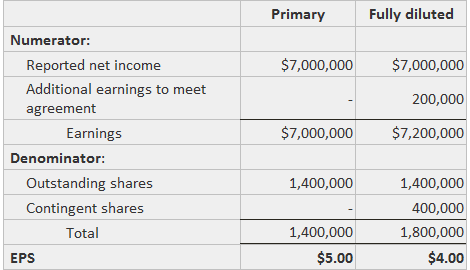

Under various circumstances, a firm may enter into a contingent issuance agreement that calls for the issuance of shares if stated future events occur. Common examples are compensatory stock plans that do not require a cash contribution and agreements for the purchase of an existing company through the issuance of shares. The treatment of these contingency agreements for earnings per share (EPS) depends on the nature of the future events and the perceived likelihood of their occurrence. If it appears from present conditions that the future event will occur, the shares are included in the denominator for both primary and fully diluted EPS. If the future event is a higher level of earnings than is presently being attained, the shares are included only in the fully diluted denominator, but the numerator is adjusted upward to the level necessary to achieve the issuance of the shares. This situation clearly demonstrates how the EPS number is typically a pro forma result rather than a description of actual performance. A contingent issuance agreement is considered anti-dilutive if the addition to earnings divided by the number of issuable shares exceeds EPS without considering the agreement. Suppose that Sample Company's reported earnings for 2021 are $7,000,000 and that the weighted average of outstanding shares is 1,400,000. There exists a contingent issuance agreement such that 400,000 shares will be issued if earnings reach $7,200,000. Because the earnings requirement has not yet been met, the contingent shares are included only in fully diluted EPS. In that calculation, $200,000 of hypothetical earnings must be added to the actual earnings in the numerator. The calculations are shown below.Definition and Explanation

Example

Contingent Issuance Agreements FAQs

Contingent issuance agreements are entered between two parties (e.g. company and investor) where one party is to receive shares of common stock in the company if certain conditions are met (e.g. earnings per share).

If the conditions are met, the issuance of shares will reduce earnings per share. However, if the conditions are not met then EPS will increase.

Common examples include compensatory stock plans that do not require a cash contribution and agreements for the purchase of an existing company through the issuance of shares.

An example is when a company enters into an agreement to issue shares of common stock to an investor if the company achieves a certain amount of income within a year.

Yes, if it appears from present conditions that the future event will not occur, then the shares are included only in fully diluted earnings per share.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.