Entrepreneurship entails a lot of risk for investors. Investors know that without risks, there would be no rewards, but brilliant investors do not take any chance by investing in a company they are unsure about. Earnings per share is an extremely vital business statistic used to entice, persuade, and demonstrate to investors the advantages of putting their money into a particular firm. Earnings per share detail a company's progress during one year and is an important benchmark for investors when judging risk. Earnings per share (EPS) tells investors how profitable a company is. It is calculated by dividing the net profit by the outstanding shares of common stock. A high EPS means that investing in the company would be profitable; a low EPS indicates that it would not yield much return. For individuals who are unfamiliar with the term "professional business register," it is critical to define such terms as "earnings" and "shares." At the end of a quarter or fiscal year, a company's earnings are what remain of its revenue after all costs have been subtracted. This net profit is sometimes referred to as the bottom line or simply profit. It is one of the most important pieces of financial information about a company because it signals whether that business is making money or running at a loss. The earnings reports for public companies play a significant role in setting their stock prices on exchanges. Owning a share in a company gives you equity, or ownership interest, in the business. This means that as a shareholder, you are entitled to part of the company's profits through dividends and increased value if the company's overall worth rises. People who own shares are called shareholders. Shares are also commonly known as stocks. Investing in the stock market is a lucrative way of life that can enable people who are not ready to start their own businesses to profit from existing firms. Most individuals with enough idle cash to invest are hesitant since they are unsure which company to invest in. In a corporation, there are several kinds of shares, each with its own set of rights. Furthermore, various types of shares are accessible to different corporate and non-profit organizations. Some shares may be acquired by public members, whereas others are only available to certain people in the company. In the following sections, we will look at the sorts of stock and earnings per share companies offer. A shareholder, as previously defined, has a stake in the company and owns shares. A person who owns shares in a firm is referred to as a shareholder. There are two distinct sorts of shares: common shares and preference/preferred shares. Common shares are types of stocks that show partial ownership in a company. In other words, somebody who owns one or more common shares is part-owner of the corporation which issued those shares. Common shareholders have voting rights to elect the Board of Directors and pass (or reject) corporate policies brought to vote by shareowners. From an investment standpoint, common stockholders usually profit more handsomely in the long run. The risk of holding common stock in a business is that the general shareholders are the last to be reimbursed or to claim the company's assets if it goes bankrupt. This implies that before common shareholders can claim the assets in a company, bondholders, preferred shareholders, employees, and creditors must be repaid completely. If a firm goes bankrupt due to bankruptcy, common stockholders receive nothing. If a company ever has to liquidate, common shareholders are the last group of people who can make claims. They are also the last ones to receive dividends. In other words, before common shareholders get any profit, dividend payments have already been sent to preferred shareholders. Because of their right to vote for corporate policies and elect board members, common shares are also known as ordinary shares or voting shares. Preferred shares, as the name implies, give preference to preferred shareholders and pay them dividends before common ones. If a firm goes bankrupt, preferred stockholders receive payment before ordinary stockholders. Because they are generally entitled to a certain dividend and are reimbursed in the event of a company's collapse, preferred stockholders have less risk than common stockholders. Preferred shares, on the other hand, provide preferred shareholders with no voting rights. This implies that preferred shareholders do not have the ability to vote for the board of directors or a corporate policy. Preferred shares are classified into cumulative preferred, non-cumulative, participating preferred, and convertible preferred stocks. Holders of cumulative preferred shares are entitled to be paid current and past dividends (dividends in arrears) that the common shareholders have not paid. The cumulative preferred stock dividends accumulate, just as the name implies, and they cannot be lost until they are paid in full. If a shareholder is not paid on time, preferred shares allow for that person to still receive their full dividend payment, including any missed or previous payments. Oftentimes, those who hold a preferred cumulative share are given some form of compensation for the unreasonable delay in receiving their dividends. The dividends of a cumulative preferred share are calculated as follows. A cumulative preferred share is sometimes referred to as a guaranteed share because shareholders are ensured of receiving all their dividends. A non-cumulative preferred share differs from a cumulative one in that if the company does not pay out dividends for a quarter or year, a non-cumulative preferred investor cannot claim unpaid dividends while receiving current ones. This implies that noncumulative shareholders do not build up over time as cumulative preferred investors pay dividends in arrears. Shareholders of participating preferred shares receive dividends that match the specified rate of regular preferred dividends and an additional sum based on a pre-existing condition. This extra amount is generally given to shareholders if the dividend payments made to common shareholders surpass the agreed amount set initially. If the firm is dissolved, investors who hold