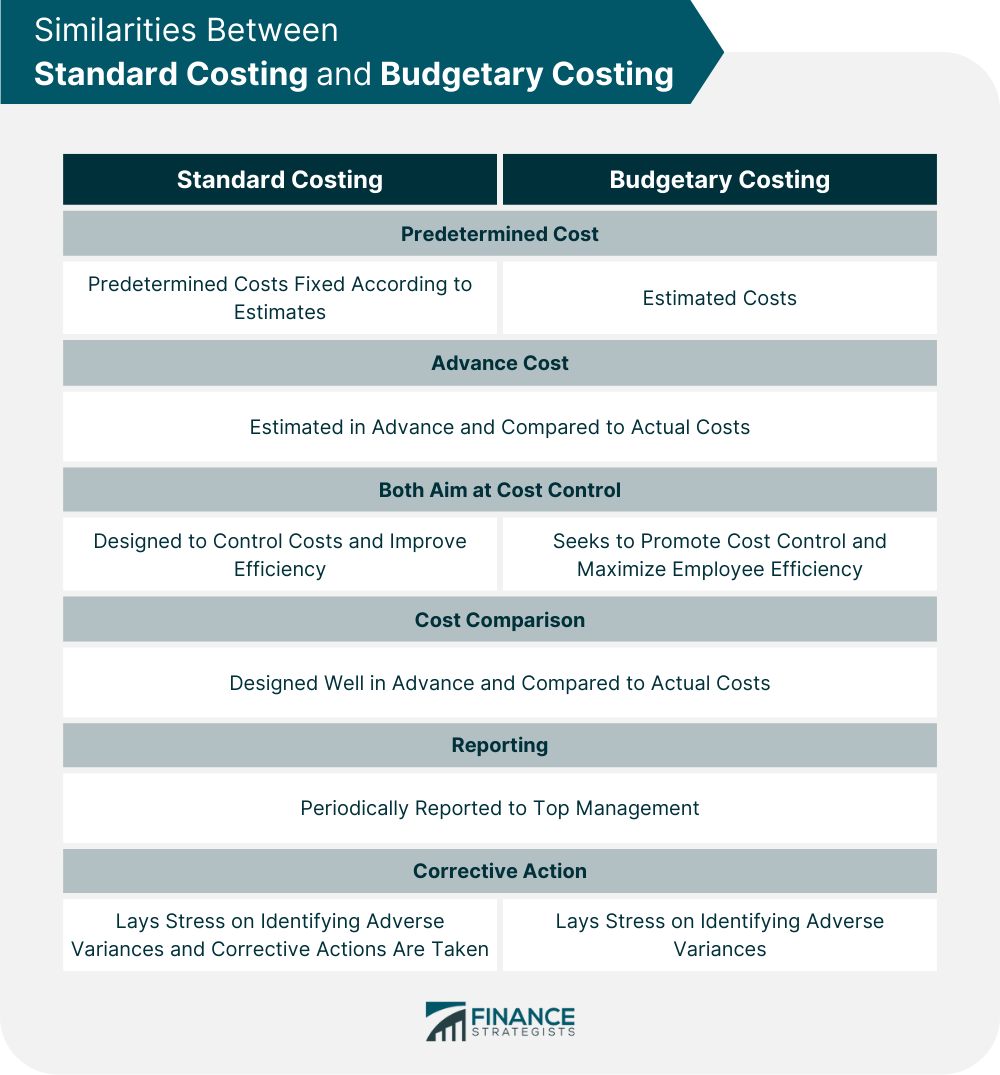

Similarities Between Standard Costing and Budgetary Costing

Basis of Similarities

Standard Costing

Budgetary Costing

Predetermined

costStandard costs are predetermined costs fixed according to estimates.

Budgetary costs are also estimated costs.

Advance cost

Standard costs are estimated in advance and compared to actual costs.

Budgetary costs are also estimated in advance and compared to actual costs.

Both aim at

cost controlStandard costs are designed to control costs and improve efficiency.

Budgetary costing also seeks to promote cost control and maximize employee efficiency.

Cost

comparisonStandard costs are designed well in advance and compared to actual costs.

These advanced estimated costs are compared to actual costs.

Reporting

Standard costs are periodically reported to top management.

Budgetary costs are also reported to management periodically.

Corrective

actionStandard costing lays stress on identifying adverse variances and corrective actions are taken.

Budgetary control lays stress on identifying adverse variances.

