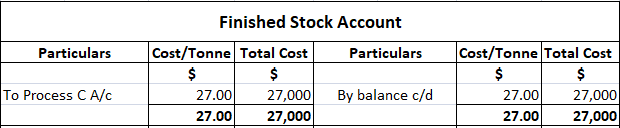

A process costing system accumulates the costs of a production process and assigns them to the products that the business outputs. A production report has to be made under the process costing system. Process costing is applied to determine the cost of production in industries where products pass through different phases of production before completion. Under process costing, there is a finished product at each stage. This becomes the raw material of the subsequent stage until the final stage of completion. Process costing is generally used in industries that deal with chemicals, distilled products, canned products, food products, oil refineries, edible oils, soap, paper, textiles, and others. Process costing refers to a type of costing procedure commonly adopted by factories. In process costing, there is continuous or mass production and ongoing costs, which are accumulated regularly. The following five conditions are favorable for the use of process costing: The main characteristics of process costing are: The following are the general principles of process costing: The main features of process costing include: To summarize, W. Big offered an informative remark: The author continued: Industries that may benefit from the use of process costing are: Under process costing, the procedure used to manufacture a product is divided into well-defined processes. A separate account is opened for each process to which all incurred costs are charged. The total number of units produced during a given period is calculated. By dividing the total cost of a process by the total number of units produced, the cost per unit can be obtained. The finished material of one process constitutes the raw material of the next. Therefore, as the finished material is transferred to the next process, the cost of each process is also transferred, until it ends in the finished stock account. Calculating the unit cost for any work performed during a period is a key part of a production report. A student's first thought is that this is easy—just divide the total cost by the number of units produced. However, the presence of work-in-process inventories causes problems. You cannot calculate the total output of the period by just taking the sum of completed units and work in process (ending inventory) because units in the work-in-process inventory are not 100% complete. This problem is handled through the concept of equivalent units of production. The process costing procedure is explained in more detail in the next example. A product passes through three processes: Process A, Process B, and Process C. 1,000 tons of the commodity were produced at the following costs: Required: Assume that there was no work-in-progress (i.e., not at the beginning or at the end). Show the process costs for each process and the total cost of the finished product. Cost per unit = Cost of input / Output = $6,000 / 1,000 tons = $6 per ton Cost per unit = $15,000 / 1,000 tons = $15 per ton Cost per unit = $27,000 / 1,000 tons = $27 per tonProcess Costing: Definition

Process Costing: Explanation

Characteristics of Process Costing

General Principles of Process Costing

Features of Process Costing

The fundamental principle involved in process cost accounts is simple. A separate account is opened for each process … to which all expenditure incurred thereon is charged.

When the process or operation has been completed, the partially worked out product is passed into a process stock account, from which it will be requisitioned as and when required by the next process; or it may become automatically the raw material of the next process and be charged to the process account immediately.

Use of Process Costing

Process Costing Procedure

Calculating Unit Cost Under Process Costing

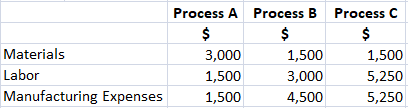

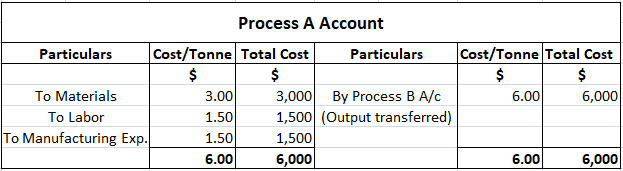

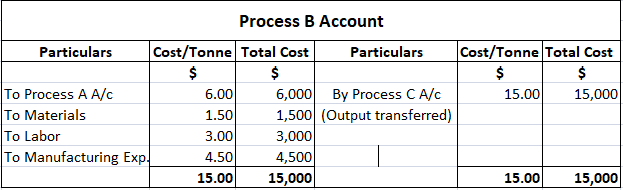

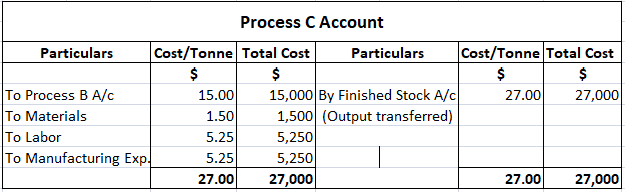

Example

Solution

Process Costing FAQs

Process Costing, also called job-order costing, assigns total manufacturing costs to the units being produced. Process Costing is a system of product cost allocation used in merchandising and industry. The main objective is to allocate total manufacturing costs to the various products according to the proportion of resources consumed by each product.

The main benefit of Process Costing is that it provides information that can be used to make critical business decisions. For example, managers using this system can assess profit margin by product and isolate problem products before they become major issues. Process Costing also allows companies to set prices according to production costs.

While both systems produce a cost of goods sold for a given period, Process Costing focuses on the product's progression through various stages of production. Job-order costing focuses on a specific product or service produced for a given customer. Process costs are expensed as incurred; job-order costs are capitalized. Process costs represent a higher level of accuracy than job-order costing, but they are also more complex and time consuming to develop.

Process Costing helps companies make critical decisions based on accurate information. It allows companies to track product cost performance by production location or department—information that can be used to help determine which products are most profitable.

Yes, many services are produced in a manner similar to manufacturing goods. For example, when an airline provides transportation for passengers the way it would produce any product.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.