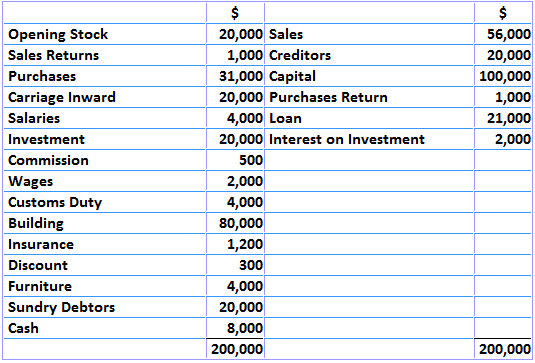

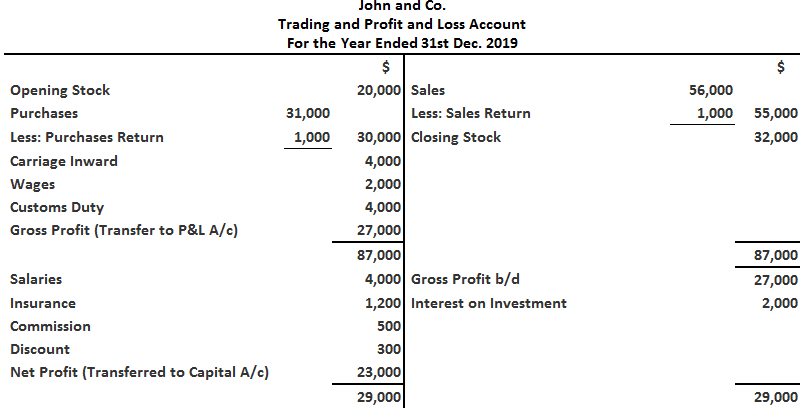

A profit and loss (P&L) account shows the annual net profit or net loss of a business. It is prepared to determine the net profit or net loss of a trader. The P&L account is a component of final accounts. A profit and loss account is prepared to determine the net income (performance result) of an enterprise for the year/period. This is the most significant information to be reported for decision making. Net income or net profit is calculated by charging all operating expenses and by considering other incomes earned in the form of commission, interest, rent, discounts, and fees. In fact, the profit and loss account is prepared by following the accrual system of accounting, in which gross profit and other operating incomes are credited and all operating expenses are debited. The resulting effect is either net profit or net loss. If the total amount of gross profit and other operating incomes exceeds the operating expenses, the difference is treated as net income or net profit. By contrast, if the total amount of gross profit and other operating incomes is less than the operating expenses, then the difference is treated as a net loss. The following items usually appear on the debit and credit side of a profit and loss account. On the debit side: On the credit side: Net profit or net loss is the difference between the total revenue for a certain period and the total expenses for the same period. A company reports net profits when its total revenues exceed its total expenses. If the value for total revenues is less than the total expenses, a net loss is incurred. The resulting balance at the bottom of a profit and loss account (see below) represents either a net profit or net loss that will be transferred to the capital account. If it is prepared in the form of a statement, it appears as shown below. Notes: When preparing a profit and loss account, it is important to remember that closing entries are made at the end of each accounting period. The aim is to transfer the indirect expenses and indirect revenue accounts to the profit and loss account. These closing entries are made in the general journal (journal proper). After making closing entries, the balances of these accounts disappear from the ledger. This is because they are closed and transferred to the profit and loss account. 1. For debit side items: 2. For credit side items: 3. For net profit: 4. For net loss: Note: In the case of a partnership enterprise, the net profit or net loss is shared according to the partner's profit-sharing ratio. Therefore, the amount of profit or loss associated with a partner will be transferred to their capital account. From the following trial balance of John and Co., prepare the trading and profit and loss accounts for the year ended 31st December 2024. The closing stock was valued at $32,000. From the following ledger balances extracted from the books of Mr. Bharath, prepare a profit and loss account as on March 31, 2024. Profit and Loss Account for Mr. Bharath

for the Year Ended 31st March 2024 Statement of Profit and Loss Account for Mr. Bharath for the Year Ended 31st March 2024Explanation

