What Is a Ledger?

Before explaining what ledger accounts, it’s worth briefly introducing the ledger.

Journals are used to record transactions chronologically, but journal entries only show the effect of individual transactions.

Business owners, however, don’t just want to know about the effects of individual transactions on financial statements. They are also interested in the accumulated effect of each account.

For example, if the business owner needs to know the total amount of purchases relating to a specific accounting period, it will be difficult to find this information in the journal.

This is because the journal contains a large number of transactions relating to purchases at different places according to their respective dates of occurrence. However, the business owner can easily find the total purchases amount from the purchases account.

Therefore, it is worthwhile for transactions of a similar nature to be sorted out and accumulated in one place. This place is known as the ledger.

Introduction to Ledger Accounts

The ledger system of double entry bookkeeping involves the use of several account-ruled books (known as a set of books) for the purpose of recording accurate information (in monetary values) of the day-to-day trading operations of a business.

From these permanent records, periodical statements are prepared to show the trading profit or loss made by the business and its assets and liabilities, at any given date.

In the past, these records would literally have been kept in bound ledger books. However, even before the widespread use of computers, mechanized systems based on mechanical accounting machines were used by many larger companies.

In smaller organizations, looseleaf systems with multipart forms and carbon paper reduced the number of times that bookkeepers had to write out the same data.

Now, any business with a full-time bookkeeper is likely to use computerized accounting. However, computerization can only speed up the arithmetical aspects of accounting; they cannot replace an understanding of the concepts.

It is notable that underlying all modern computer accounting programs is the same doubl entry system.

The Ledger: The Second Phase of Accounting

The ledger is the principal book of accounts in which transactions of a similar nature relating to a particular person or thing are recorded in classified form.

Also known as the general ledger, the ledger is a book in which all accounts relating to a business enterprise are kept. In other words, it is the collection of all accounts of a business enterprise. The accounts kept in the ledger are sometimes termed ledger accounts.

One account usually occupies one page in the ledger. However, if the account is large, it may extend to two or more pages. All entries recorded in the general journal must be transferred to ledger accounts.

The ledger may be in a bounded form or loose-leaf form. It is the master reference book of the accounting system. It provides a permanent and classified record of every element in the business operation.

Due to all of these features, the ledger is sometimes called the king of all the books of accounts.

Advantages of the Ledger

- The double entry system is successfully applied through the ledger because it records the twofold aspects of each transaction.

- Ledger information related to specific persons or things is recorded separately in the account. This enables the business to look at the accumulated figures for each account.

- Ledgers make it possible to analyze the total incomes and expenses of a business over a particular period (i.e., the trading and profit & loss account).

- By opening separate accounts for various assets and liabilities, it is also possible to learn about the financial position of a business.

- Transactions are first recorded in the journal. The ledger is the second stage where transactions are posted, thus minimizing the chance of errors and omissions.

- The ledger helps managers by providing important information needed to ensure that the business runs smoothly.

What Is Posting?

The process of transferring information from the general journal to the general ledger, for the purpose of summarizing, is known as posting. Entries relating to a particular account are all collected in that account, and so its position may be known when needed.

Ledger Accounts

The record of trading transactions is kept on the folios or pages of these account books, called ledgers. The ledger folios have special rulings to suit the needs of the business.

The bank statement style lends itself to modern accounting, but for the time being, double entry will be explained by the older traditional method.

Format of Ledger Accounts

This is the ordinary ruling for the older style of ledger account:

In practice, separate ledgers are kept for the different classes of accounts: customers, suppliers, business property, trading revenue, expenses, and so on.

Batches or groups of similar accounts are kept together, and ledgers are indexed so that information pertaining to a particular account can be obtained quickly.

A critical point to remember is the following:

It is important to check the accuracy of entries made in ledger accounts at regular intervals as failing to debit a customer’s account for goods bought on credit, for instance, may result in no payment reminder being sent.

Types of Ledger Accounts

There are two popular formats for ledger accounts:

- Standard format (or T-shaped format) of ledger account

- Self-balancing format

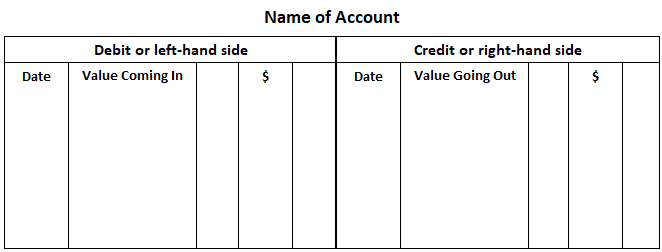

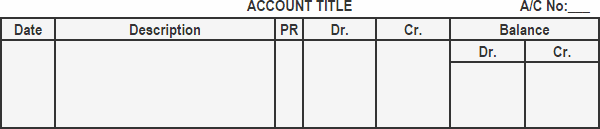

Standard Format

In the standard format of a ledger account, the page is divided into two equal halves. The left-hand side is known as the debit side and the right-hand side is the credit side. As it takes the shape of the capital letter “T”, it is also known as the T-shaped format.

