Merchandise that is returned to suppliers is known as returns outward. If merchandise purchased are not received according to specifications or if they are defective, buyer can return them to the seller or ask the seller for an allowance (e.g., reduction in price). To record such returns and allowances, the purchase returns and allowances account is used in the buyer’s books. If goods are returned to a supplier, or if an invoice received from the supplier has an overcharge, a credit note would be sought to rectify the situation. All credit notes received from the supplier are entered in the returns outward book. The entries are listed in more or less the same manner as invoices received are entered in the purchases book. As the various credit notes may bear different serial numbers, these are re-numbered at the time of making entries in the returns outward book for convenience in filing and reference. This example shows how to record the following transactions in John’s returns outward book. The returns outward book will appear as follows: The journal entries for the return of merchandise purchased for cash and merchandise purchased on account are different. When merchandise purchased for cash are returned to the supplier, it is necessary to make two journal entries. In the first entry, we debit the accounts receivable account and credit the purchase returns and allowances account. This entry is made to recognize the return of merchandise. In the second entry, we debit the cash account and the credit accounts receivable account. This entry is made when a refund is received from the supplier for the returned merchandise. On 1 April 2016, Y Merchants purchased merchandise for $2,500 in cash from Z Traders. Upon delivery, Y Merchants found serious defects in the items, meaning that they could not be sold to customers. Y Merchants returned the merchandise to Z Traders on the same day. On 2 April 2016, Z Traders returned the full amount in cash to Y Merchants. Required: Make a journal entry in the books of Y Merchants that records: When merchandise purchased using an account are returned to a supplier, it is necessary to debit the accounts payable account and credit the purchase returns and allowances account. On 1 April 2016, Y Merchants purchased merchandise for $2,500 on account from Z Traders. Upon delivery, Y Merchants found that the merchandise was defective and, therefore, could not sell it to customers. Y Merchants returned the merchandise to Z Traders on the same day. Required: How would you journalize the above transactions in the books of Y Merchants?Returns Outward: Definition

Returns Outward: Explanation

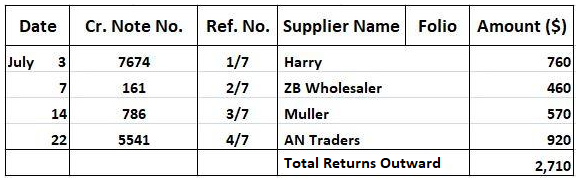

Example: Recording Transactions in the Returns Outward Book

Journal Entry

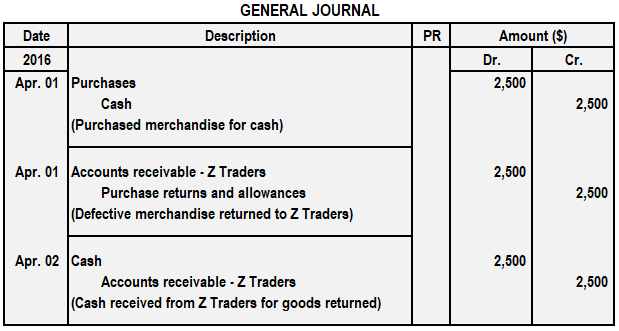

Return of Merchandise Purchased for Cash

Example

Solution

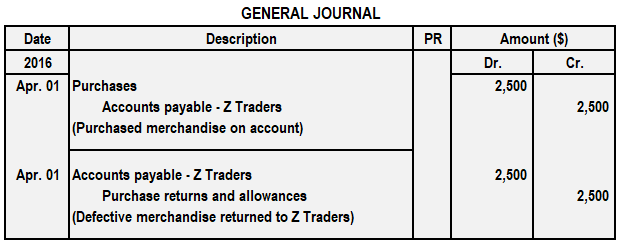

Return of Merchandise Purchased on Account

Example

Solution

Journal Entry for Purchase Returns (Returns Outward) FAQs

Merchandise that is returned to suppliers is known as returns outward. If merchandise purchased is not received according to specifications or if they are defective, the buyer can return them to the seller or ask the seller for an allowance (e.g. reduction in price).

If you need to refund a customer for a purchase they made from your business, you will need to create a purchase return journal entry. This will help you track the returned merchandise and ensure that the vendor or supplier provides you with a credit for the returned items.

To create a purchase return journal entry, you will first need to identify the merchandise that was returned. Next, you will need to record the credit that was given to you by the vendor or supplier. Finally, you will need to subtract the cost of the returned merchandise from your total sales for the period.

When merchandise purchased for cash is returned, it is necessary to make two journal entries. The first entry debits the accounts receivable account and credits the purchase returns and allowances account. The second entry debits the cash account and credits the accounts receivable account. When merchandise purchased on account is returned, only one entry is necessary, which debits the accounts payable account and credits the purchase returns and allowances account.

No, the journal entries are the same whether merchandise is returned for a credit note or for a refund of cash. In both cases, the accounts payable or accounts receivable account is debited, and the purchase returns and allowances account is credited.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.