The contribution margin (CM) is the amount of revenue in excess of variable costs. To cover the company's fixed cost, this portion of the revenue is available. After all fixed costs have been covered, this provides an operating profit. Hence, CM is a profit measure, albeit an incomplete one. This is because fixed costs are not covered. However, when CM is expressed as a ratio or as a percentage of sales, it provides a sound alternative to the profit ratio. The difference between the selling price and variable cost is a contribution, which may also be known as gross margin. Variable cost refers to the marginal cost. In fact, both terms are synonymous. The contribution margin may also be expressed as fixed costs plus the amount of profit. In other words, we can say that: The following formula can be used to calculate the contribution margin: An alternative formula is as follows: Let's apply this formula in the next example. Assume that Company X manufactures and sells a single product. The various per unit costs are: Total fixed costs are $30,000 for the time period involved. Presently, the sales of the company are 100,000. Required: Calculate the break-even point (BEP) for Company X. The different formulas for calculating the break-even point (BEP) are:

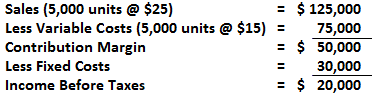

For the above question, the calculations are: 1. BEP in sales units BEP = 30,000 / 10 = 3,000 units 2. BEP in sales percentage Selling price per unit = $25 (100%) Variable cost per unit = $15 (60) Contribution margin per unit = $10 (40%) 3. BEP in sales ($) = 30,000 / 40% = $75,000 The break-even point in dollar terms can also be expressed as: = 25 x 3,000 = $75,000 Each unit sold contributes $10 to cover fixed costs and profits. The break-even point (BEP) for Company X is 3,000 units. If the company realizes a level of activity of more than 3,000 units, a profit will result; if less, a loss will be incurred. Profits will equal the number of units sold in excess of 3,000 units multiplied by the unit contribution margin. Thus, at the 5,000 unit level, there is a profit of $20,000 (2,000 units above break-even point x $10).Contribution Margin: Definition

Contribution Margin: Explanation

Formula For Contribution Margin

Contribution margin = Sales revenue – Variable expenses

Contribution margin = Fixed cost + Profit

Example

Solution

BEP in sales $ = SP per unit x BEP in units

Interpretation

Contribution Margin FAQs

The difference between the selling price and variable cost is a contribution, which may also be known as gross margin. Variable cost refers to the marginal cost. In fact, both terms are synonymous. Hence, CM can be explained as fixed costs plus profit.

The break even point (BEP) is the number of units at which total revenue (selling price per unit) equals total cost (fixed costs + variable cost). Although, fixed costs are not covered. BEP is an important concept in analysis of business viability. If the selling price per unit is more than the variable cost, it will be a profitable venture otherwise it will result in loss.

There is no definitive answer to this question, as it will vary depending on the specific business and its operating costs. However, a general rule of thumb is that a Contribution Margin above 20% is considered good, while anything below 10% is considered to be relatively low.

Break even point (BEP) refers to the activity level at which total revenue equals total cost. Contribution margin is the variable expenses plus some part of fixed costs which is covered. Thus, CM is the variable expense plus profit which will incur if any activity takes place over and above BEP.

The contribution margin is calculated as the difference between the selling price and the variable costs. This measures how much money is generated from each unit sold after deducting the costs associated with producing and selling that unit.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.