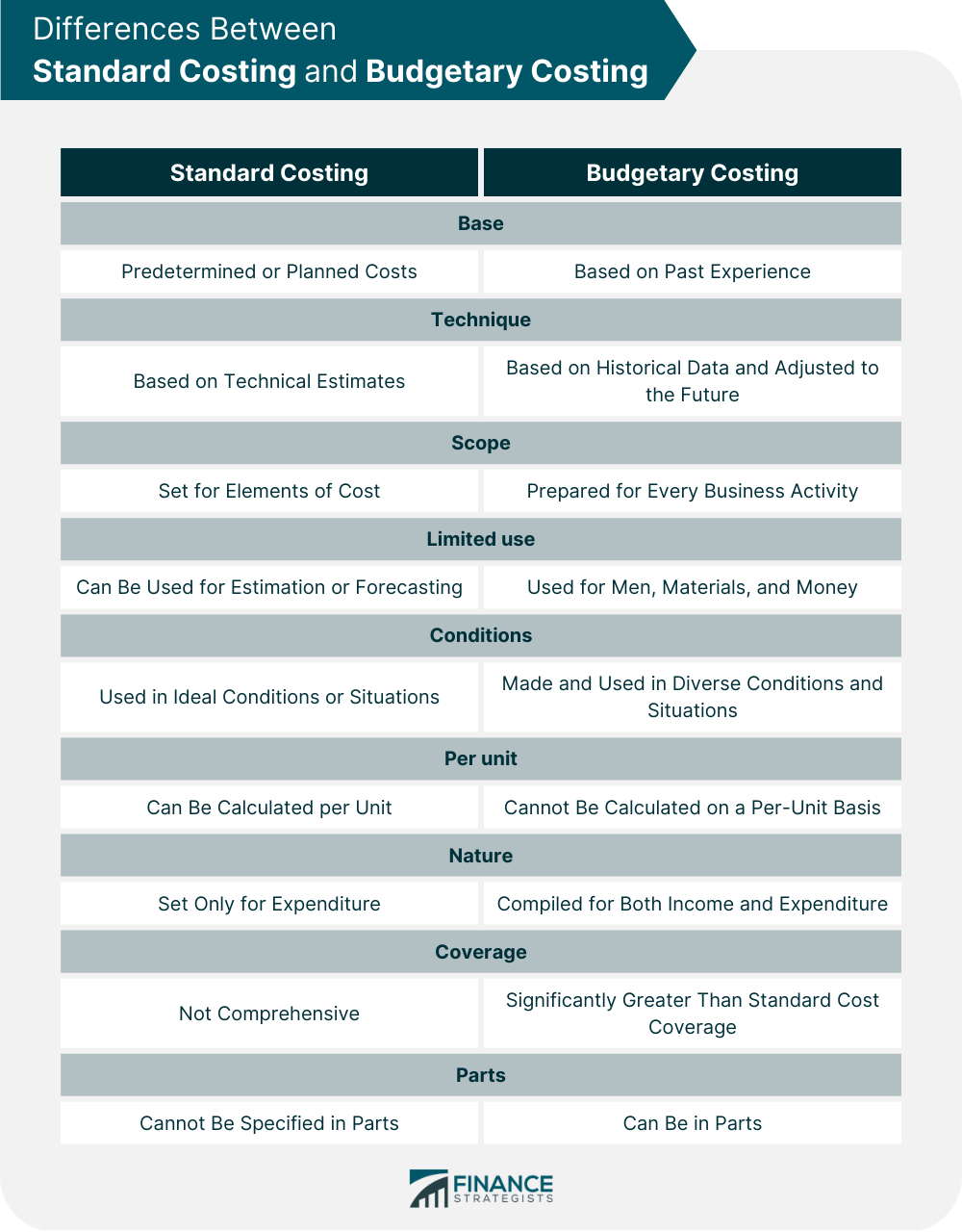

Differences Between Standard Costing and Budgetary Costing

Basis of Difference

Standard Costing

Budgetary Costing

Base

Standard costs are predetermined or planned costs.

Budgetary costs are based on past experience.

Technique

Standard costs are based on technical estimates.

Budgetary costs are based on historical data and adjusted to the future.

Scope

The standards are set for elements of cost.

Budgets are prepared for every business activity.

Limited use

Standard costs can be used for estimation or forecasting.

Budgets are used for men, materials, and money.

Conditions

Standard costs are used in ideal conditions or situations.

Budgets are made and used in diverse conditions and situations.

Per unit

Standard costs can be calculated per unit.

Budgetary costs cannot be calculated on a per-unit basis.

Nature

Standards are set only for expenditure.

Budgets are compiled for both income and expenditure.

Coverage

Standard cost is not comprehensive (i.e., it is limited only to cost operations).

Budgetary cost coverage is significantly greater than standard cost coverage.

Parts

Standard costs cannot be specified in parts.

The budget can be in parts (only the cash budget).

Similarities and Differences Between Budgeting And Standard Costing FAQs

Standard Costing is the most effective way to control costs. It provides criteria that can be used to evaluate and compare the operating performance of executives.Essentially, Standard Costing is a technique of cost calculation and control. Standard Costs are prepared and used to clarify the final results of a business.

Budget costs are estimated costs that are used only for planning or research purposes to understand the size of the company and make business decisions.

The similarities between budgeting and Standard Costing are the following:predetermined cost sandard costs are predetermined costs fixed according to estimates.Budgetary costs are also estimated costs.Advance costStandard Costs are estimated in advance and compared to actual costs.Budgetary costs are also estimated in advance and compared to actual costs.Both aim at cost controlStandard Costs are designed to control costs and improve efficiency.Budgetary costing also seeks to promote cost control and maximize employee efficiency.

The differences between budgeting and Standard Costing are:baseStandard Costs are predetermined or planned costs.Budgetary costs are based on past experience.TechniqueStandard Costs are based on technical estimates.Budgetary costs are based on historical data and adjusted to the future.Scopethe standards are set for elements of cost.Budgets are prepared for every business activity.

Standard Costing can be performed at any time or place.Budgeting confines the timing of costs to predetermined times only.Both are useful in budgeting for future earnings and expenses, present decision-making, and control over the existing operations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.