preferred shares will be reimbursed the amount they paid for the shares. As the name suggests, convertible preferred shares can be transformed into common shares if the shareholder desires. Though, there are specific steps the shareholder must take before converting this type of preferred share to a common one. The similarity between a common share and a convertible preferred share that may be converted must first be stated plainly. Some shares are transferable, which means the shareholder can give them to another person according to company rules. Non-transferable shares cannot be given away. As defined earlier, earnings per share is a firm's net profit divided by its common stock's outstanding shares. There are two main ways to calculate earnings per share: Basic Earnings per Share or Diluted Earnings per Share. The earnings per share (EPS) is a measure of the profit shown in a company's financial statements. The amount earned by each share of common stock is represented by basic earnings per share in the company's income statement. Basic earnings per share are recorded in a company's income statement and are quite important for assessing the performance of firms with just common shares. The higher the company's basic earnings per share, the greater the return on investment and profit common stockholders make. For example, if a company has 100 units of common shares and makes 1000 USD to pay shareholders, each share unit will be worth 10 USD. However, if the company instead makes 20,000 USD to pay investors, each unit of the share will then be 200 USD. The earnings per shareholder would depend on how much profit the company allots to common shareholders, ranging from 10-200USD. As demonstrated in the example, if a company's earnings per share are 200USD, then investors will be more likely to invest in that company. That is how earnings per share influence investments in a company. Basic earnings per share are most accurate when calculating for companies with uncomplicated financial structures or that only have common shares. Some businesses issue a variety of shares to investors. For such organizations, simply calculating earnings per share based on common shares alone may not be sufficient, as there are various sorts of shares, including convertible preferred stocks. To calculate basic earnings per share, diluted earnings per share is used in firms with a complicated financial structure. Such companies generally compute both basic and diluted earnings per share to ensure that investors have all the information they need about the company's profits. The following are the many sorts of earnings per share that differ from the calculation described above. There are five types of earnings per share, which are discussed further down. The reported earnings per share are calculated using generally accepted accounting principles. The company declares this during its filing with the Stock Exchange Commission. A pro forma or continuing earnings per share is a variant of earnings per share that excludes one-time events and extraordinary occurrences. It is calculated using the regular net profit of a corporation. This sort of earnings per share allows for consistent comparisons by excluding unusual occurrences like the sale of a major division, which would distort comparative figures. The carrying value earnings per share, also known as book value earnings per share, reveals the company's worth or equity in each share. If a firm is liquidated, the book value earnings per share are enough to calculate the worth of each share. When a company has enough profit to pay shareholders but chooses not to, Retained earnings per share is the amount of money that would have gone to shareholders. For example, if a company makes 8 dollars per share instead of 10 USD, which it could have quickly paid out, then the $2 withheld from each shareholder is considered retained earnings per share. Stock price movement is the most significant indicator of future performance. Cash earnings per share are calculated by dividing a firm's operating cash flow by diluted shares outstanding. Because it represents the actual cash paid to shareholders, potential investors pay close attention to cash earnings per share. An investor is more likely to invest in a firm that reports earnings per share of 50 USD and cash earnings per share of 30 USD than one that reports earnings per share of 50 USD but no cash earnings per share. The most crucial aspect of earnings per share comprehension is knowing how to do the calculation. In this chapter, we will look at how to calculate a company's various earnings per share. As mentioned earlier in this book, basic earnings per share show how much was earned by each common stock and is useful for calculating earnings per share for companies with a straightforward financial structure or who only have common shares. Earnings per share is an important metric used by investors and analysts to evaluate a company's financial performance. It can be calculated using different methodologies, which is important to keep in mind when comparing companies across industries. When analysts or investors use earnings per share to make decisions, they are usually looking at either basic or diluted earnings per share. Basic EPS is calculated by dividing a company's net income by the number of its outstanding shares. Diluted EPS, on the other hand, reflects the potential dilution that could occur if convertible securities or options were exercised. This is commonly used by investors because it gives a more accurate picture of a company's true profitability. However, it is also important to look at other types of earnings per share, such as cash, reported, continuous/pro forma, carrying value, and retained EPS, to get a fuller picture of a company's financial performance. Investors should also be aware that companies can sometimes manipulate their reported earnings per share by using accounting techniques such as aggressive revenue recognition or creative expense management. As an investor, it is important to be aware of these practices and to understand a company's financial statements in order to get an accurate picture of its profitability.Earnings per Share

