The contribution margin ratio is the total contribution margin divided by total sales. It is also known as the profit-volume (P/V) ratio. The contribution margin is the amount of revenue in excess of variable costs. One way to express it is on a per-unit basis, such as standard price (SP) per unit less variable cost per unit. The contribution margin may also be expressed as a percentage of sales. When the contribution margin is expressed as a percentage of sales, it is called the contribution margin ratio or profit-volume ratio (P/V ratio). The contribution margin (or P/V) ratio is calculated as follows: Company X manufactures and sells only one product. The per-unit costs are: SP per unit = $30 VC per unit = $18 Contribution margin per unit = $12 The company reports fixed costs of $40,000. Required: Calculate the contribution margin ratio (or P/V ratio). P/V ratio = 30 - 18/30 = 40% A contribution margin ratio of 40% means that 40% of the revenue earned by Company X is available for the recovery of fixed costs and to contribute to profit. The remaining 60% is consumed by variable costs. The break-even point (BEP) is calculated using the contribution margin ratio. The formula is: BEP = Fixed costs / P/V ratio = 40,000 / 40% = $100,000 Conceptually, the contribution margin ratio reveals essential information about a manager's ability to control costs. This is especially true in relation to sales revenue. A firm's ability to make profits is also revealed by the P/V ratio. With a high contribution margin ratio, a firm makes greater profits when sales increase and more losses when sales decrease compared to a firm with a low ratio.Contribution Margin Ratio: Definition

Contribution Margin Ratio: Explanation

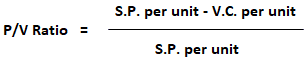

Formula to Calculate Contribution Margin Ratio

Example

Contribution Margin Ratio FAQs

The Contribution Margin Ratio is a measure of profitability that indicates how much each sales dollar contributes to covering fixed costs and producing profits. It is calculated by dividing the contribution margin per unit by the selling price per unit.

A high Contribution Margin Ratio indicates that each sale produces more profit than it did before and that the business will have an easier time making up fixed costs. A low Contribution Margin Ratio, on the other hand, suggests that there may be difficulty in covering fixed costs and making profits due to lower margins on individual sales.

A business can increase its Contribution Margin Ratio by reducing the cost of goods sold, increasing the selling price of products, or finding ways to reduce fixed costs.

Yes, the Contribution Margin Ratio is a useful measure of profitability as it indicates how much each sale contributes to covering fixed costs and producing profits.

Other financial metrics related to the Contribution Margin Ratio include the gross margin ratio, operating margin ratio, and net profit margin ratio. These ratios provide insight into the overall profitability of a business from different perspectives.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.