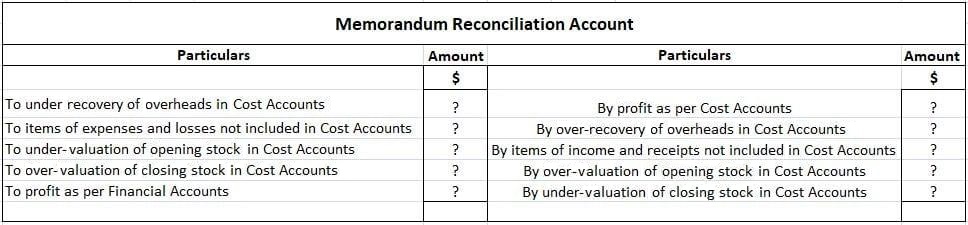

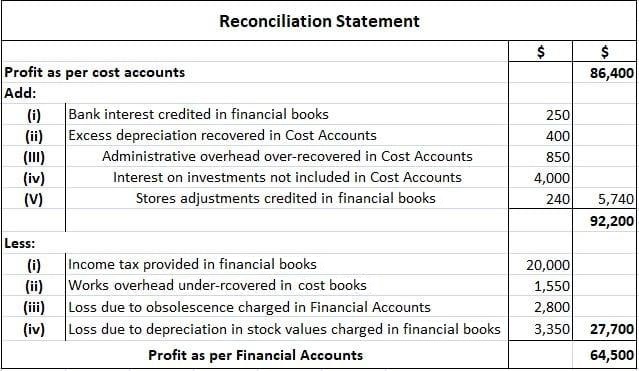

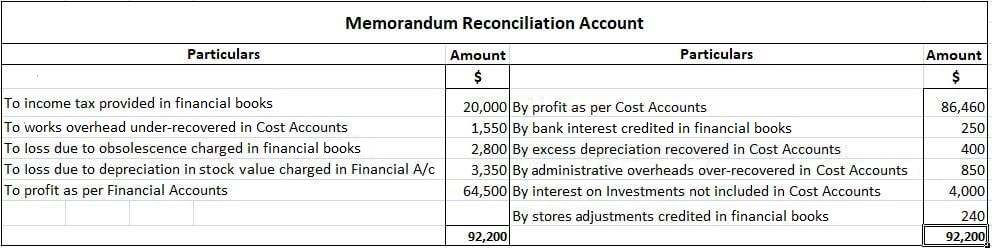

The reconciliation of cost and financial accounts can also be presented in the form of an account prepared on a memorandum basis. Such an account is known as a memorandum reconciliation account. The amount of profit as per cost accounts is shown on the credit side of this account. Also, the various items to be added to the profit as per cost accounts are credited to this account, and the items to be deducted from profit as per cost accounts are debited to it. The difference between the two sides of the account will reveal the amount of profit or loss as per the financial accounts. A specimen of the memorandum reconciliation account is presented below. The net profits of a manufacturing company were shown in the financial records as $64,500 for the year ended 31 March 2019. The cost books, however, showed a net profit of $86,460 for the same period. Careful scrutiny of the figures from both the sets of accounts revealed the following facts: Required: Prepare the following: 1. 2.What Is a Memorandum Reconciliation Account?

Specimen of Memorandum Reconciliation Account

Example

Solution

Memorandum Reconciliation Account FAQs

A financial reconciliation statement reconciles the totals of the cost account with those of the financial accounts. It shows whether there is any divergence between the two sets of books, and if so, how such divergence occurred. On the other hand, a memorandum reconciliation account is a detailed account which reconciles the profits as per the cost books with those as per the financial books.

The main purpose of preparing a memorandum reconciliation account is to identify and quantify all the differences between the profits as per the two sets of accounts. This helps in understanding the reasons behind any discrepancies that may have arisen between the two sets of books.

No, not all differences between the profits as per the two sets of accounts are highlighted in a memorandum reconciliation account. Only those differences which have a significant impact on the bottom-line profit are shown in this account. Any minor discrepancies between the two sets of accounts are ignored.

A memorandum reconciliation account is prepared by taking into account the total profits as per the cost books and the total profits as per the financial books. All the differences between the two sets of accounts are identified and accounted for in this account.

The formula for preparing a memorandum reconciliation account is as follows: total profit as per cost books = total profit as per financial books - differences

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.