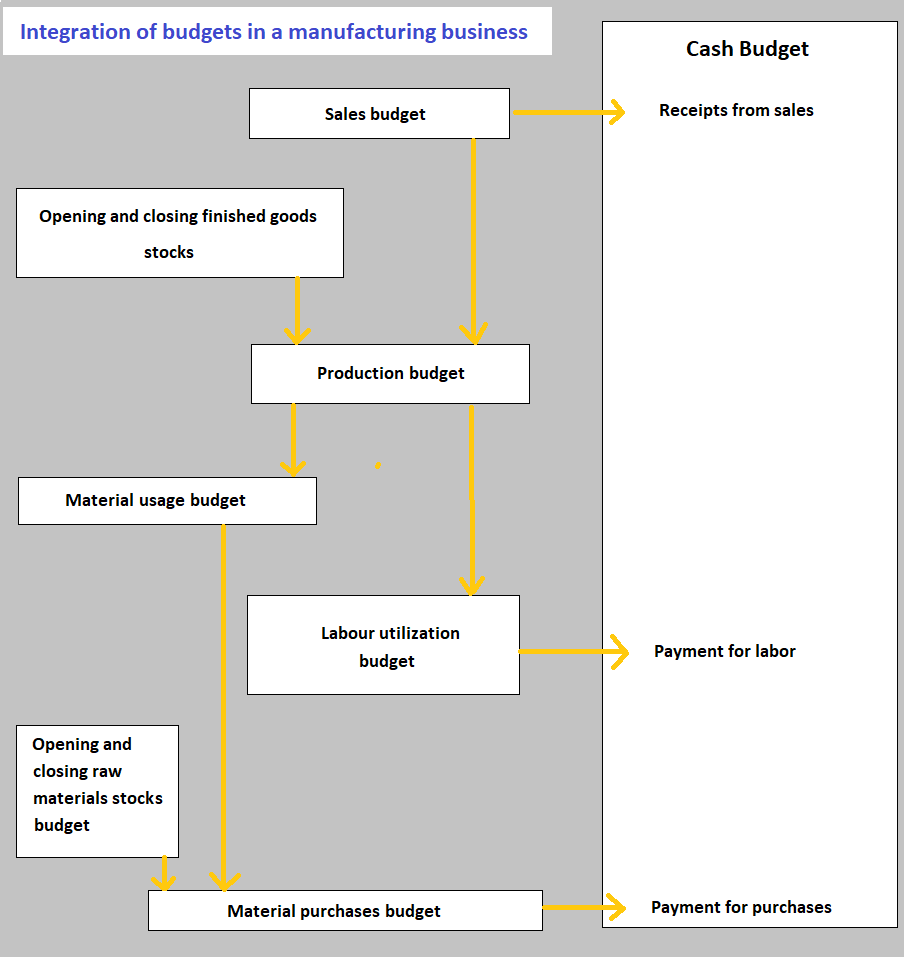

Manufacturing businesses are typically more complex than businesses that just buy and sell. In the manufacturing industry, there is a broad range of possible budgets that an organization can use to build-up the master budget and cash budget. Budgets need to be based on the same set of assumptions about the way that the organization operates. They are typically organized around estimates of the key budget factor, which is usually the sales forecast. The typical budgets are: The sales budget is usually generated directly from the key factor forecast data. The production budget is based on the sales budget together with expected stock levels of finished materials. This budget is based on the production budget. This budget is based on the materials usage budget, together with the anticipated materials stock levels. This budget is based on the production budget. These budgets are prepared to support the operations of the manufacturing business. Examples of functional budgets include the administration budget and finance budget. A capital expenditure budget must be developed in conjunction with the above revenue budgets to ensure that the agreed spending on new or replacement equipment, along with other expenditures, is in place. The cash budget takes account of the data in the above budgets. The effect of all the revenue and capital budgets is finally consolidated into the master budget. This takes the form of a budgeted profit and loss account and balance sheet for the whole manufacturing business. You will have noticed several references in the above list of budgets for a manufacturing business to stock levels. Where stock levels are to remain constant, the situation is simple. For example, the production budget will be identical to the sales budget if the finished goods stock level is to remain unchanged. However, if the stock level is to increase, then the extra units of goods that will go into stock will need to be produced in addition to the units that are to be sold immediately. This is a concept that is important throughout budgeting, including cash budget preparation. The diagram below shows how the main budgets used in a manufacturing business fit together. It also illustrates how various pieces of data are used in a cash budget. This diagram, for the sake of clarity, concentrates on issues that are specific to the creation of a cash budget for a manufacturing business. Other data (e.g., disbursements, capital items, and financing) also need to be accounted for in the cash budget.Budgets for a Manufacturing Business

Sales Budget

Production Budget

Materials Usage Budget

Materials Purchases Budget

Labour Utilization Budget

Various Functional Budgets

Capital Expenditure Budget

Cash Budget

A Note on Stock Levels

Integration of Budgets in a Manufacturing Business

Budgets for a Manufacturing Business FAQs

Although many businesses create a full 12-month budget, you can produce a budget for any period that is appropriate for your business. What length of time you use will depend on the stage in your business cycle and when you need information about future performance to help plan your work.

The length of a cash forecast will depend on the circumstances. In general, it is sensible to have forecasts that cover at least three months, and preferably six months.

Budgets can play an important role in improving your business. They can help you to identify areas where you are making losses and need to take action, as well as helping you to track your progress towards achieving your long-term goals. In addition, they can be used to measure the performance of different parts of your business.

If your budget is too restrictive, you need to take action to loosen the constraints. What you do will depend on the size of the error. If the figures are very important, you may want to discuss them with your senior managers. For example, if they have been overoptimistic about the future of the business and sales forecasts for next year show a dramatic shortfall in income, you may need to revise your plans and cut back on marketing and expansion activity.

You should review your budgets frequently to make sure they are still relevant. Your business may change very quickly, making it necessary to update or revise your plan for achieving financial success in the short and long term.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.