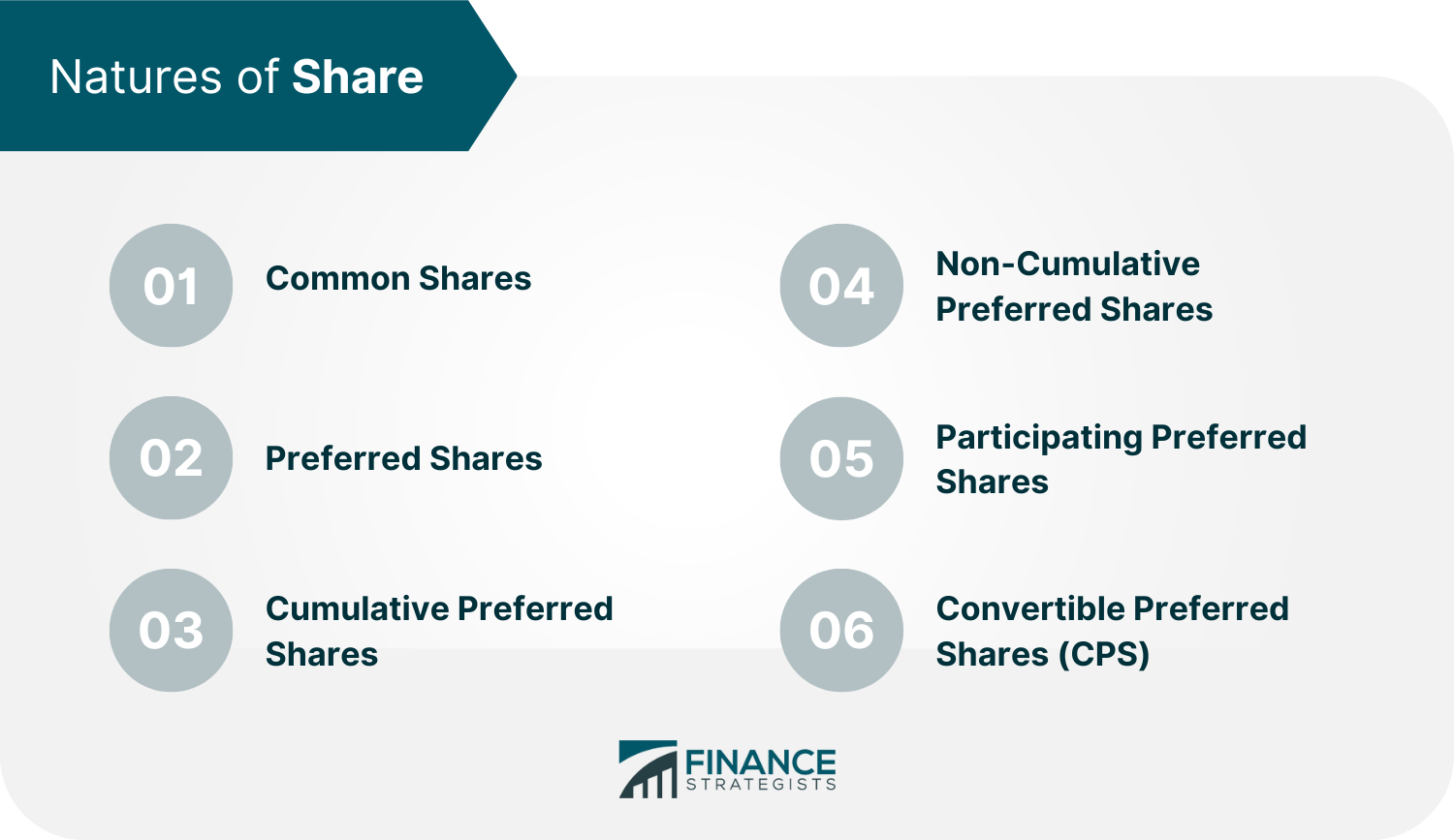

The Nature of Shares

Preferred Shares

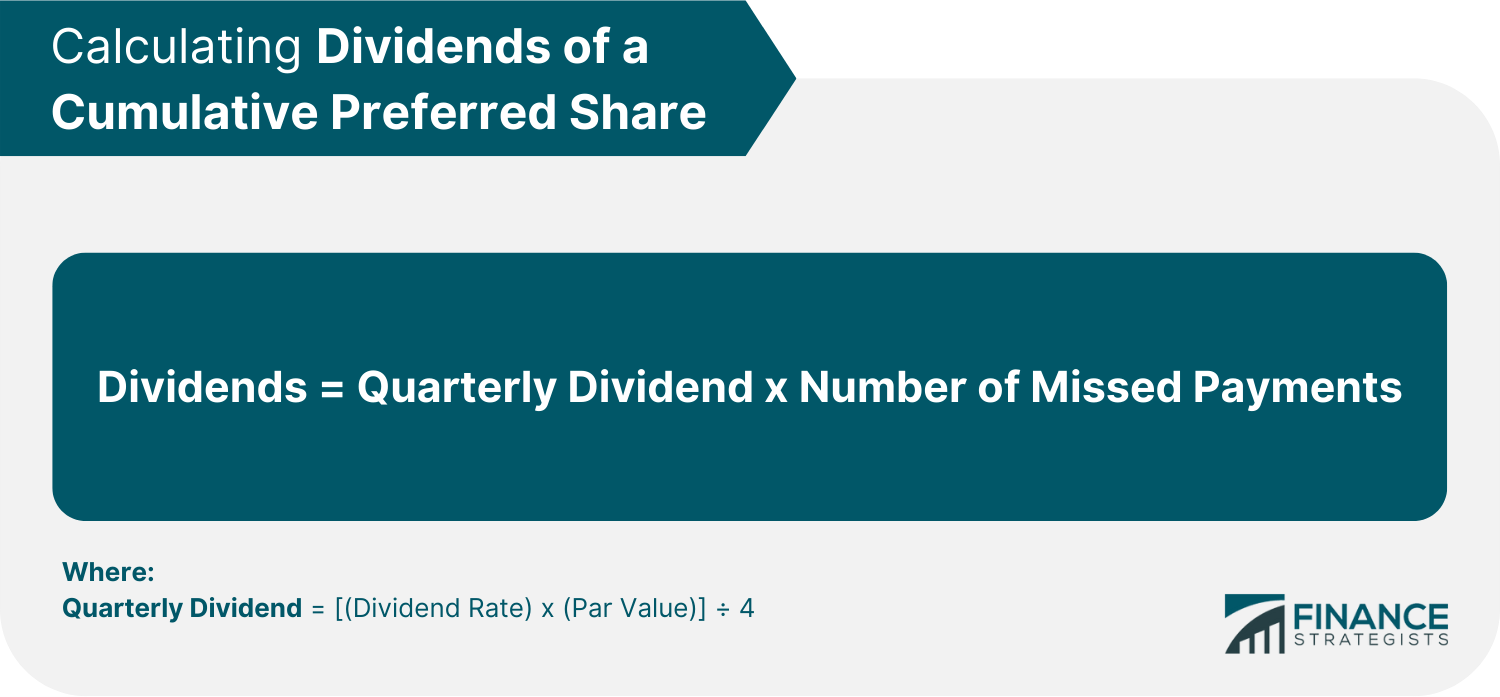

Cumulative Preferred Shares

Non-Cumulative Preferred Shares

Participating Preferred Shares

Convertible Preferred Shares (CPS)

