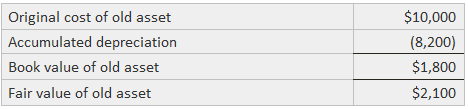

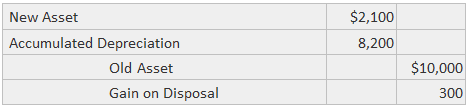

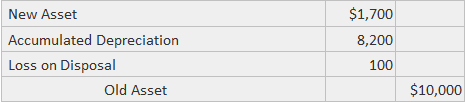

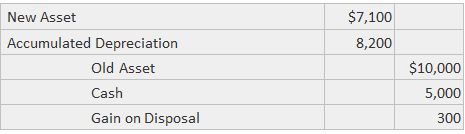

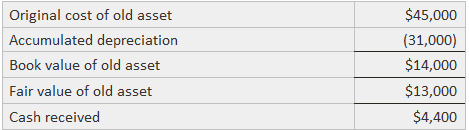

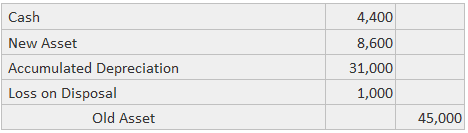

When an asset of one kind is exchanged for an asset of another kind, the preferred measurement of the new asset's cost is the fair value of the asset given up. The simplest example of this type of exchange is a purchase for the cash. The journal entry is straightforward, as seen for this $100,000 acquisition: Noncash transactions are more difficult to account for. The practice was sufficiently unsettled to deal with nonmonetary transactions. The basic principle is: An important exception to this principle was drawn for exchanges of similar productive assets, which were defined as assets "of the same general type, that perform the same function or that are employed in the same line of business." Thus, the GAAP call for exchanges of dissimilar operating assets to be recorded as if the following conditions apply: If no cash is given up, the new asset is recorded at the estimated value of the old one, and a gain or loss is recorded for the difference between that value and the old asset's book value. Suppose we have the following information about an asset: In this case, the following journal entry would be made: If the fair value is lower than the book value, a loss is recorded. If the estimate of the fair value of the new asset differs significantly from the estimated fair value of the old asset, the accountant should use the valuation approach that is more reliable. If, for example, the fair value of the new asset acquired is known more reliably than the value of the old one, and that value is only $1,700, this journal entry would be recorded: If both values are viewed as equally reliable, conservatism would encourage the selection of the smaller figure. It seems unlikely that an exchange would be negotiated where the parties are not reasonably certain of the values of the assets given up and received. However, the book value of the nonmonetary asset transferred from the enterprise may be the only available measure of the transaction. In most cases, the buyer of a new asset that exchanges an old asset also gives up cash. The cost of the new asset is considered to be the sum of the cash paid and the fair value of the old asset. Assuming the same facts as in the above example, suppose that $5,000 cash is also given up. The following entry would be made: Again, a loss would be recorded if the old asset's book value exceeded its fair value. When the firm gives up an old asset and receives cash, the cost of the new asset is measured as the difference between the fair value of the old asset and the cash received. For example, assume the following facts: The cost of the new asset would be $8,600, or $13,000 less $4,400, and this entry would be recorded as below. The loss is equal to the difference between the book and the fair value of the old asset.Definition and Explanation

Accounting for nonmonetary transactions should be based on the fair values of the assets (or services) involved.

Thus, the cost of a nonmonetary asset acquired in exchange for another nonmonetary asset is the fair value of the asset surrendered to obtain it.

Exchanges Without Cash

Exchanges With Cash Given

Exchanges With Cash Received

Exchange of Dissimilar Nonmonetary Assets FAQs

An exchange of dissimilar nonmonetary assets is a transaction in which two or more parties trade different types of non-financial assets with each other.

There are many reasons why two parties might want to engage in an exchange of dissimilar nonmonetary assets, including tax benefits, the need to unload certain assets, or simply to acquire a new type of asset.

There are several things to consider before engaging in an exchange of dissimilar nonmonetary assets, such as the fair market value of the assets involved, any potential tax implications, and whether or not the assets are actually compatible with each other.

The parties should first consult with professionals in order to determine the fair market value of the assets involved and to ensure that the exchange will be conducted legally and without any negative tax implications. Once these details have been ironed out, the actual exchange of assets can take place.

Some potential pitfalls of exchanging dissimilar nonmonetary assets include receiving assets that are not as valuable as expected, or encountering difficulties in exchanging the assets in a timely and efficient manner. It is therefore important to be well-informed and to consult with professionals before engaging in this type of transaction.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.