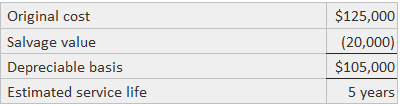

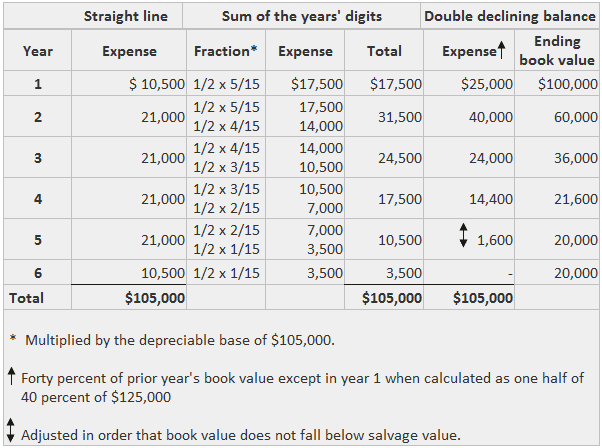

Since operating assets are purchased and retired throughout the year, companies must overcome the problem of determining how much depreciation expense should be recorded for the part of the year during which acquired or retired assets are used. The basic principle holds that the company should adopt a convention for computing the partial year's expense and use it consistently. In the event that abiding by the convention will produce a material misstatement (e.g., if a large acquisition occurs early or late in the year), a more precise calculation should be made. Among the possible conventions are the following: Due to their simplicity and the likelihood that they will not be materially different from a more precise calculation, the half-year and modified half-year conventions are the most commonly used. This example illustrates how to calculate the partial year's depreciation expense under the straight-line method, sum-of-the-years' digits method, and double-declining method. First, consider the following information: Under the half-year convention, a half-year's depreciation is charged to the year of acquisition. The subsequent year's charges depend on the chosen method and the disposal date. An illustration of partial year's depreciation under the half-year convention is shown below: Under the straight-line method, years 1 and 6 receive only one-half of a full year's expense. The other four years receive a full year's expense, which is computed normally. Under the sum-of-the-years' digits method, the calculations are more difficult after the first year because each year's expense is the sum of two half-years' depreciation. The last year's expense is simply one-half of the amount that would have been reported if there had been no need to allocate between years. Under any of the declining-balance methods, calculation of a partial year's depreciation is needed only in the first year. Thereafter, the rate can be multiplied by the prior year's ending book value to find the expense. As before, the last year's expense is modified in order to ensure that the book value does not fall below the salvage value.Explanation

Example

Partial Year’s Depreciation FAQs

Depreciation is the process of allocating the cost of plant and equipment to the period in which the enterprise receives the benefit from these assets.

Since operating assets are purchased and retired throughout the year, companies must overcome the problem of determining how much Depreciation expense should be recorded for the part of the year during which acquired or retired assets are used.

In the event that abiding by the convention will produce a material misstatement, a more precise calculation should be made. Among the possible conventions are the following: 1. Actual days used 2. Actual months used 3. One-half year’s charge in the year of acquisition or disposal 4. Full year’s charge when acquired in the first half of the year or sold in the second half; no charge when acquired in the second half of the year or sold in the first half 5. Full year’s charge in the year of acquisition and none in the year of disposal

Due to their simplicity and the likelihood that they will not be materially different from a more precise calculation, the half-year and modified half-year conventions are the most commonly used.

Under any of the declining-balance methods, calculation of a partial year’s Depreciation is needed only in the first year. Thereafter, the rate can be multiplied by the prior year’s ending book value to find the expense.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.