Last in, First Out (LIFO) is an inventory costing method that assumes the costs of the most recent purchases are the costs of the first item sold. The LIFO method, which applies valuation to a firm's inventory, involves charging the materials used in a job or process at the price of the last units purchased. In other words, under the LIFO method, the cost of the most recent lot of materials purchased is charged until the lot is exhausted. After this, the price of the next most recent lot is charged to the job, department, or process. This results in leaving an old lot of materials in hand. When materials are returned from the factory to the storeroom, they should be treated as the most recent stock on hand. They should be entered in the materials ledger card balance below all of the units on hand, at the same price as they were when issued to the factory. In terms of the flow of cost, the principle that LIFO follows is the opposite compared to FIFO. LIFO assumes that the last cost received in stores is the first cost that goes out from stores. The cost of materials is charged to production in the reverse order of purchases. The later costs recorded on the materials ledger cards are used for costing materials requisitions, and the balance consists of units received earlier. The following are the main advantages of the LIFO method of inventory valuation: The LIFO method of inventory valuation suffers from the following major drawbacks: Consider the following information: Required: Show the value of the inventory on hand on 30 April using the LIFO method. Several problems related to LIFO limit its effectiveness. Some of the more important problems include the effects of prices, LIFO liquidation, purchase behavior, and inventory turnover. When prices decrease, LIFO shows higher earnings and, as a result, higher taxes. This is because the latest and, in this case, the lowest prices are allocated to the cost of goods sold. In some industries, prices are volatile and thus unpredictable. For example, in 2018, a number of sugar companies changed to LIFO as sugar prices rose at a rapid pace. By switching to LIFO, they reduced their taxable income and their tax payments. However, in 2019, sugar prices declined. The result of this decline was an increase in earnings and tax payments over what they would have been on a FIFO basis. The potential of LIFO liquidation is a major concern to LIFO users. As noted already, at least a portion of the inventories valued under LIFO is priced at the firm's early purchase prices; this might go back to the date when LIFO was adopted. LIFO liquidation occurs when a firm sells more units than it purchases in any year. Thus, LIFO layers that have been built up in the past are liquidated (i.e., included in the cost of goods sold for the current period). In effect, a firm is apt to sell units that may have 2000 or 2010 costs attached to them. The result is a lower cost of goods sold, higher gross margin, and higher taxes. Although firms can often plan for LIFO liquidation, events sometimes happen that are beyond the control of management. For example, a supplier's strike or unanticipated demand can cause unplanned LIFO liquidation. As an example, Revere Copper and Brass Incorporated reported the following in its 2018 annual report. During 2018, inventory quantities were reduced, resulting in the liquidation of certain LIFO inventory layers carried at costs that were lower than the cost of current purchases. The effect of this was to increase net income by approximately $1,772,000 or $0.31 per share, including $1,443,000 or $0.25 per share in the fourth quarter. These amounts represented around 8% of net income and earnings per share. The use of LIFO, especially in connection with the periodic inventory method, offers management a level of flexibility to manipulate profits. Although the is not problematic from the point of view of managers, critics of LIFO point to this as a disadvantage of LIFO. In any case, by timing purchases at the end of the year, management can determine what costs will be allocated to the cost of goods. It is worth remembering that under LIFO, the latest purchases will be included in the cost of goods sold. Therefore, by making purchases at year-end, the cost of any purchase will be included in the cost of goods sold. Purchases at the beginning of the next year, however, could end up in next year's ending inventory as a new LIFO layer. This will happen if the units purchased during this year exceed the units sold. Inventory turnover is the rate at which a company sells its inventory. Inventory turnover can influence the differential between FIFO and LIFO. When a company has a high turnover rate, the advantage of LIFO over FIFO is not massive. This is because, with a high turnover rate, a FIFO-based cost of goods will approximate a LIFO-based or current-cost cost of goods sold. Therefore, the inventory profits usually found in connection with FIFO are substantially decreased. In summary, choosing principles of accounting that can guide both financial reporting and tax strategy is an important management decision. In the LIFO versus FIFO case, it is even more important because of the LIFO conformity rule. According to this rule, management is forced to consider the utility of increased cash flows versus the effect LIFO will have on the balance sheet and income statement.Last In, First Out (LIFO): Definition

LIFO Method of Inventory Valuation: Explanation

Advantages of LIFO

Disadvantages of LIFO

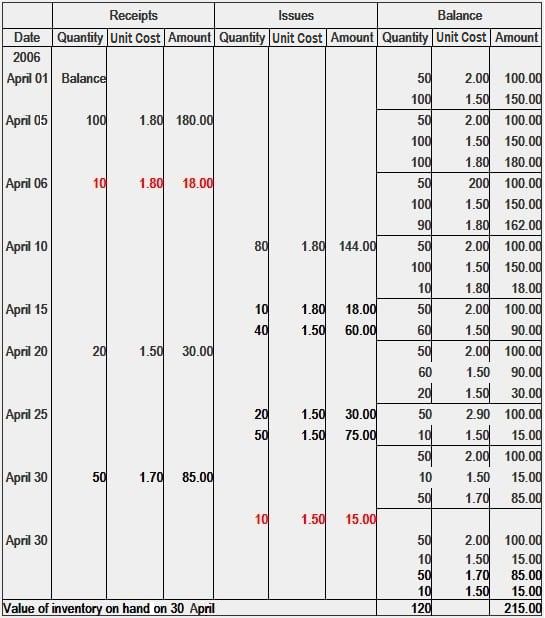

Example

Solution

Problems Related to the LIFO Method

Falling Prices

LIFO Liquidation

Purchase Behavior

Inventory Turnover

Last In, First Out (LIFO) Method Problem and Solution FAQs

LIFO is an inventory management system in which the items most recently added to a company's stock are the first ones to be sold or used.

With LIFO, when a new item arrives on the shelf it will replace the oldest item of that type and be sold or used first. This helps companies keep their stock up-to-date with current products and customer demand.

Using LIFO can help prevent obsolescence by ensuring out-of-date items are sold or used before they become obsolete. Additionally, it helps companies better manage their stock levels and ensure they have the most current products available.

One potential downside to LIFO is that it can lead to higher inventory costs as old items must be replaced frequently. Additionally, businesses may not be able to take advantage of bulk discounts since only a few items are purchased at a time.

LIFO is best suited for situations in which inventory needs to remain up-to-date and turnover is high, such as in retail stores or warehouses. It is not recommended for situations where stock needs to remain consistent or bulk discounts are available.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.