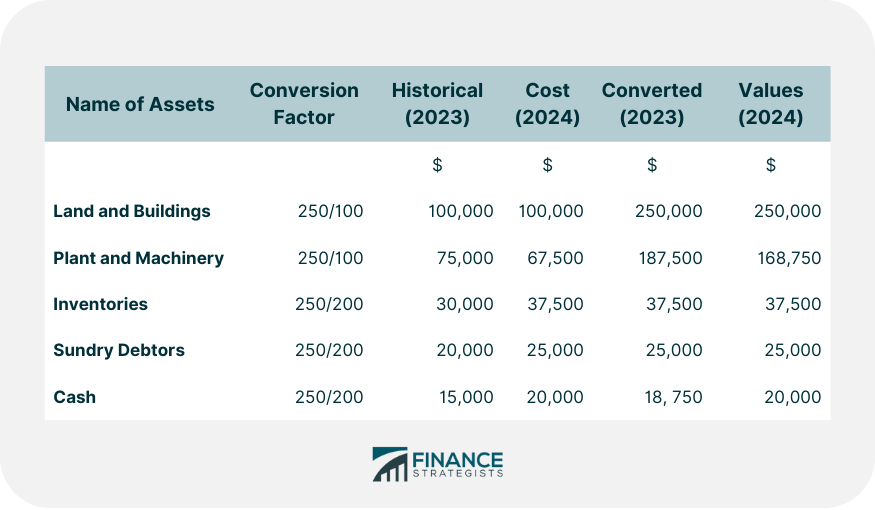

Under the current value accounting method, all assets and liabilities are shown in the balance sheet at their current values. The difference in the value of net assets at the start and end of the year is known either as profit or loss. Significantly, determining current values is not a straightforward task. Required: Prepare the following: Conversion of Assets at Current Values (2024 Index) Sundry Creditors: 250/200, 25,000, 30,000, 31,250, 30,000 Calculation of loss for holding current assets = 81,250 - 65,000 = $16,250 Calculation of gain from current liabilities From Sundry Creditors (Current Value - Historical Values) = 31,250 - 25,000 = $6,250 Net loss from holding current assets and current liabilities = 16,250 - 6,250 = $10,000Example

The general index was 100 in 2014 (i.e., the base year). It was 200 in 2023 and 250 in 2024. No dividend was paid in 2024.

