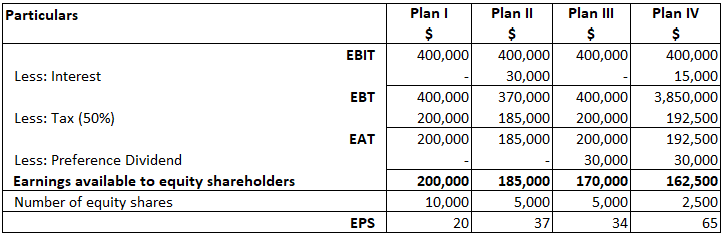

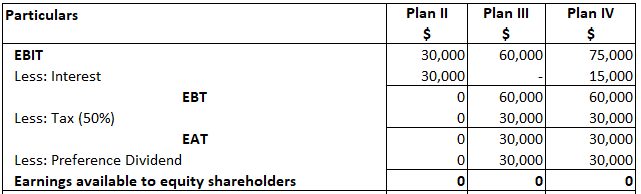

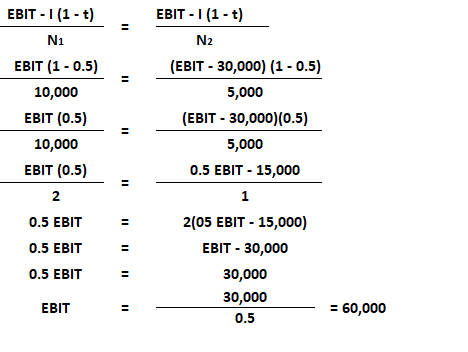

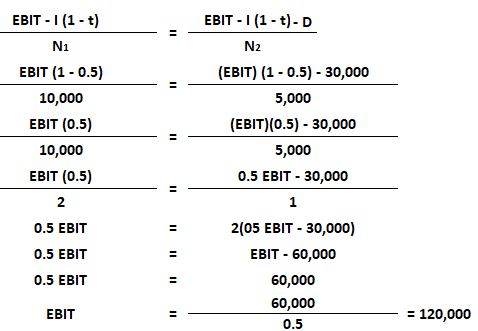

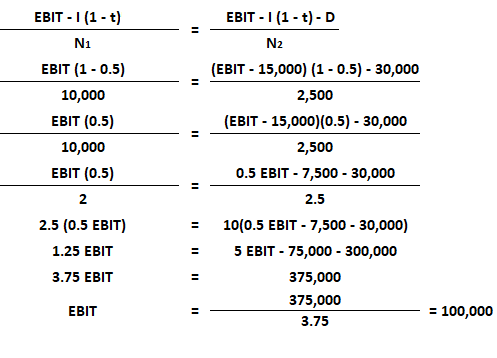

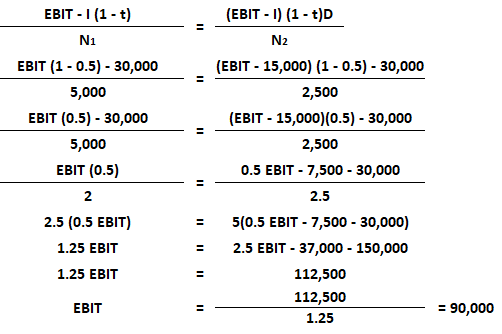

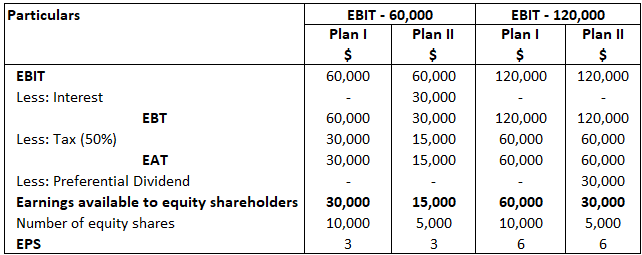

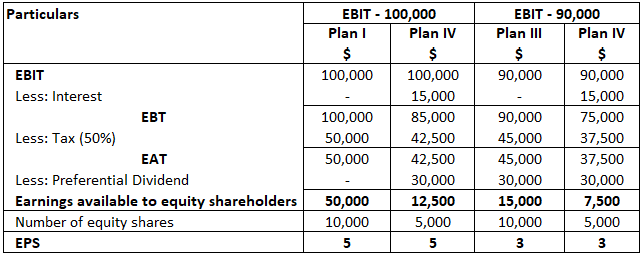

The so-called debt-equity mix is used to make financing decisions that increase the earnings per share (EPS) of a company. EBIT-EPS analysis involves determining the crossover or indifference EBIT at which the EPS is the same between two financing alternatives. In other words, the use of a financial break-even point (BEP), and the return from alternative financial plans, is called indifference analysis. EBIT-EPS analysis involves comparing alternative methods of financing and their impact on earnings. When making financial decisions, companies have many options. For example, if a company has to raise funds to finance its investment proposals, it has options such as: The choice of proportions from the above funding options is made to ensure the highest EPS at the given level of earnings before interest and taxes (EBIT). Thus, EBIT-EPS analysis helps to determine EPS under various financial plans. Indifference analysis is generally undertaken using the formula stated below. Suppose that a company is comparing two possible financing alternatives, 1 and 2. Then the indifference EBIT is calculated as follows: where: If the capital structure of the company does not contain preference shares and the earnings of the company do not come under the tax bracket, then the following formula can be applied: The necessary conditions for calculating the indifference point are: XYZ Company requires $1,000,000 for its proposed plan. The following financial alternatives are available: The rate of tax applicable to the company is 50%. The company expects an EBIT of $4,000,000. Required: Calculate the following: 1. EPS under different plans 2. Determination of financial break-even point Plan I: There is no fixed financial charge (debenture interest or preference dividend). Therefore, there is no financial break-even. Plan II: Fixed financial charges amount to $30,000 (interest on debentures). Therefore, the financial break-even is $30,000. Plan III: In the case of Plan III, the fixed financial charge is $30,000 (preference dividend). Preference dividend is payable out of profit after tax. The tax rate applicable is 50%. Therefore, the financial break-even is $60,000 (Dividend 30,000 + Tax 30,000). Plan IV: In the case of Plan IV, the fixed financial charges are $75,000, i.e., interest on debentures $15,000 + preference dividend ($30,000 + Tax on profit $30,000) $60,000. Verification 3. Indifference point of EBIT between different plans Plan I and Plan II Plan I and Plan III Plan I and Plan IV Plan II and Plan III Plan II and Plan III are not comparable because they have the same equity capital base. Plan III and Plan IV Calculations for EPS at various levels are shown below. Note: Plan I and III with EBIT $120,000 are considered to be beneficial as they have the highest EPS of $5.Indifference Analysis: Definition

Indifference Analysis: Explanation

Formula for Indifference Analysis

Calculating the Indifference Point

Example

Solution

Indifference Analysis FAQs

The use of a financial break-even point (bep), and the return from alternative financial plans

The firm’s capital structure should have equity capital as a component and financial plans should have differing equity capital bases

The main use of indifference analysis is to find the financial break-even point at which the EPS is same for two financing alternatives.

A company can use indifference analysis to find its optimal capital structure by calculating the financial break-even point for each financing alternative and then selecting the alternative that results in the highest EPS.

Some of the limitations of indifference analysis are: It does not take into account the costs of different financial plans It does not take into account the tax benefits associated with different financial plans

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.