Just as operating leverage results from the existence of operating expenses in the enterprise's income stream, financial leverage results from the presence of fixed financial charges in the firm's income stream. In fact, financial leverage relates to financing activities (i.e., the cost of raising funds from different sources carrying fixed charges or not involving fixed charges). For example, if funds are raised through long-term debts such as bonds and debentures, these instruments carry fixed charges in the form of interest. This must be paid irrespective of the operating profits. In contrast, if funds are raised through equity shares, then the dividend to be paid is not a fixed charge. Furthermore, it is paid out of operating profits. If the funds are raised by preference shares, despite not carrying a fixed interest charge, they carry the fixed dividend rate. Therefore, the dividend payable to preference shareholders is regarded as a fixed charge when calculating financial leverage. It should be noted that equity shareholders are entitled to the remainder of the operating profits of the firm after meeting all the prior obligations. Thus, financial leverage measures the relationship between the operating profit (EBIT) and earning per share (EPS) to equity shareholders. It is calculated as the percentage change in EPS divided by a percentage change in EBIT. When calculating financial leverage, you should note that EBIT is a dependent variable that is determined by the level of EPS. To calculate both operating leverage and financial leverage, EBIT is referred to as the linking point in the study of leverage. When calculating the operating leverage, EBIT is a dependent variable that is determined by the level of sales. When calculating financial leverage, EBIT is no doubt a dependent variable, but it is determined by the level of EPS. In fact, EPS is calculated using the formula below: To calculate the degree of financial leverage, let's consider an example. XYZ Company has an EBIT of $1,000,000. The interest liability is $150,000. The company has issued 10% preference shares of $500,000 and 50,000 equity shares of $100 each. The average tax applicable to the company is 30% and corporate dividend tax is 20%. Required: Calculate the degree of financial leverage. Number of equity shares = 50,000 EPS = Earnings available to equity holders / Number of shares = 535,000 / 50,000 EPS = 10.7 Financial leverage = EBIT / EBT -D ÷ (1 - t) = 1,000,000 / 850,000 - 60,000 ÷ (1 - 0.30) = 1,000,000 / 850,000 - (60,000 ÷ 0.7) = 1.000.000 / 850,000 - 85,714 Therefore, the degree of financial leverage = 1,000,000 / 764,286 = 1.308 Let's examine how EPS varies at different levels of EBIT, taking into account the following: In this example, suppose that HT Limited's EBIT for the current year is $1,000,000. The company has 5% bonds amounting to $400,000. What is the EPS? Suppose the EBIT is: How would this affect EPS? You can assume that the company falls under the tax bracket of 40%. The number of outstanding equity shares is 100,000. Required: Calculate the financial leverage and interpret the results. EPS = Earnings available to equity holders / Number of shares = 548,000 / 100,000 = 5.48 = 668,000 / 100,000 = 6.68 = 428,000 / 100,000 = 4.28 Based on calculations like those shown above, the finance manager can make appropriate decisions by comparing the cost of debt financing to the average return on investment. To conclude, financial leverage emerges as a result of fixed financial cost (interest on debentures and bonds + preference dividend). If the financial leverage is positive, the finance manager can try to increase the debt to enhance benefits to shareholders. Where earnings are either equal to fixed financial charge or unfavorable, debt financing should not be encouraged. Operating leverage helps to determine the reasonable level of fixed costs, whereas financial leverage helps to ascertain the extent of debt financing. Both financial and operating leverage emerge from the base of fixed costs. That's to say, operating leverage appears where there is a fixed financial charge (interest on debt and preference dividend). The variability of sales level (operating leverage) or due to fixed financing cost affects the level of EPS (financial leverage). It is observed that debt financing is cheaper compared to equity financing. This encourages finance managers to opt for more debt financing. Simultaneously, one should be conscious of the risks involved in increasing debt financing, including the risk of bankruptcy. Therefore, it is suggested to have a trade-off between debt and equity so that the shareholders' interest is not affected adversely. As this discussion indicates, both operating and financial leverage (FL) are related to each other. Both of them, when taken together, multiply and magnify the effect of change in sales level on the EPS. However, operating leverage directly influences the sales level and is called first-order leverage, whereas FL indirectly influences sales and is called second-order leverage. If the operating leverage explains business risk, then FL explains financial risk. In conclusion, the higher the operating leverage, the more the company's income is influenced by fluctuations in sales volume. If the sales volume is significant, it is beneficial to invest in securities bearing the fixed cost. In the case of FL, the higher the amount of debt, the higher the FL. High leverage may be beneficial in boom periods because cash flow might be sufficient. During times of recession, however, it may cause serious cash flow problems. This is because there may not be enough sales revenue to cover the interest payments. However, the finance manager should carefully consider the situation and make a decision that enhances the benefits to shareholders. To cover the total risk and to be precise in their decision, the financial manager may rely on combined leverage.What Is Financial Leverage?

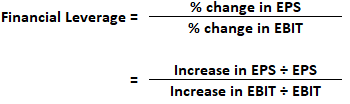

Formula For Financial Leverage

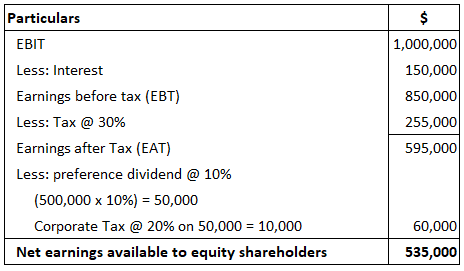

How to Calculate Degree of Financial Leverage

Solution

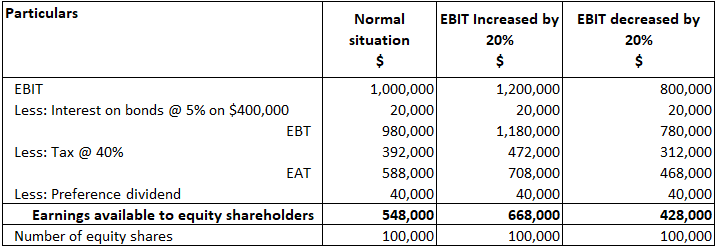

Example

Solution

Interpretation

This situation encourages the finance manager to go in for more and more debt financing to enhance the benefits to shareholders.

This situation is called unfavorable financial leverage or negative financial leverage.

Operating and Financial Leverage Viewed Together

Financial Leverage FAQs

Financial leverage is the use of debt to increase investment returns.

Benefits of financial leverage include that it increases profits without increasing sales, it reduces risk on investments, and decisions can be made rapidly with less time required for planning and implementation than other methods.Some risk factors of financial leverage include interest expenses, potential bankruptcy if interests can not be paid, and loss in market value for publicly traded stock.

Examples of financial leverage usage include using debt to buy a house, borrowing money from the bank to start a store and bonds issued by companies.

Financial leverage is calculated using the following formula: assets ÷ shareholders' equity = debt ratio.

Financial leverage relates to Operating Leverage, which uses fixed costs to measure risk, by adding market volatility into the equation. First-order operational leverage affects income directly, whereas second-order or combined leverage affects income indirectly through fluctuations in asset values.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.