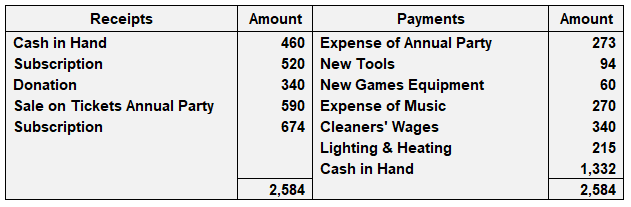

When you understand the difference between a receipts and payments account and an income and expenditure account, it should be a simple matter to convert the former into the latter. As a general guide, this article shows a series of steps you can follow to convert a receipts and payments account into an income and expenditure account. First, exclude the following: In turn, include the following: Lastly, provision for bad debts and depreciation on fixed assets should be made and charged to the income and expenditure account. When preparing an income and expenditure account, you should pay special attention to the following items: This amount is received as per the will of the deceased person. If the amount is greater, it is normally treated as a capital item and shown as a liability in the balance sheet; otherwise, it is treated as income and entered in the income and expenditure account. Sometimes, a portion of the legacy is transferred to the income and expenditure account. If nothing is clear, it may be treated as income or capitalized, but a footnote of its treatment should be given. The treatment regarding the donations may vary. Large amounts are capitalized and shown as liabilities on the balance sheet. Some donations are simply treated as income and are taken to the credit side of income and expenditure account. If the amount is moderate, it can be treated in any manner, but a footnote should be given regarding the treatment of such amounts. Also, if donations are given for a specific purpose (e.g., construction of a room, acquisition of sports equipment, and so on), then it should be capitalized and will be shown as a liability on the balance sheet. Two main methods are used to deal with amounts received on account of life membership subscriptions: If there is a specific fund and there are certain items of expenditure relating to such a fund, then the expenditure should not be shown in the income and expenditure account. Instead, it should be subtracted from its relative fund in the balance sheet. For example, if there is tournament fund in the receipts and payments account and tournament expenses are also given, then tournament expenses should not be entered in the income and expenditure account. Instead, they should be deducted from the tournament fund in the balance sheet. The cash received on account of old sports equipment and old newspapers is classified as recurring income. Therefore, it should be included in the income and expenditure account. Sale of an old asset is deducted from a particular asset in the balance sheet. The profit or loss made on the sale of an old asset should be recorded in the income and expenditure account. If incomes are greater, this is referred to as excess of income over expenditure (or surplus balance). If expenditures are greater, this is referred to as excess of expenditure over income (or deficit balance). Explanatory Note: Any amount of credit to income will be shown as a liability on the balance sheet. For the year ended 31 March 2017, the treasurer of the Youth Center produced the following summary of receipts and payments. Required: Prepare an income and expenditure account for the year ended on 31 March 2017.

Accounting Treatment of Important Items

Legacies

Donations

Life Membership Subscriptions

Items Relating to a Specific Fund

Sale of Old Newspapers and Sports Equipment

Sale of Old Assets

Closing an Income and Expenditure Account

Example

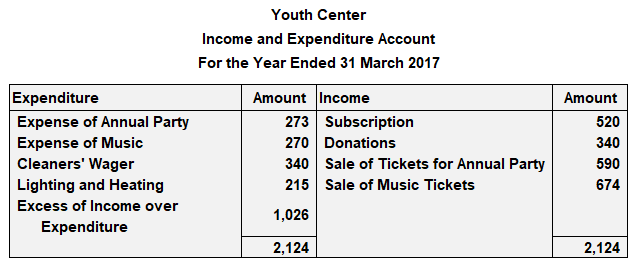

Solution

Note: Expenditure incurred on the purchase of new tools and new games equipment has not been entered in the account because this is paid expenditure (i.e., it will be treated as an asset).

Preparation of Income and Expenditure Account From Receipts and Payment Account FAQs

The steps to convert a receipts and payments account into an income and expenditure account include the following:1. All income relating to the current period but not yet received2. All expenditures relating to the current period but not yet paid

Legacies is the amount received as per the will of the deceased person. If the amount is greater, it is normally treated as a capital item and shown as a liability in the balance sheet; otherwise, it is treated as income and entered in the income and expenditure account.

The treatment regarding the donations may vary. Large amounts are capitalized and shown as liabilities on the balance sheet. Some donations are simply treated as income and are taken to the credit side of income and expenditure account.

Two main methods are used to deal with amounts received on account of life membership subscriptions:1. When the amount is relatively small and there is a regular flow of members who take advantage of the facility each year, then the item is regarded as income and entered in the income and expenditure account.2. When the amount is large, then a certain percentage is treated as income each year. For example, 10% is treated as income, meaning that the complete income is taken over the 10-year period.

If incomes are greater, this is referred to as excess of income over expenditure (or surplus balance).If expenditures are greater, this is referred to as excess of expenditure over income (or deficit balance).Keep in mind that any amount of credit to income will be shown as a liability on the balance sheet.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.