A comparative study of process and job costing will help to understand both systems more effectively. A summary of their differences is given below.Process Costing

Job Costing

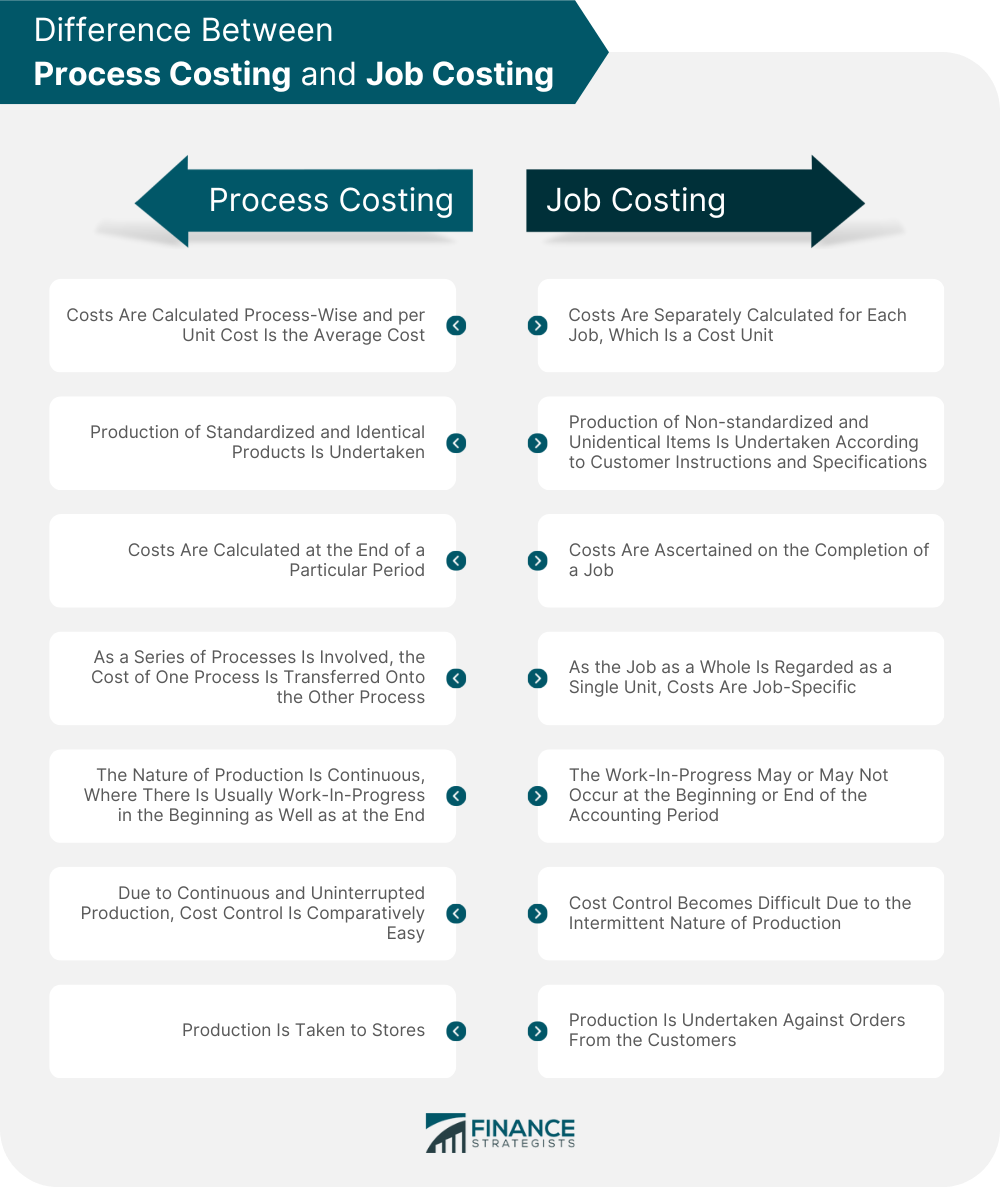

1. Costs are calculated process-wise and per unit cost is the average cost (ascertained by dividing the total cost of the process by the number of units produced) 1. Costs are separately calculated for each job, which is a cost unit 2. Production of standardized and identical products is undertaken 2. Production of non-standardized and unidentical items is undertaken according to customer instructions and specifications 3. Costs are calculated at the end of a particular period 3. Costs are ascertained on the completion of a job 4. As a series of processes is involved, the cost of one process is transferred onto the other process 4. As the job as a whole is regarded as a single unit, costs are job-specific 5. The nature of production is continuous, where there is usually work-in-progress in the beginning as well as at the end 5. The work-in-progress may or may not occur at the beginning or end of the accounting period 6. Due to continuous and uninterrupted production, cost control is comparatively easy 6. Cost control becomes difficult due to the intermittent nature of production 7. Production is taken to stores 7. Production is undertaken against orders from the customers

Difference Between Process Costing and Job Costing FAQs

Process Costing calculates costs at a particular stage of production whereas job cost accounts for each completed work order.

Both methods follow the same convention of charging direct material, direct labour and factory overhead to production accounts (common pool).

Total Standard Costs ÷ Equivalent Units = Equivalent Cost Per Unit

There are 5 kinds of costs, namely: product costs, period costs, inventoriable costs, non-inventory holding costs and reported costs.

Product or period costs can be inventoriable under Process Costing.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.