The debit side is used to record debit entries and the credit side is used to record credit entries. The title of the account is written in the center at the top of the page. The account number is written in the extreme right-hand corner.

The standard form of a ledger account does not show the balance after each entry. The balance is calculated after a certain period (or when needed). This is why this type of account is also called the periodical balance format of a ledger account.

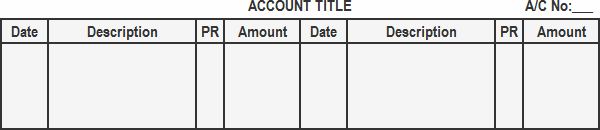

Format of a Standard Ledger Account

Notice that each side of the ledger account is divided into four columns. The purpose of these columns is briefly described below:

(1) Date: The year, month, and date of the entry are recorded in the same manner as in the general journal.

(2) Description: The title of the corresponding account is entered into this column (i.e., the other account included in the journal entry).

(3) Posting reference: In this column, the general journal page number is recorded.

(4) Amount: The amount of the account is recorded in this column.

Method of Posting

The posting process consists of the following steps:

- Trace the ledger account in which the entries are to be posted.

- If an account is debited in the general journal, it will be posted on the debit side in the ledger account, and if it is credited in the general journal, it will be posted on the credit side.

- In the description column, the title (name) of the account included in the other part of the journal entry is written. For example, when posting an account included in the journal entry’s debit part, the account(s) in the credit part will be written in the description column.

- The amount of the entry is written in the amount column of the ledger account.

Balancing the Ledger Account

Balancing means finding out the debit or credit balance of a ledger account. This process may be divided into the following steps:

- Total the debit and credit sides of the account.

- Calculate the difference between the two totals found in the previous step.

- Put the difference on the lighter side.

To elaborate on the third point above, this difference so placed is the balance of the account.

If the debit side of the account is heavier than the credit side, the account is said to have a debit balance. In case the credit side of the account is heavier than the debit side, the account is said to have a credit balance.

If the totals of the two sides of the account are equal, the balance will be zero.

