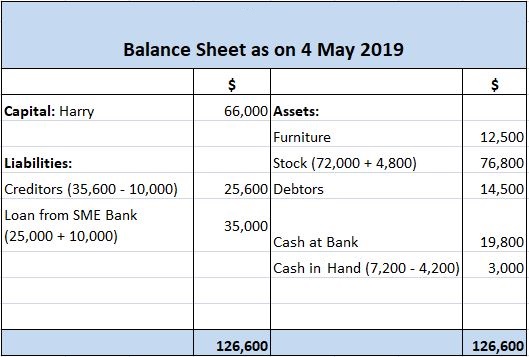

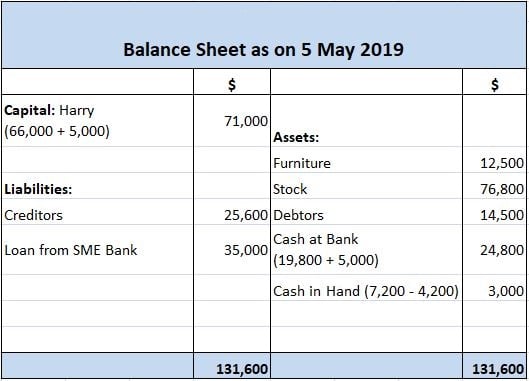

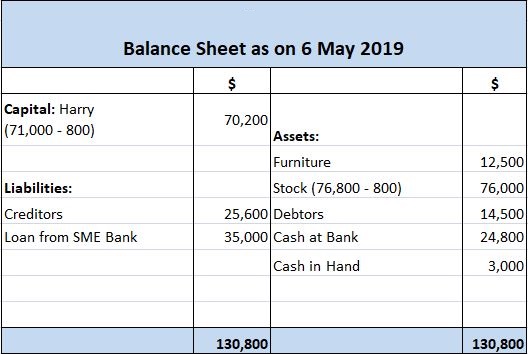

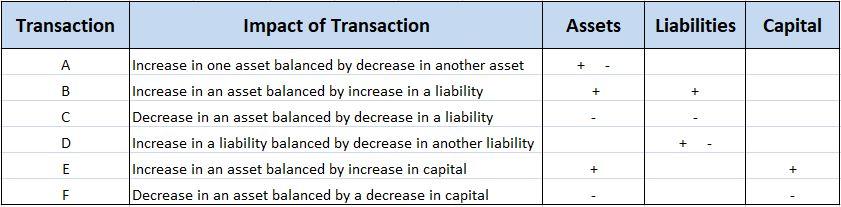

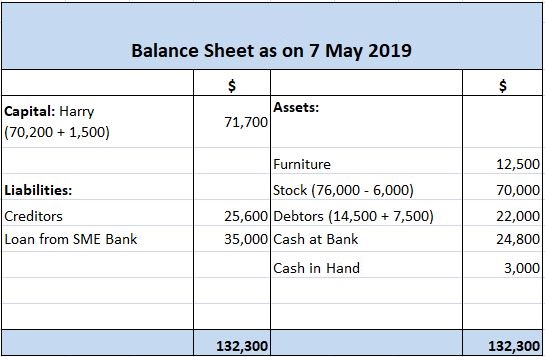

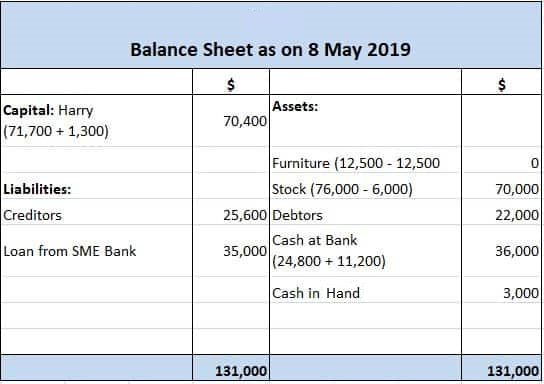

Balance sheets are only true at the time they are prepared. This is because every transaction that a business makes affects the balance sheet. Although the balance sheet equation is always true (i.e., that the two sides of the balance sheet will always have the same total), the values of individual items listed in the balance sheet change due to transactions. To clearly understand this statement and the impact that various transactions may have on a balance sheet, let's consider some examples. Suppose that Harry, a retailer, had the following assets and liabilities on 30 April 2019. On 1 May, Harry purchased a pair of chairs for $2,500, paying for them by check. The effects of this transaction were: The net impact of this transaction is that an increase in one asset (furniture) has been offset by a decrease in another asset (cash at bank). The value of total assets, therefore, remains unchanged, leaving the balance sheet in balance. The revised balance appears as follows: On 2 May, Harry bought some resale goods on credit for $4,800. The effects of this transaction are: The net impact of this transaction is that an increase in an asset (stock) is balanced by an equal increase in a liability (creditors). As the amount of capital remains unaffected, the balance sheet stays in balance. It will now appear as follows: On 3 May, Harry paid $4,200 in cash to a creditor. The effects of this transaction are: The net impact of this transaction is that a decrease in an asset (cash in hand) is balanced by an equal decrease in a liability (creditors). As the amount of capital remains unaffected, the balance sheet stays in balance. It will now appear as follows: On 4 May, Harry borrowed an additional $10,000 from SME BANK, asking SME BANK to make the payment directly to one his creditors. The effects of this transaction on the balance sheet are: The net impact of this transaction is that an increase in one liability (SME BANK) is offset by a decrease in another liability (creditors). The amount of assets and liabilities remains unaffected and, hence, the balance sheet stays in balance. After transaction D, the status of Harry's balance sheet is as follows: On 5 May, Harry introduced additional capital into his business by depositing $5,000 into the business bank account out of his personal cash held at his house. The effects of this transaction are: The net impact of this transaction is that an increase in capital is balanced by an equal increase in an asset (cash at bank). As liabilities remain unaffected, the balance sheet equation stays in balance, as shown below. On 6 May, Harry withdrew goods costing $800 from stock for personal use. The effects of this transaction are: The net impact of this transaction is that a decrease in the capital is balanced by an equal decrease in an asset (stock). As the liabilities are unaffected, the Balance Sheet stays in balance. It will now appear as follows: Did you notice how the balance sheet remained in balance after every transaction? That's