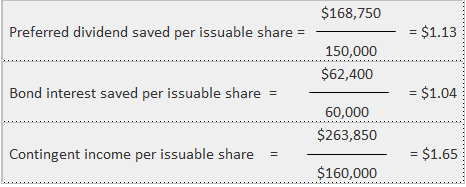

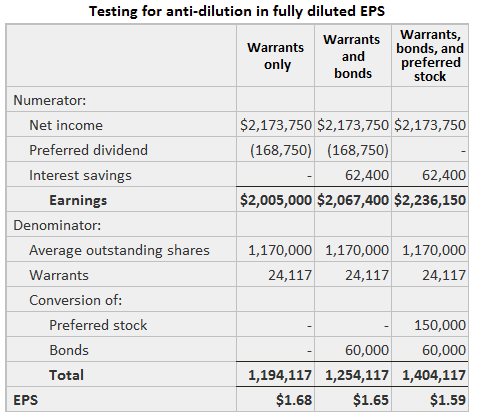

Although primary earnings per share (EPS) is less than simple EPS, and fully diluted EPS is less than primary EPS, additional testing must be done to assure that maximum dilution has occurred. Anti-dilutive securities should be excluded from calculations. The only potentially anti-dilutive securities that influence the calculation of primary EPS are bonds. The interest savings per issuable common share are $1.04, which was found by dividing the total savings ($62,400) by the number of issuable shares (60,000). This result is far below primary EPS without it ($1.68). The second number above was found by dividing the earnings adjusted for preferred dividends ($2,005,000) by 1,191,726 (the number of outstanding shares plus the net number issuable from warrants). Thus, the bonds are dilutive for primary EPS. The identification of anti-dilutive effects in fully diluted EPS is more complicated than in primary EPS because there are three factors to consider: The first phase is to calculate the additional earnings per issuable share of each of them. These results are shown below. The EPS result before considering these factors is $1.68, which is found by dividing the adjusted reported income by the number of outstanding shares plus shares issuable from the warrants (1,194,117), as shown in the example below. Thus, none of the three is obviously anti-dilutive and the next phase must be performed. At this stage, each security is included in the calculation in order of most to least dilutive. The first step includes the bonds. The numerator equals the $2,005,000 seen above plus $62,400 of interest savings. The denominator is the 1,194,117 seen above plus 60,000 shares. The result is $1.65 per share, as shown in the second column of the above example. At the next step, the preferred dividends saving per share ($1.13) is seen to be dilutive of the $1.65 EPS from step 1. Thus, it should be included. The calculations are shown in the third column of the above example. The numerator is not adjusted for preferred dividends paid and the denominator is increased by the 150,000 shares of common that would be issued. The result is $1.59 per share. The third step is the comparison of this result with the additional EPS provided by the contingent agreement ($1.65). Since its effect per share is greater than $1.59, the agreement is anti-dilutive and it should be omitted. As confirmation, observe that the $1.59 is lower than the preliminary result of $1.60 seen in the above example. Before determining what EPS disclosures are to be provided, these preliminary results must be tested for the materiality of the dilution. The test shows that fully diluted EPS ($1.59) is only 93% of simple EPS ($1.71). Therefore, in this case, the company in question must report both primary and fully diluted EPS.Primary EPS

Fully Diluted EPS

Materiality Test

Anti-Dilution and Primary and Diluted Earnings Per Share FAQs

A contingent agreement is considered anti-dilutive if its effect per share would be less than fully diluted EPS. If it was more, then the additional shares would be dilutive to the EPS number.

There are two cases in which a company must disclose both primary and fully diluted EPS: (1) when the company has an available conversion privilege on its convertible securities and (2) when the average market price of the common stock was below the exercise price of those securities. In cases one and two, adjusted EPS is higher than basic EPS, which results in a slight dilution of earnings per share.

Preferred dividends are not considered anti-dilutive when they pay an amount equal to or less than the same stockholder's portion of income before preferred dividends divided by basic earnings per share.

Yes, you must show both numbers. Fully diluted EPS will always be adjusted for any convertible Debentures and warrants that could come due.

Investors should be able to tell if their earnings are being diluted by these securities. This calculation is used to show that number, but it also uses the potential shares that could result from exercising the convertible security.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.