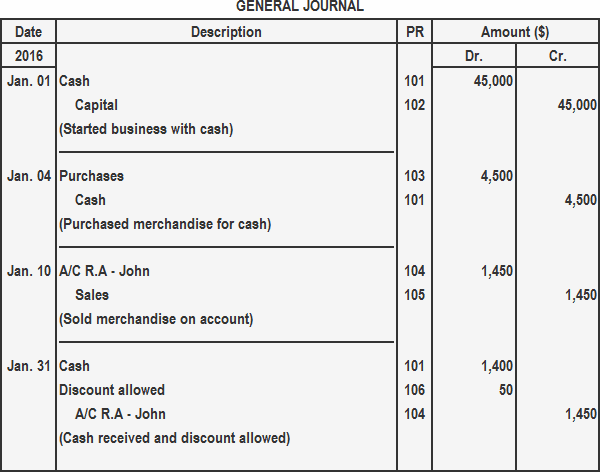

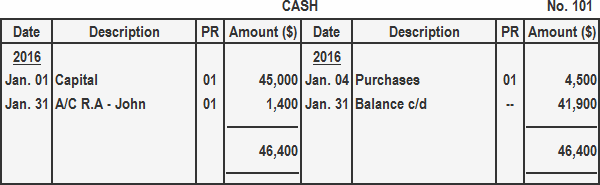

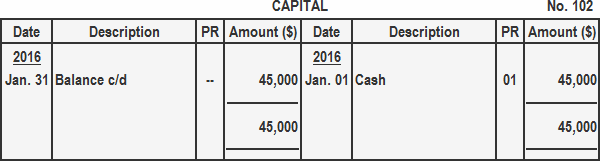

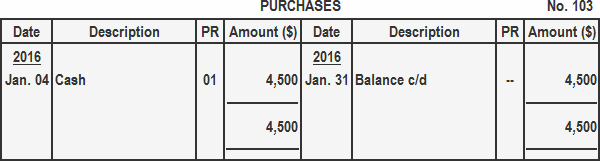

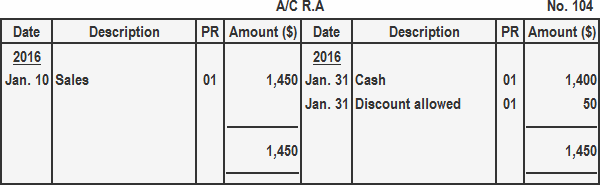

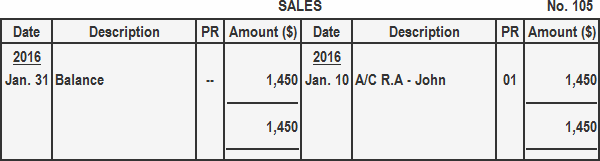

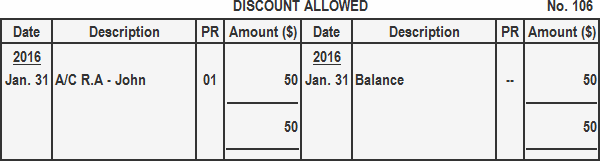

Example

Record the following transactions in the general journal and post them to the ledger accounts:

- Jan. 01: Mr. A started a business with cash of $45,000

- Jan. 04: Purchased merchandise for cash amounting to $4,500

- Jan. 10: Sold merchandise to Mr. John for $1,450

- Jan. 31: Cash received from Mr. John amounting to $1,400 with a discount of $50

Solution

Self-balancing Format

In the standard format of a ledger account, the balance is not stated after each transaction. In organizations where account balances are required after each transaction, the self-balancing or running balance format of a ledger account is used.

The main advantage of this ledger account format is that it shows the current balance at a glance. Banks and other financial institutions are examples of business organizations that use self-balancing ledger accounts.

Format of a Self-balancing Ledger Account

The standard format of a self-balancing ledger account is given below:

Posting and Balancing

The method used for posting and balancing in a self-balancing ledger account is similar to that of the standard ledger account format. The only difference is that the balance is ascertained after each entry and is written in the debit or credit column of the account.

The following example is useful to clarify the posting and balancing procedure.

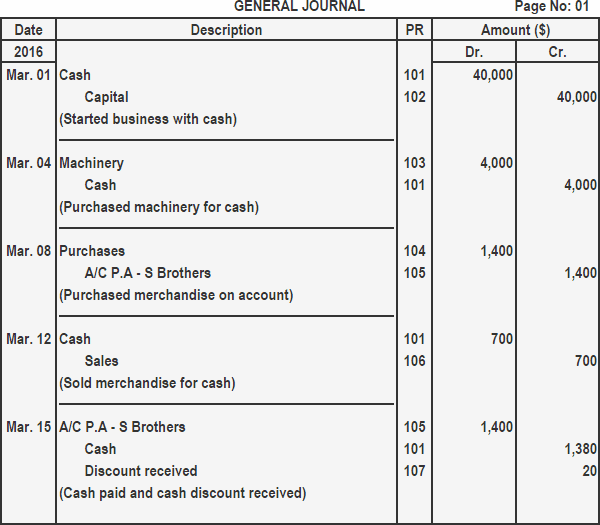

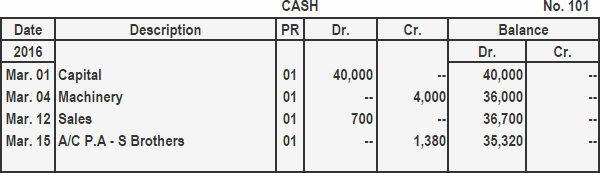

Example

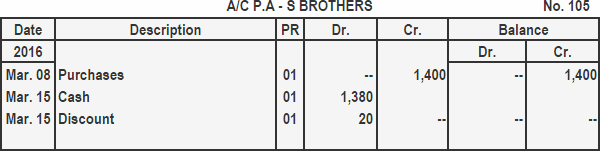

Journalize the following transactions and post them to the ledger accounts. Use the self-balancing/running balance ledger account format.

- Mar. 01: Started a business with $40,000 cash

- Mar. 04: Purchased machinery for $4,000 cash

- Mar. 08: Purchased merchandise for $1,400 on account from S Brothers

- Mar. 12: Sold merchandise to a customer for $700 cash

- Mar. 15: Paid $1,380 cash to S Brothers and received a cash discount of $20

Solution

Recording Transactions in Ledger Accounts

After recording the opening balances (i.e., the amounts at the beginning of an accounting period) in the ledger account, the next step is to record transactions as they take place.