to say, the total assets always stayed equal to the total of capital and liabilities. This is an essential fact to remember: Balance sheets always balance. The reason why a balance sheet always balances is easy to understand. If you check all of the above transactions, you'll notice that each one has two effects on the balance sheet. These two effects have the opposite nature and, as such, neutralize each other. The table below summarizes the impact of the various transactions seen so far. Some transactions may influence not just two but three or more items in a Balance Sheet. While the net effect of these transactions is the same as those that affect only two items, it is useful to study them a bit more carefully. On 7 May, Harry sold stock costing $6,000 (and included in his balance sheet at this value) to a credit customer for $7,500. The effects of this transaction are: The net impact of this compound transaction is that the assets side increases by a net amount of $1,500 (i.e., a $7,500 increase in debtors less a $6,000 decrease in stock). In addition, capital increases by an equal amount of $1,500. The balance sheet will, therefore, remain in balance. It will now appear as follows: On 8 May, Harry sold all of his furniture for $11,200, receiving the proceeds by check. The check was immediately deposited in Harry's business bank account. The effects of this transaction are: The net impact of this compound transaction is that the assets side decreases by a net amount of $1,300 (i.e., a $12,500 decrease in furniture less an $11,200 increase in cash at bank). Also, capital is reduced by $1,300. The balance sheet, therefore, remains in balance, as shown below.Example

1. Transaction A

2. Transaction B

3. Transaction C

4. Transaction D

5. Transaction E

6. Transaction F

Summary of Effects of Transaction on a Balance Sheet

Effect of Compound Transactions on a Balance Sheet

7. Transaction G

8. Transaction H

Effects of Transactions on a Balance Sheet FAQs

Each transaction has two effects on a balance sheet - one that increases an asset and one that decreases a liability. These two effects cancel each other out, so the balance sheet always remains in balance.

The reason why balance sheets always balance is easy to understand. If you check all of the above transactions, you'll notice each one has two effects on the balance sheet. These two effects have the opposite nature and, as such, neutralize each other.

The net impact of a compound transaction is simply calculated by subtracting its negative effect from its positive effect. In other words, the net impact is the difference between increases and decreases. The term "net" means that you have to consider whether a transaction increases or decreases both assets and liabilities.

When there's a gain, this belongs to the business unit's owner. Thus, it's added to the business's capital. In this case, assets increase by a greater amount than liabilities and equity decreases by a smaller amount.

When there's a loss, this belongs to the business unit's owner. So, it gets deducted from capital. In this case, assets decrease by a greater amount than liabilities and equity decreases by a smaller amount.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.