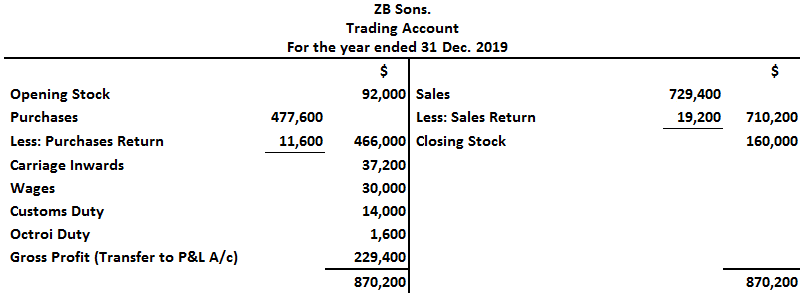

The trading account shows the result of buying and selling goods. This account determines the gross profit or the gross loss of a trader at the stage of final accounts preparation. The following items usually appear on the debit and credit sides of a trading account. This account comprises items directly related to trading, i.e., net sales + closing stock minus opening stock + net purchases + direct expenses = gross profit or gross loss. If the net sales + closing stock value is more than the opening stock, net purchases, and direct expenses, the difference is gross profit. If it is vice versa (i.e., less than), the difference is gross loss. The equation is: where, Cost of goods sold = Opening stock + Net purchases + Direct expenses - Closing stock Direct expenses include carriage inward, freight, customs duty clearing charges, import duty and dock charges, octroi, motive power, coal, gas, and fuel, and expenses with a direct bearing on the procurement of merchandise. Net purchases = purchases - purchase returns or returns outwards Net sales = sales - sales returns or returns outwards The trading account is prepared by debiting opening stock, purchases less returns, direct expenses and crediting sales less returns, and closing stock. From an accounting perspective, gross profit or gross loss is the difference between sale proceeds of a certain period and the cost of goods sold in the same period. Gross profit occurs when the sales proceeds exceed the cost of goods sold. Gross profit refers to overall profit, which means operating expenses such as administrative and selling expenses are not deducted from it. Sales proceeds less than the cost of the goods sold incur a gross loss. The balance of the trading account representing either gross profit or gross loss is transferred to the profit and loss account. A trading account has multiple features. A trading account is a nominal account. Also, it is prepared on the last day of an accounting year, and it is the first stage of the final account of a trader and the second stage of the final accounts of a manufacturer. Only revenue transactions are included in a trading account. No capital item is taken into account. A trading account has no opening balance. In the case of a manufacturing concern, it starts with the balance of the manufacturing account. A trading account is debited with the cost of goods sold and all the expenses connected with the purchase of goods and credited with sale proceeds of goods. Expenses concerning the sale of goods are not recorded here (they are included in the profit or loss account). All expenses relating to the current year — whether paid in cash or not — are taken into account. Expenses relating to the previous or next year are not included. All revenues relating to the current year — whether received in cash or not — are taken into account. Revenues relating to the previous or next year are not included. The balance of the trading account indicates the gross profit or gross loss. Credit balance represents a gross profit, while debit balance represents a gross loss. Finally, in a trading account, gross profit or gross loss is transferred to the profit or loss account. Profit or loss determined through the trading account is not the net result of the business. This means that a question naturally arises: what is the use of preparing a trading account? The answer is that a trading account is necessary since it provides several advantages. First of all, a trading account discloses gross profit from which all expenses are deducted to find out the true profit of the business (i.e., net profit). The gross profit of a business is a crucial piece of data since all business expenses are met using the gross profit. Therefore, the amount of gross profit should be adequate to meet all the expenses. Another advantage of a trading account is that net sales can be calculated at a glance. Gross sales can be ascertained from the sales account in the ledger, but net sales cannot be obtained. The true sales of a business are net sales — not gross sales. Net sales are determined by deducting the sales returns from gross sales. Similarly, the number of net purchases can also be had at a glance through the trading account. Lastly, it is possible to understand the progress or failure of a business by comparing net sales of the current year with those of the previous year. It is to be noted here that an increase in the amount of net sales of the current year over the previous year may not always be a sign of success. This is because sales may increase due to an increase in the price level. Conversely, a fall in the current year’s net sales over the previous year may decrease because of a fall in the price level. Students should note that by passing the above closing entries and following the posting procedure, these items are transferred to a trading account. While preparing a trading account, a crucial point must be kept in mind: closing entries are made at the end of each accounting period to transfer the direct expenses and direct revenues accounts to the trading account. These closing entries are made in the general journal (journal proper). After making closing entries, the balances of these accounts disappear from the ledger since they are closed and transferred to the trading account. For the items on the debit side: A sales returns account has a debit balance, and it is closed to the trading account just like other accounts following the principle of the double-entry system. However, in practice, it is not recorded on the debit side of the trading account but deducted from the sales account on the credit side of the trading account. For the items on the credit side: A purchase returns account has a credit balance, and it is closed to the trading account just like other accounts following the principle of the double-entry system. However, in practice, it is not recorded on the credit side of the trading account but deducted from the purchases account on the debit side of the trading account. For gross profit: For gross loss: From the following trial balance of ZB Sons, prepare a trading account for the year ending 31 December 2024. The closing stock was valued at $160,000.What Is a Trading Account?