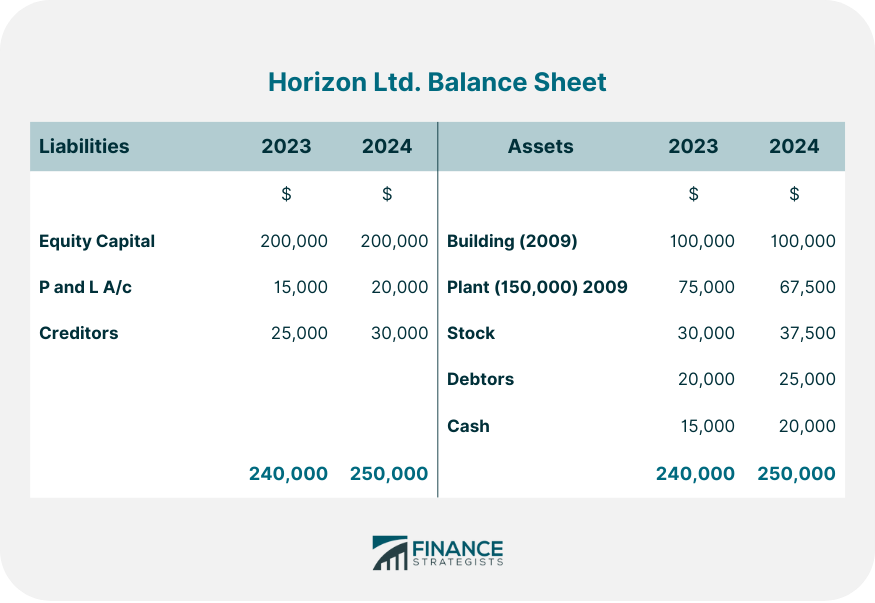

Solution

Conversion of liabilities at current value 2024

Loss = Current values - Historical values of current assets

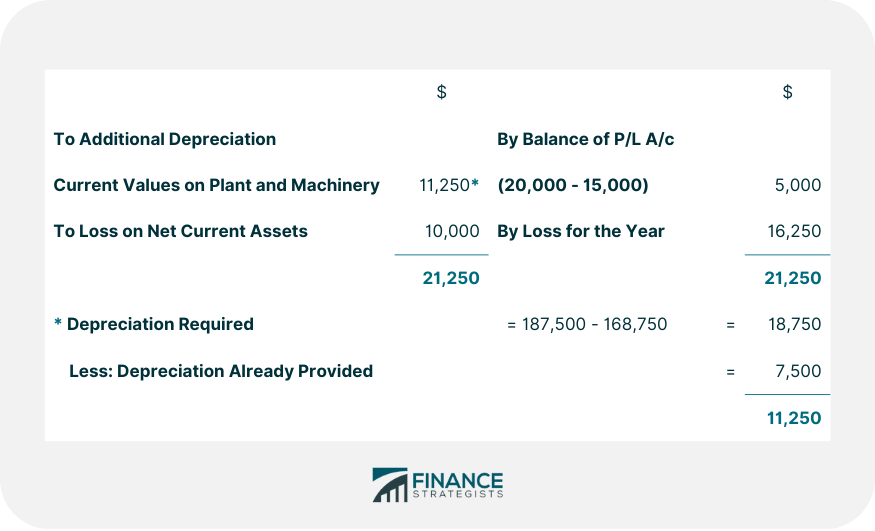

Supplementary Income Statement at Current Values

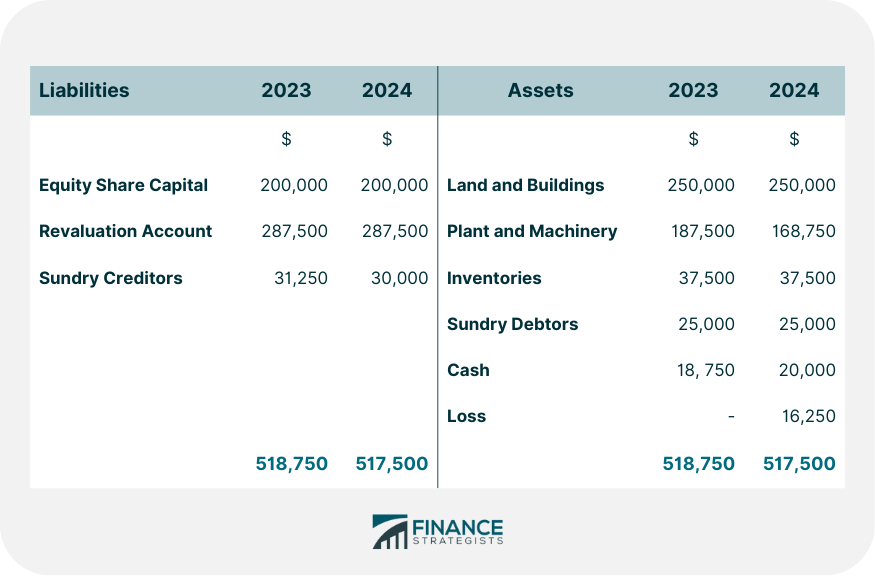

Supplementary Comparative Balance Sheet at Current Values

Current Value Accounting Technique FAQs

Under the current value accounting method, all assets and liabilities are shown in the balance sheet at their current values. The difference in the value of net assets at the start and end of the year is known either as profit or loss. Significantly, determining current values is not a straightforward task.

The current value accounting method is used because it provides a more accurate picture of a company's financial position. It takes into account changes in market conditions, which can impact the value of assets and liabilities.

This can be done in a number of ways, depending on the type of asset or liability. Some assets, such as land and buildings, may be valued at their current market value. Other assets, such as cash and investments, may be converted to their current value by using an appropriate index. Liabilities may be converted to their current value by multiplying them by a conversion factor.

Under historical Cost Accounting, assets and liabilities are shown at their original costs. The values on the balance sheet will not change over time. Under current value accounting, assets and liabilities are shown at their current values. Their values will change as market conditions change. This provides a more accurate picture of a company's financial position.

The main benefit of using the current value accounting method is that it provides a more accurate picture of a company's financial position. It takes into account changes in market conditions, which can impact the value of assets and liabilities. This can be especially important in times of economic turmoil, when the market value of assets may be more volatile.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.