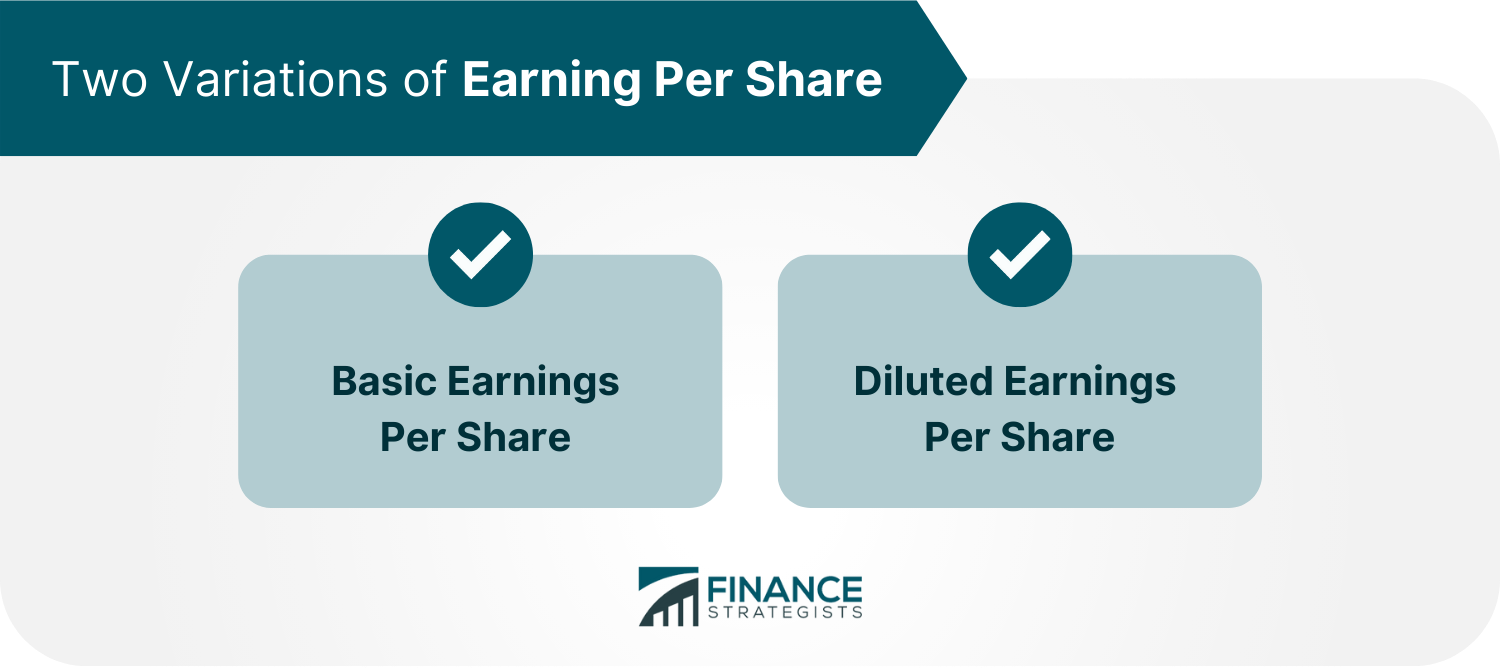

The Variations of Earnings Per Share

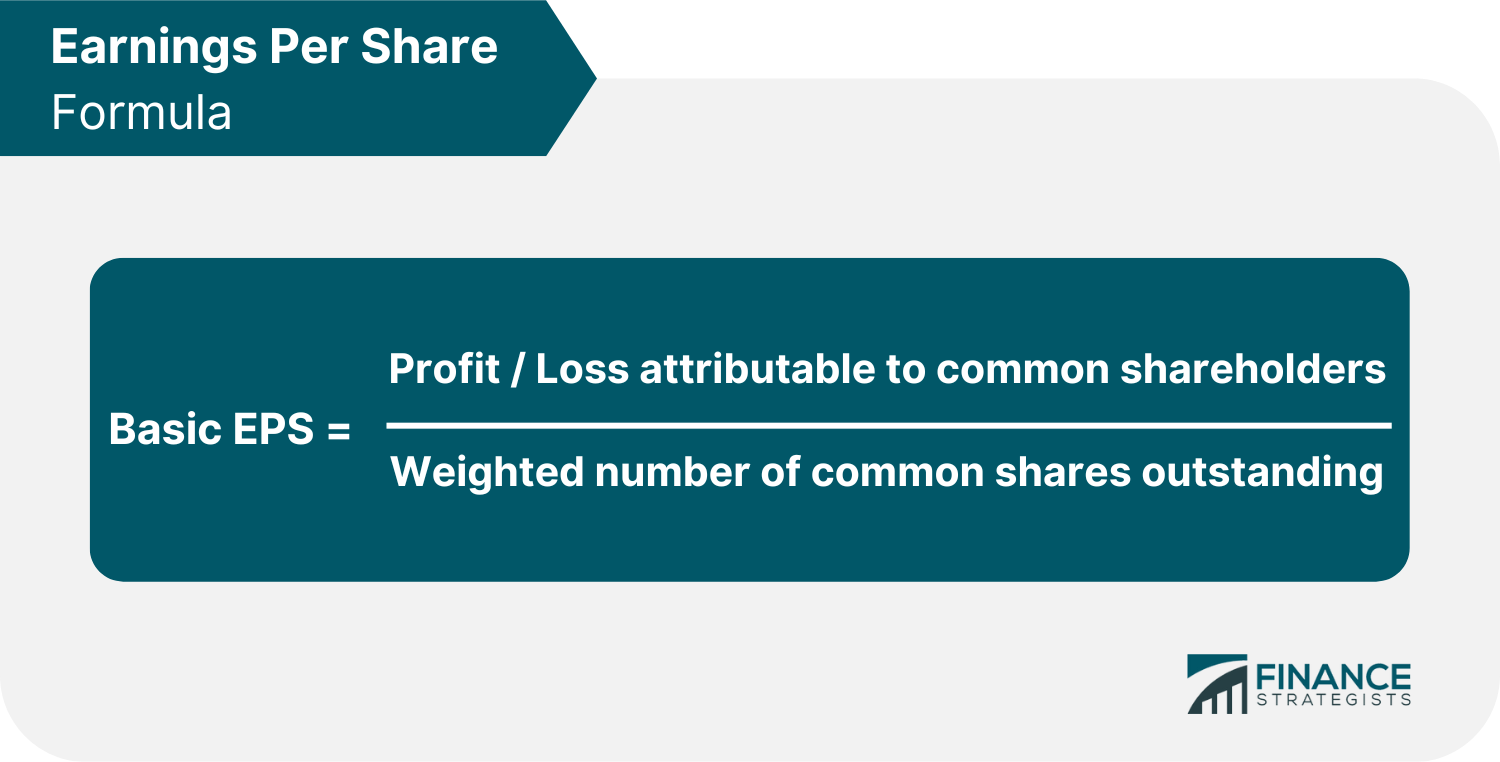

Basic Earnings Per Share

Diluted Earnings Per Share

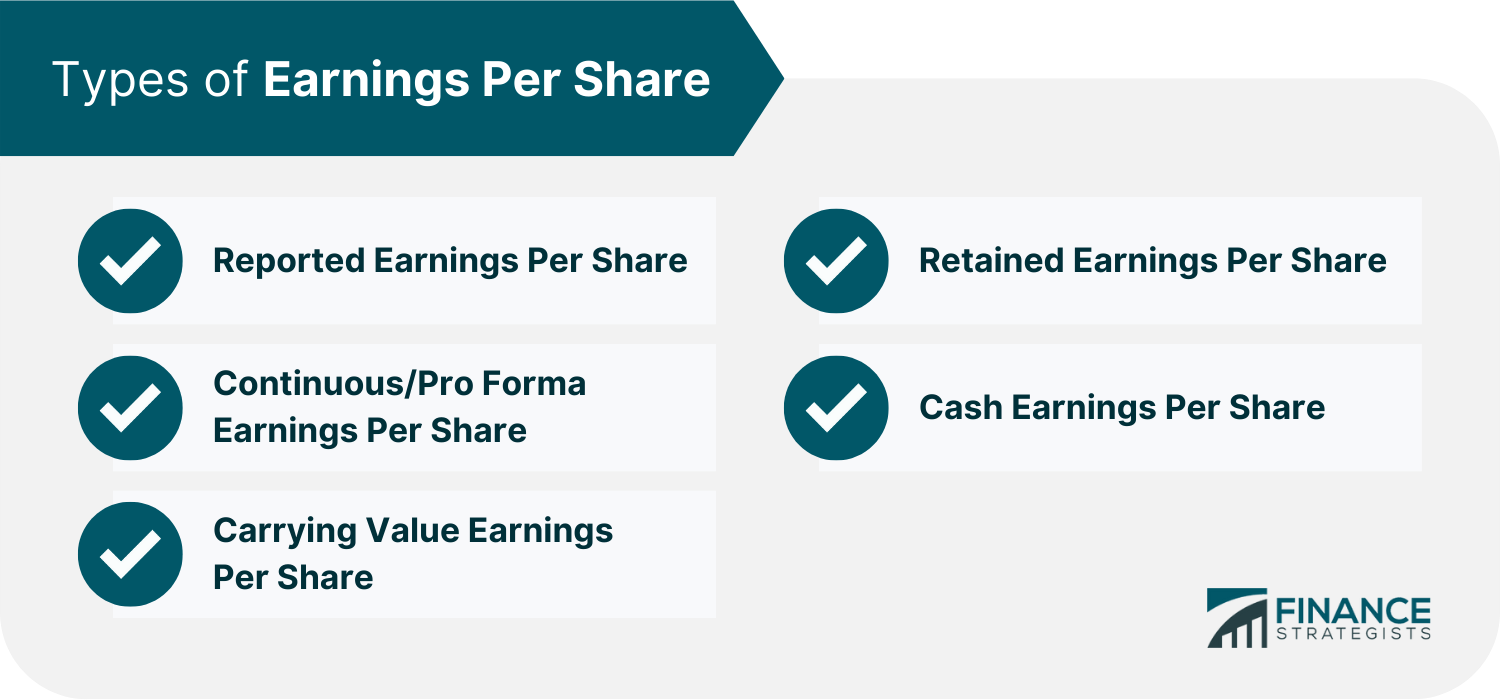

Types of Earnings Per Share

1.) Reported Earnings Per Share

2.) Continuous/Pro Forma Earnings Per Share

3.) Carrying Value Earnings Per Share

4.) Retained Earnings Per Share

5.) Cash Earnings Per Share

Calculating Earnings Per Share

Final Thoughts

Earnings per share (EPS) FAQs

Basic EPS and diluted EPS are used to measure the profitability of a company. The amount earned by each share of common stock is represented as basic earnings per share in the company income statement. The higher the company's basic earnings per share, the greater the return on investment and profit common stockholders make. On the other hand, diluted earnings per share represent the profit that would be earned by each share of common stock if all dilutive securities were converted into common stock. This includes options, warrants, and convertible debentures. Diluted EPS is usually lower than basic EPS because it takes into account the potential dilution of earnings that could occur if all dilutive securities were exercised.

To calculate a company's earnings per share, take a company's net income and subtract from that preferred dividend. Then divide that amount by the average number of outstanding common shares.

There are several types of earnings per share, including cash, reported, continuous/pro forma, carrying value, and retained EPS.

Pro forma earnings per share is a measure of a company's profitability that excludes one-time or non-recurring items. This allows investors to get a more accurate picture of the company's true profitability. Reported earnings per share, on the other hand, includes all items that are reported on the income statement.

Earnings per share is an important metric used by investors and analysts to evaluate a company's financial performance. It can be calculated using different methodologies, which is important to keep in mind when comparing companies across industries.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.