate resources and how to improve efficiency.

It is important to keep track of your total period cost because that information helps you determine the net income of your business for each accounting period.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.