Transactions result in an increase or decrease in the value of various individual balance sheet items. The following rules are applied to record these increases and decreases in individual ledger accounts.

1. Assets

Assets are recorded on the debit side of an account. Any increase in an asset is recorded on the debit side of the relevant account, while any decrease in an asset is recorded on the credit side.

For example, the amount of cash in hand at a particular date (e.g., the first day of the accounting period) is recorded on the debit side of the cash in hand account. Whenever an amount of cash is paid out, an entry is made on the credit side of this account.

2. Liabilities

Liabilities are recorded on the credit side of an account. Any increase in liability is recorded on the credit side of the account, while any decrease is recorded on the debit side.

For example, the amount payable to United Traders on the first day of the accounting period is recorded on the credit side of the United Traders Account.

If more goods are bought from United Traders (thereby incurring an additional liability to United Traders), an entry is made on the credit side of the United Traders Account.

Additionally, if an amount is paid to United Traders (thereby reducing the liability to United Traders), an entry is made on the debit side of the United Traders Account.

3. Capital

Capital is recorded on the credit side of a ledger account. Any increase in capital is also recorded on the credit side, and any decrease is recorded on the debit side of the respective capital account.

For example, the amount of capital that Mr. John has on the first day of the accounting period (see the previous example) will be shown on the credit side of Mr. John’s capital account.

If he introduces any additional capital, an entry will be made on the credit side of his capital account. If he draws any money or goods from the business, this will reduce his capital, meaning that an entry should be made on the debit side of his capital account.

An important point to note is that the treatment for assets is exactly the opposite of the treatment for liabilities and capital.

Another important fact to note stems from the fact that total assets are equal to total liabilities and capital at any given time.

Due to this, the amounts entered on the first day of the accounting period on the debit side of the accounts (in respect of various assets) will be equal to the total of all the amounts entered on the credit side of various accounts (in respect of various liabilities and capital).

The Double Effects of Transactions in Ledger Accounts

A balance sheet remains in balance after each transaction.

This is to ensure that each transaction affects the balance sheet in such a way that an increase on one side of the balance is offset either by a decrease on the same side or by an increase on the other side.

Therefore, various double effects of transactions in ledger accounts should be borne in mind.

1. Since increases in assets are debited and decreases in assets are credited, a transaction resulting in an increase in one asset and a decrease in another asset will in effect have equal debit and credit entries.

These entries will, of course, be made in two different asset accounts, but the amount will be equal.

For example, a receipt of $3,000 from Adam, a debtor, will be recorded on the debit side of the cash in hand account (as this asset is increasing) and on the credit side of Adam’s account (as the amount due from him is decreasing).

The entries in both of these asset accounts will amount to $3,000 each.

2. Since increases in assets are debited and increases in liabilities are credited, a transaction resulting in an increase in an asset and an equal increase in a liability (or capital) will in effect have equal debit and credit entries.

For example, when furniture is bought on credit for $4,000 from Fine Furniture Co., we will need to make an entry of $4,000 on the debit side of the furniture account (i.e., because this asset is increasing).

We will also need to make an entry of $4,000 on the credit side of the furniture account because the liability to this creditor is increasing.

3. Since decreases in liabilities are debited and decreases in assets are credited, a transaction resulting in a decrease in a liability (or capital) account and an equal decrease in an asset account, will in effect have equal debit and credit entries.

For example, when a business owner draws $500 in cash from the business cash box for his personal use, an entry will be made on the debit side of the capital account (i.e., as the owner’s capital in the business is now reduced).

An entry will also be made for an equal amount on the credit side of the cash in hand account because this asset is decreased in so far as the business is concerned.

Discussion

The above examples show that each transaction affects at least two accounts in the ledger. One of these accounts must be debited and the other credited, both with equal amounts.

Now, since opening entries have equal debits and credits, and since all the transactions also result in equal debit and credit entries, it follows that barring any errors, the total of all entries on the debit side of the ledger accounts is always equal to the total of the credit side.

This pivotally important fact is called the golden rule of bookkeeping: namely, debits must always equal credits.

Since every transaction affects at least two accounts, fully recording its impact on the ledger requires us to make two entries for each transaction. One of the entries is a debit entry and the other is a credit entry, and the amounts of both are equal.

This is what is known as the double entry system of bookkeeping. Put simply, the double entry system requires that at least two entries of equal amounts are made for each transaction: one a debit entry and another a credit entry.

Do you want to test your knowledge about ledgers? We have prepared quizzes for you.