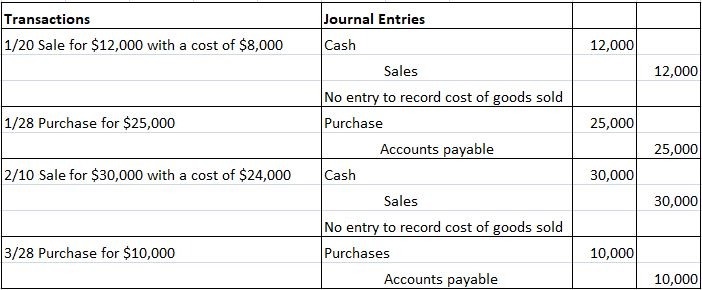

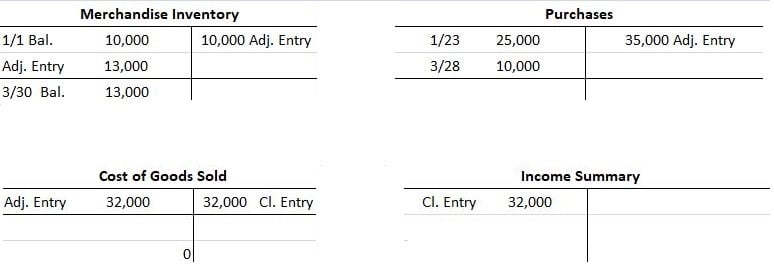

A periodic inventory system does not keep continuous track of ending inventories and the cost of goods sold. Instead, these items are determined at the end of each quarter, year, or accounting period. Although this method offers ease of use for record-keeping, it hinders the managerial decision-making process. However, the sheer volume of transactions in some merchandising businesses makes it impossible to use anything but the periodic system. The example below shows the journal entries necessary to record inventories under the periodic system. The information from the example data illustrates the perpetual inventory method. The periodic method does not record the cost of the inventory sold for a particular sale. Furthermore, as the journal entries show, inventory purchases are not debited to the merchandise inventory account. Instead, they accumulate in a separate purchases account. Consequently, there are no merchandise inventory account entries during the period. Therefore, before any adjusting entries, the balance in the merchandise inventory account will reflect the amount of inventory at the beginning of the year, as indicated in the following T-accounts. Preparing financial statements under the periodic inventory system means calculating the cost of goods sold during the period and the ending inventory. This process involves taking a physical inventory or counting the end-of-period inventory to determine the quantity and the cost of the ending inventory and then applying this formula (the data is from the current example): The total of the beginning inventory and purchases during the period represents all the firm's goods available for sale. After subtracting the ending inventory from this total, the remaining balance represents the cost of the items sold. Determining the cost of the ending inventory and the cost of goods sold helps determine the periodic income and financial position. Journal entries record the resulting figures. Once the ending inventory and cost of goods sold are clarified, the accounts require adjustment to reflect the ending inventory balance and the cost of goods sold. There are several ways to do this, but we recommend making the following adjusting and closing entries: The adjusting entry is based on the formula to calculate the cost of goods sold. Thus, the purchases and merchandise inventory (beginning) are added together and represent goods available for sale. The debit, merchandise inventory (ending), is subtracted from that total to determine the balancing debit to the cost of goods sold. For convenience, merchandise inventory is labeled beginning and ending. However, there is only one ledger account: merchandise inventory. Note that this adjusting entry adjusts the merchandise inventory account to its proper ending balance in order to zero out the purchases account and create a cost of goods sold account. The entry to close the cost of goods sold is like all entries to close expense accounts. After the adjusting and closing entries have been posted, the T-accounts appear as follows: The following closing entry offers an alternative method to record the ending inventory and to determine the cost of goods sold: Although this method requires one less entry, the cost of goods sold is not specifically determined. However, this account is necessary to prepare the income statement.What Is a Periodic Inventory System?

Accounting Under the Periodic Inventory System: Journal Entries

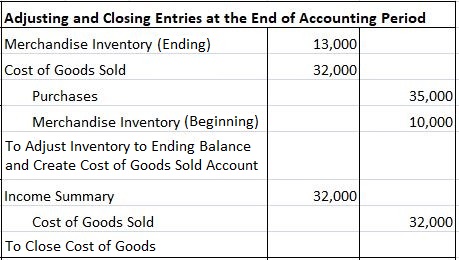

Determining Cost of Goods Sold and Ending Inventory

Adjusting and Closing Entries Under the Periodic Inventory Method

Periodic Inventory System FAQs

A periodic inventory system does not keep continuous track of ending inventories and the cost of goods sold. Instead, these items are determined at the end of each quarter, year, or accounting period.

Determining the cost of the ending inventory and the cost of goods sold helps determine the periodic income and financial position. Journal entries record the resulting figures.

The adjusting entry is based on the formula to calculate the cost of goods sold. Thus, the purchases and merchandise inventory (beginning) are added together and represent goods available for sale.

The debit, merchandise inventory (ending), is subtracted from that total to determine the balancing debit to the cost of goods sold. For convenience, merchandise inventory is labeled beginning and ending. However, there is only one ledger account: merchandise inventory.

The periodic method does not record the cost of the inventory sold for a particular sale.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.