Prime cost is the aggregate of direct material cost, direct labor cost, and direct expenses. It is also known as 'flat cost,' 'first cost,' or 'direct cost.' Once the cost of raw materials has been ascertained, the cost of direct labor and direct expenses is known. The prime cost can be calculated by adding up the three figures. Prime costs are the sum of direct costs incurred during the manufacture of a product. These costs comprise raw material and direct labor in the production process but do not include indirect expenses (e.g., factory rent or supervisor's salary). The method involves calculating the contribution margin of a product, and it shows the ability of a product to cover fixed expenses, as well as its profitability. Prime costs play a vital role in cost and management accounting. These costs are the crucial ingredient required to calculate the contribution margin, determine prices, forecast sales and profits, and make decisions. Prime costs constitute direct costs and refer to expenses directly associated with each unit of the manufactured product. These costs usually comprise the following: Tangible goods, materials, or supplies directly identified with a particular product. These are raw materials in the production process converted into finished goods. For example, sugar and strawberry pulp are direct materials used for the manufacture of strawberry jam. Workers or employees directly involved in the production of a particular product. Direct laborers apply their skills during the production process to produce the finished goods. Hence, the direct labor cost includes wages paid to the direct laborers in an organization, such as salaries paid to the chefs in a restaurant. Any direct expenses other than material and labor are included in the prime cost, irrespective of whether they are variable, semi-variable, or stepped fixed. For example, a commission or bonus awarded to a salesperson who works as an intermediary between the producer and buyer on achieving a goal would also be included as indirect labor cost. Compared to direct costs, indirect costs are not included in the calculation of prime costs. Indirect expenses refer to the costs incurred in production that cannot be directly associated with a single output unit. Examples include factory rent, depreciation, salaries for supervisors and guards, utility bills, and more. The prime cost per unit is often calculated to determine the production cost of each unit of output so that the organization could fix a minimum price. However, indirect expenses are incurred and paid off aggregately, indicating why the total bill arrives annually or monthly. Such a development makes the indirect expenses tricky to predict and spread and allocate these costs to the entire output of the firm. This concept is supported by the marginal costing system of accounting, which only charges the prime costs to the cost of inventory, which is deducted from the amount of revenue to arrive at the contribution margin. The contribution margin earned is then used to set off indirect expenses. After the deduction of indirect costs, the leftover contribution margin refers to the marginal profit earned by the company that year. Prime cost = Direct materials cost + Direct labor cost This formula shows that prime cost is the sum of all the production costs (those that are directly incurred) relative to the manufacture of goods. In 2019, Elegance Limited, a sofa shop, manufactured 10 sets of sofas. They incurred the costs shown below. In total, the laborers worked for 200 hours. The total direct material of Elegance Limited amounts to timber + foam + cloth = $50,000 + $25,000 + $37,000 = $112,000. The total direct labor cost of Elegance Limited amounts to 100 x 200 = $20,000. Other direct expenses are $7,000 in total. Hence, the prime cost of Elegance Limited for the year ended 2019 amounts to $112,000 + $20,000 + $7,000 = $139,000. Prime costs are a crucial metric to measure the profitability of a product and determine the selling price. A negative contribution margin implies that sales and production result in losses, whereas a positive contribution margin implies that sales and production result in profits.Prime Cost: Definition

Prime Cost: Explanation

Direct Material

Direct Labor

Direct Expenses

Discussion

Formula

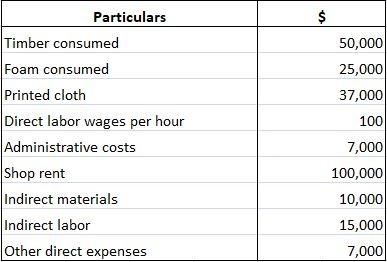

Example

Solution

Conclusion

Prime Cost FAQs

Prime cost is the aggregate of direct material cost, direct labor cost, and direct expenses. It is also known as ‘flat cost,’ ‘first cost,’ or ‘direct cost.’ Once the cost of raw materials has been ascertained, the cost of direct labor and direct expenses is known. The prime cost can be calculated by adding up the three figures.

Indirect expenses are not included in the calculation of prime costs. Indirect expenses refer to the costs incurred in production that cannot be directly associated with a single output unit. Examples include factory rent, depreciation, salaries for supervisors and guards, utility bills, and more.

The main difference between prime cost and variable cost is that prime cost includes all of the company's fixed expenses, while variable cost only includes the costs that fluctuate with production. As a result, prime cost is usually higher than variable cost. Additionally, prime cost is more stable and easier to predict than variable cost.

If your prime cost is too high, it means that your production costs are also high. As a result, you will need to find ways to reduce your costs so that you can remain competitive in the marketplace. One way to do this is to renegotiate contracts with your suppliers. Additionally, you can look for ways to become more efficient in your operations, such as automating some processes or investing in technology. Finally, you can also speak to your financial advisor or accountant for more specific advice on how to reduce your overall production costs.

As a business owner, you can use the prime cost information to identify which products are profitable and which ones are not. You could then raise or lower the prices of unprofitable products, or discontinue production altogether. Additionally, you can also use prime cost figures to negotiate better deals with your suppliers and reduce your overall production costs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.