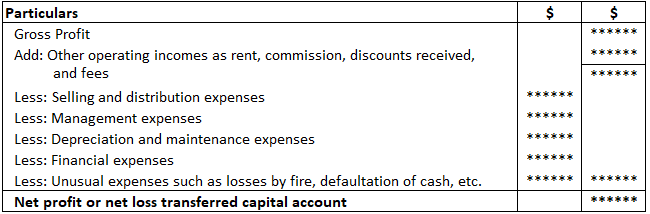

Net Profit or Net Loss

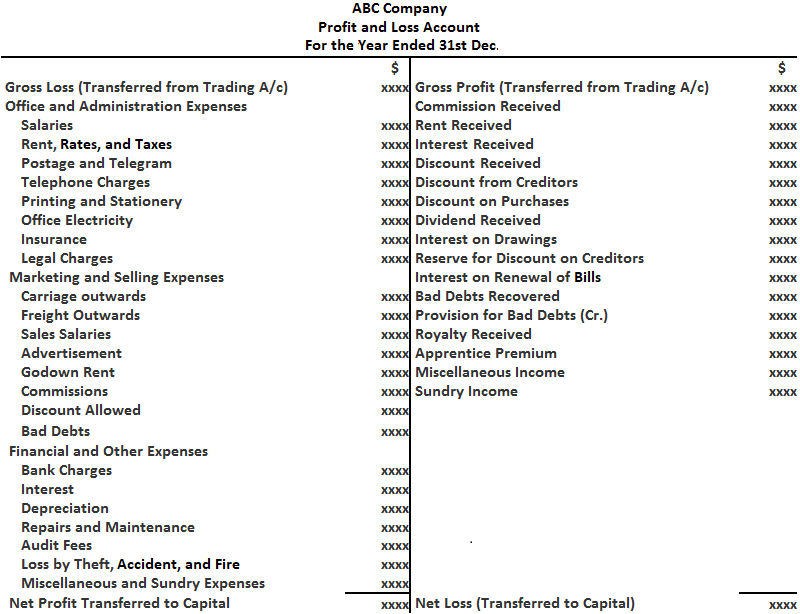

Format of Profit and Loss Account

How Are Related Items Transferred to the Profit and Loss Account?

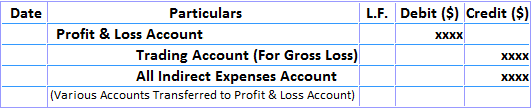

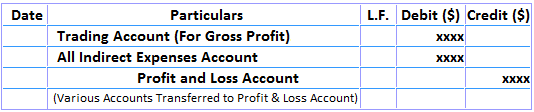

Closing Entries to Transfer Different Items in Profit and Loss Account

Example

Solution

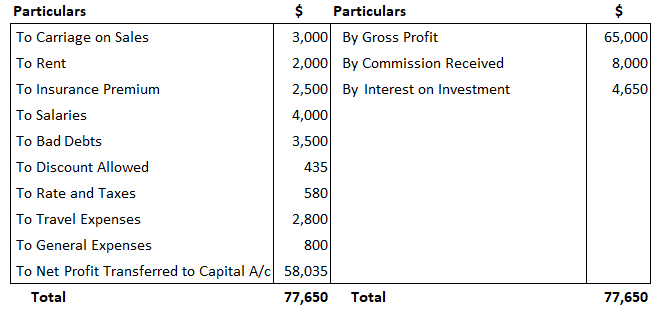

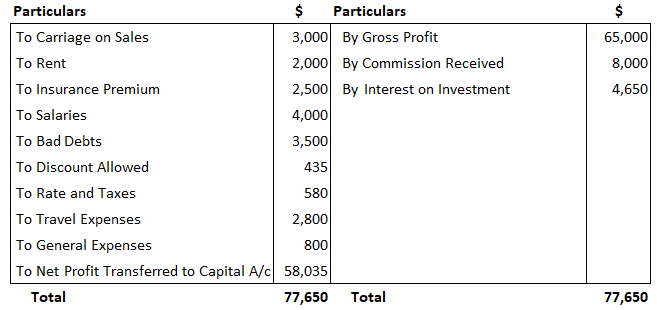

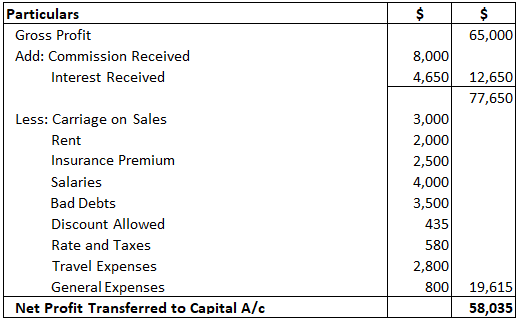

Example 2

Solution

Profit and Loss Account FAQs

A profit and loss (P&L) account shows the annual net profit or net loss of a business. It is prepared to determine the net profit or net loss of a trader. The P&L account is a component of Final Accounts.

On the debit side are the gross loss (transferred from trading account) and all indirect expenses while on the credit side are the gross profit (transferred from trading account) and all indirect revenues.

Net profit or net loss is the difference between the total revenue for a certain period and the total expenses for the same period.

When preparing a profit and loss account, it is important to remember that closing entries are made at the end of each accounting period. The aim is to transfer the indirect expenses and indirect revenue accounts to the profit and loss account.

Direct and indirect expenses are monitored by a P&L report, which provides information on indirect expenses in order to help you control these costs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.