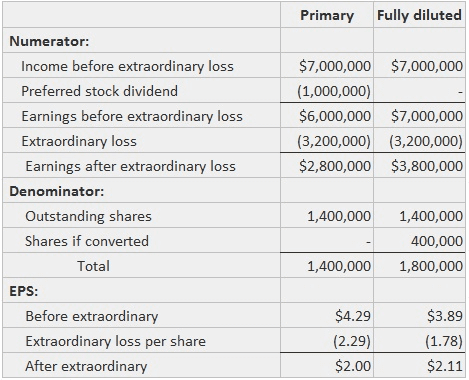

When calculating earnings per share (EPS), including the effects of a potentially dilutive security sometimes produces a higher per-share figure. This effect is known as anti-dilution. In this article, three aspects of anti-dilution are discussed in more detail. Under certain conditions, it is possible that the savings per share from a potentially dilutive security may be less than the EPS before extraordinary items but greater than the EPS after extraordinary items. Despite this result, the anti-dilutive security should be included in the calculation of a fully diluted EPS. Suppose that the Sample Company reports $7,000,000 as ordinary income and an extraordinary loss of $3,200,000. It has an issue of preferred stock on which it paid $1,000,000 of dividends, and which is convertible to 400,000 common shares. The preferred stock is not considered to be equivalent to the common stock. If there were 1,400,000 outstanding common shares, EPS calculations would be made as shown in the table below. Despite the fact that the fully diluted EPS is larger than the primary EPS, both results must be disclosed. When an ordinary loss occurs in a year, all potential savings from conversions and all potential increases in the number of shares are anti-dilutive. This is because the loss per share is reduced when they are included. That is to say, the fully diluted loss per share would be smaller than the primary loss per share, and this result would not be consistent with the worst-case assumption. Suppose that the Sample Company has a $7,000,000 operating loss and 1,400,000 outstanding shares, such that there is a $5 loss per share. If warrants equivalent to 100,000 common shares are outstanding, including them would change the result to $7,000,000 / 1,500,000, or a loss of only $4.67 per share. If bonds convertible to 200,000 shares can offer interest savings of $400,000, the result would be $6,600,000 / 1,600,000, or a loss of $4.13 per share. Therefore, neither of these potentially dilutive securities (or any others) would be included in the calculation of EPS, even if they were common stock equivalents. When more than two potentially dilutive securities exist, anti-dilutive effects can be harder to detect. The easiest approach to obtaining the most diluted EPS involves ranking the securities from most to least dilutive in terms of the savings per common share that would have been achieved if the shares had been issued. Then, each is brought into the calculation of primary or fully diluted EPS until it is reduced to the smallest possible figure. To demonstrate, assume that the Sample Company has reported a net income of $1,000,000 divided among 100,000 shares, adjusted for common stock equivalents. Further, suppose that the following convertible bonds are outstanding: Each of the bonds, as well as all of the bonds together, appears to be dilutive of the $10 primary EPS. If all of them are included, the EPS is $1,715,000 / 370,000, or $4.64, per share. To determine if this point is maximum dilution, alternate calculations can be made. These calculations involve bringing in the savings and new shares in order from the most to the least dilutive. Including only group A produces the result of $1,080,000 / 180,000, or $6, per share. This number is still larger than the total figure and the next group can be brought in. Group B will be dilutive because its saving per share ($1.25) is less than the last diluted EPS result. Including it produces $1,205,000 / 280,000, or $4.30, per share. Group C will not be dilutive because its savings per share of $4.50 is larger than the $4.30 just obtained. Thus, the $4.30 figure is the smallest fully diluted figure and should be reported on Sample's income statement. As verification, including groups A, B, and C produces $1,385,000 / 320,000, or $4.33.Definition and Explanation

Opposite Effects on EPS Before and After Extraordinary Items

Example

Losses

Example

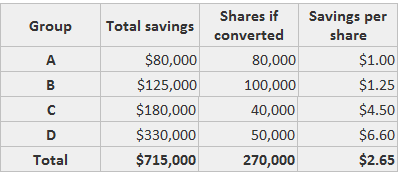

Multiple Dilutive Securities

Example

Anti-Dilutive Securities and EPS FAQs

The primary eps is the net income divided by the number of shares outstanding at the end of a reporting period. It is not adjusted for stock equivalents (such as options, warrants, and convertible securities).

Diluted eps takes into account all stock equivalents outstanding during a reporting period.

If stock equivalents are potentially dilutive, they are added together to form the stock equivalent units (seu). These seus are then included in the calculation of eps until it is reduced to the smallest possible number. The seus will be entered into this calculation according to priority level. That is to say, the worst anti-dilutive unit will be entered into the calculation first. If multiple units are equally bad, they are all entered in at once.

Stock equivalents potentially dilute eps when they provide a mechanism by which net income may be distributed to shareholders in the form of dividends or share repurchases.

If certain securities are potentially dilutive but have no value to the investor, they are considered "anti-dilutive" and are removed from the diluted eps calculation. The calculation of diluted eps may also be complicated or confusing if there are many possible security types. It also becomes more difficult to determine the number of shares outstanding at a given time as more security types are introduced.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.