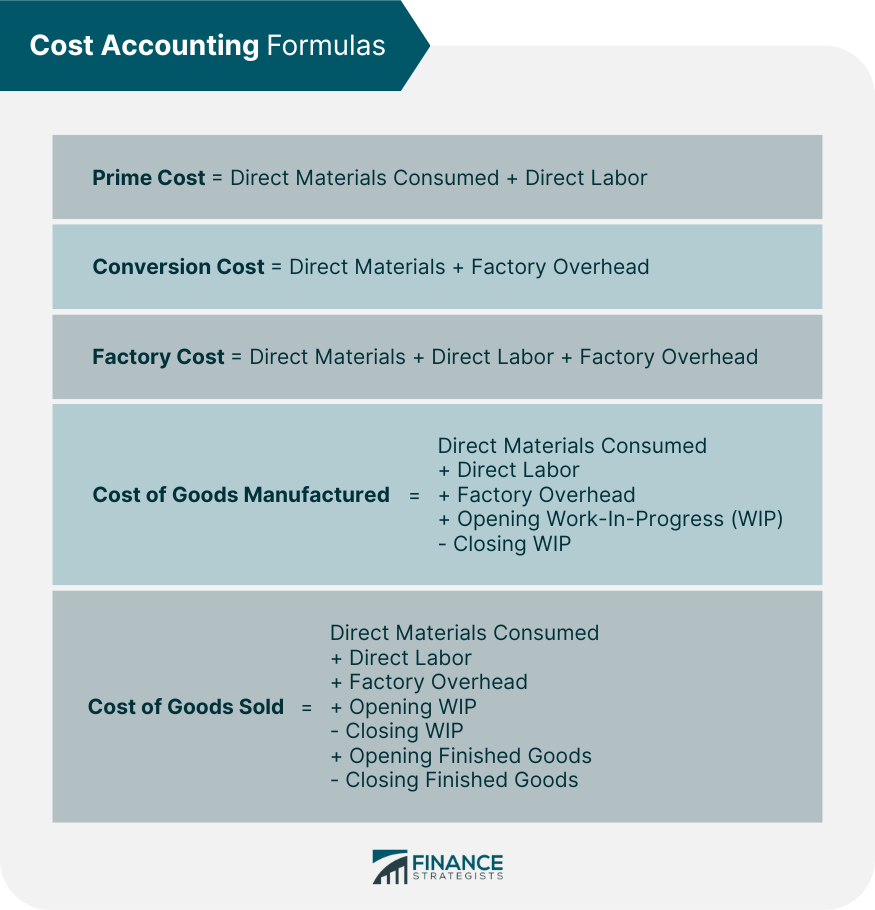

The following formulas are useful in cost accounting to determine different types of costs. Prime cost = Direct materials consumed + Direct labor Conversion cost = Direct materials + Factory overhead Factory cost = Direct materials + Direct labor + Factory overhead Cost of goods manufactured = Direct materials consumed + Direct labor + Factory overhead + Opening work-in-progress (WIP)- Closing WIP Cost of goods sold = Direct materials consumed + Direct labor + Factory overhead + Opening WIP - Closing WIP + Opening finished goods - Closing finished goods

Cost Accounting Formulas FAQs

Prime cost = direct materials consumed + direct labor

Conversion cost = direct materials + factory overhead

Factory cost = direct materials + direct labor + factory overhead

Cost of goods manufactured = direct materials consumed + direct labor + factory overhead + opening work-in-progress (wip)- closing wip

Cost of goods sold = direct materials consumed + direct labor + factory overhead + opening wip – closing wip + opening finished goods – closing finished goods

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.