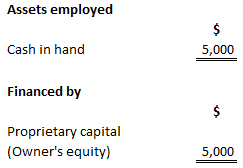

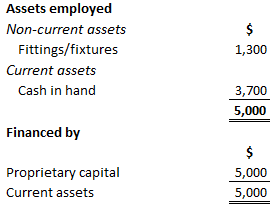

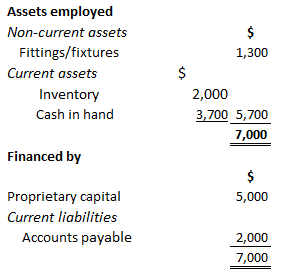

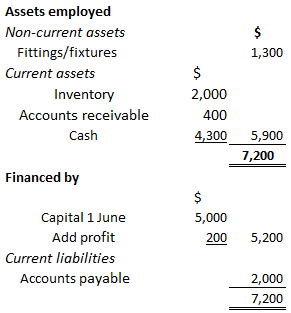

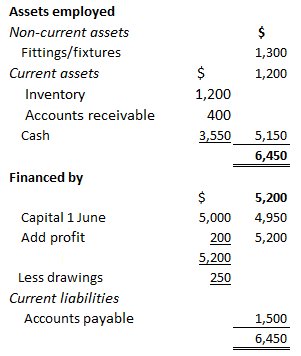

The first consideration to be given to any new business venture is that of finance. A trading business needs substantial funds or extended credit facilities from the outset. A place must be found to store and check the safety of the merchandise. Also, thought needs to be given to deliveries (involving transport), communications (e.g., telephone and email), and recording cash and credit dealings (the bookwork and accounts). In addition, at least some small reserve of finance is required to maintain the business owners during the initial period of creating or developing the business. In this article, one of the key documents in elementary accounting is explained: namely, a financial statement called the statement of financial position (sometimes called the balance sheet). A statement of financial position is a snapshot in time that always considers past events (i.e., transactions that have already taken place). An accounting period of 12 months is generally used for this type of financial reporting. Users of statements of financial position include management personnel, business owners, employees, lenders, and other stakeholders. Suppose you've inherited $5,000. You decide to use the funds to start a business from your home address. With effect from 1 June, this $5,000 is allocated to your new business venture to become the sole asset and property of the business in your name. The business, which is regarded as separate from you personally, acknowledges its debt to you as owner and proprietor in this opening balance sheet, thus: Statement of Financial Position as of 1 June The routine business dealings of a small retail trader are called transactions. Generally, these transactions involve the following: During the first week of June, a number of transactions take place, and in this particular instance, a separate balance sheet has been drawn up simply to illustrate how this financial statement is affected in two ways by each transaction. Normally, though, the listing and grouping of assets and liabilities on a balance sheet would be made in greater detail at the end of the trading period, perhaps every six months or only once a year. 2 June: You pay $1,300 for storage cupboards and some strong shelving. NB: The four stages of these elementary balance sheets are explained by simple arithmetic. Statement of Financial Position as of 2 June The payment for the non-current asset does not affect the holding of the proprietor (their capital) or current liabilities, which is because the business has no outside debts at this stage. 3 June: You purchase goods on credit priced at $2,000 from Wholesalers Ltd, arranging to pay for the goods bought later in the month. Statement of Financial Position as of 3 June Supposing you make a profit of 20% on the selling price, the cost of the goods sold is thus $800. Statement of Financial Position as of 4 June Amount due from credit customer ($400) is shown under accounts receivable. The difference between the cost price of $800 and the selling price of $1,000 is the trading profit. Statement of Financial Position as of 5 June Note how the proprietor's capital account of this small business remains constant until it is affected by: Of course, the proprietor's capital account would increase if additional private capital is paid into the business. Some elementary accounting concepts have been touched upon in this short balance sheet discussion. At each stage, there is an emphasis on total assets equaling total liabilities (including the capital). In other words, the accounting equation—namely, A = C + L—applies all the way through, where:Statement of Financial Position: Definition

Example

You may have other sources of income and property of your own, but that is your private affair, quite distinct from this new trading venture now being financed by your investment of $5000.

Property has been acquired for permanent use by the business. This purchase is shown as a non-current asset. Cash is decreased by the sum paid out.

Goods to the value of $2,000 have been taken into the inventory at cost price, increasing current assets to $5,700.

These goods have been bought on credit (no money has been paid). So cash remains at $3,700.

There is still no change in the owner's capital account. However, an outside liability has been incurred by $2,000.

The individual names of accounts payable do not appear on the statement of financial position.

4 June: You sell goods priced at $600 to a cash customer, and further goods priced at $400 to a credit customer (to be paid at the end of the month).

$800 of inventory (at cost) is sold for $1,000. This leaves the inventory balance in hand at $1,200. The cash position is now $3,700 + $600 = $4,300.

5 June: You pay $500 off your supplier's account for the goods bought on 3 June and then withdraw $250 cash for your own private and personal use.

The $500 paid-off accounts payable account reduces both the business cash and the total of trade liabilities.

The inventory figure is not affected by this payment. The sum of $250 withdrawn for the proprietor's own use is called a drawing.

Business cash is reduced and also the proprietor's holding or net assets, as shown by the capital account.

Critical Point

Remember that the statement of financial position reflects the accounting equation. Therefore, since there are several ways to write the accounting equation, there are also several ways to present the balance sheet.

You must take this into account and remain flexible when you encounter different financial statements.

Statement of Financial Position FAQs

The statement of financial position, also known as the balance sheet, is a financial statement that shows a company's assets, liabilities, and equity at a specific point in time. The balance sheet can be used to give insights into a company's financial strength and health.

The statement of financial position is typically prepared quarterly or annually. However, companies may choose to prepare it more or less frequently depending on their needs.

The statement of financial position includes a company's assets, liabilities, and equity. It may also include information about a company's cash flow, earnings, and performance.

Equity is important because it represents the ownership interest of shareholders in a company. Equity can also be used to give insights into a company's financial health. For example, a high equity ratio (the ratio of equity to total assets) suggests that a company is in good financial shape.

Some common assets on the statement of financial position include cash, accounts receivable, inventory, and fixed assets.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.