On the Debit Side

On the Credit Side

Explanation

Gross Profit or Gross Loss

Features

Advantages

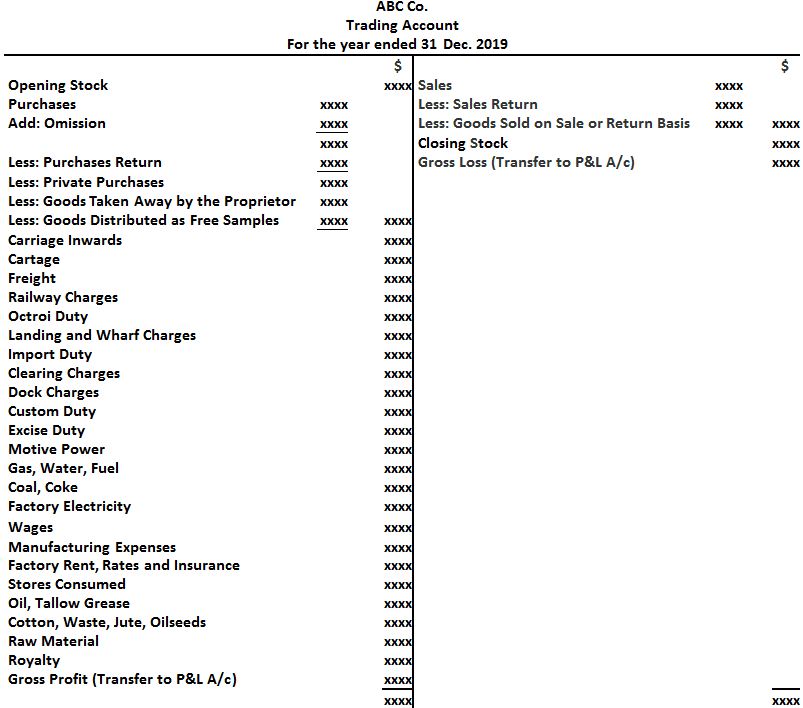

Format/Specimen of a Trading Account

How Do Related Items Travel to a Trading Account?

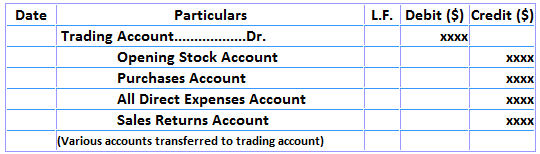

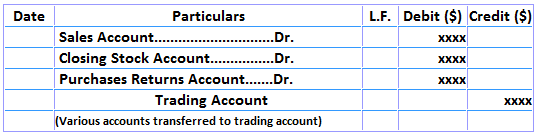

Closing Entries to Transfer Different Items in a Trading Account

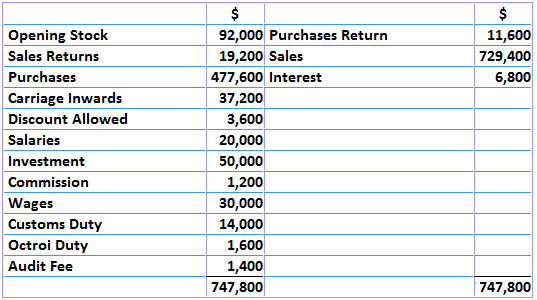

Example

Solution

Trading Account FAQs

The trading account shows the result of buying and selling goods. This account determines the gross profit or the gross loss of a trader at the stage of final accounts preparation.

The answer is that a trading account is necessary since it provides several advantages, such as:-disclosing gross profit from which all expenses are deducted to find out the true profit of the business -calculating net sales -understanding the progress or failure of a business by comparing net sales of the current year with those of the previous year

A trading account is typically prepared by the company's accountant.

The significance of a trading account is that it provides an accurate picture of a company's profits and losses from the sale of goods. This information is important for making sound business decisions.

A trading account should be prepared at the end of each accounting period.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.