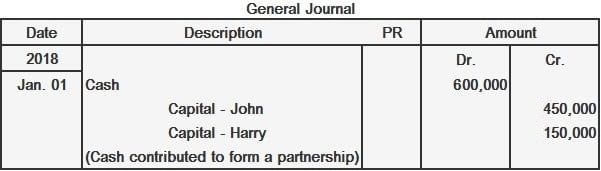

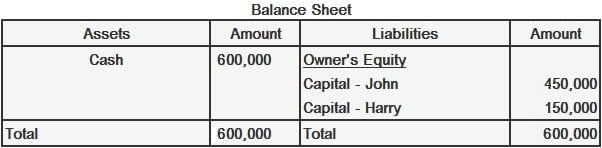

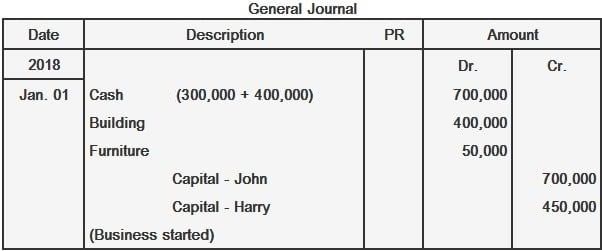

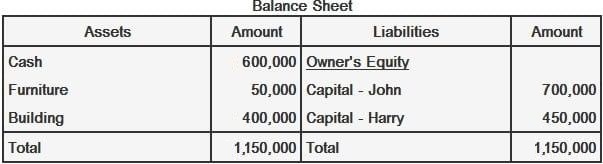

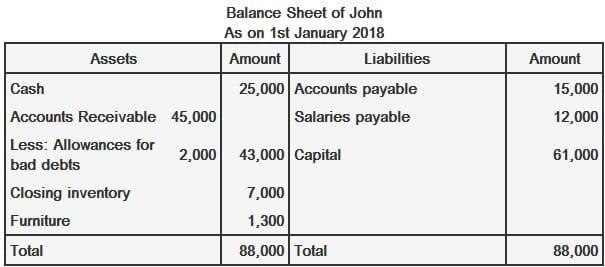

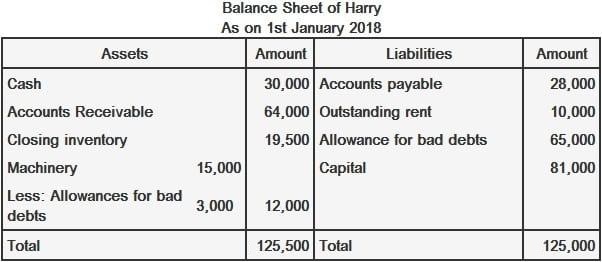

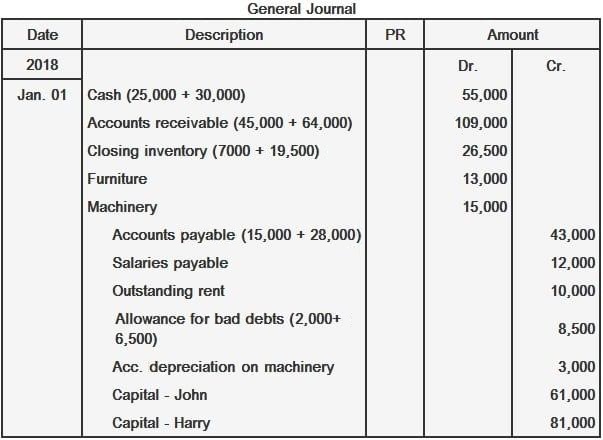

When a partnership is formed, each partner contributes capital in the form of either cash or a non-cash asset. Separate capital accounts are opened to record each partner's investment. The partners can invest in the business in any of the following ways: If a contribution is made in cash, the cash account is debited and the respective partner's capital account is credited with the contribution. For example, suppose that A and B form a partnership contributing $100,000 and $50,000, respectively, in the form of cash. The journal entry will be as follows: John and Harry formed a partnership on 1 January 2018. John contributed $450,000 and Harry $150,000. Required: If non-cash assets are invested, debit is given to assets invested at the amount agreed by all the partners, and credit is made to the partner's capital. For example, suppose that A and B form a partnership. A invests $100,000 in the form of cash, whereas B adds buildings to the partnership, the agreed value of which is $80,000. In this case, the journal entry will be: John and Harry formed a partnership on 1 January 2018. John contributed cash amounting to $300,000 and buildings totaling $400,000. Harry contributed cash of $400,000 and furniture amounting to $50,000. Required: A partnership may also be formed by combining two or more existing businesses. For this purpose, the journal entry will be as follows: John and Harry both have their own businesses. They agree to form a partnership on 1 January 2018 by combining their businesses. On this date, their balance sheets were as follows: All assets and liabilities of the two companies will be taken over by the firm at book value. Required:

By Contributing Cash

Example

Solution

By Contributing Non-Cash Assets

Example

Solution

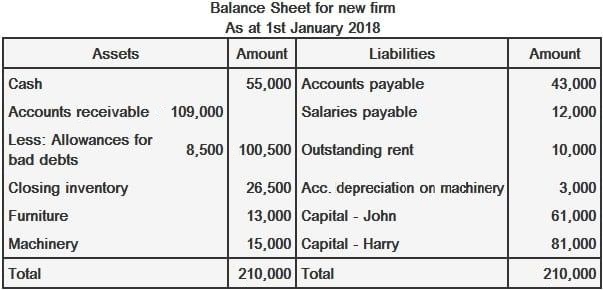

By Combining Individual Business

Example

Solution

Procedure to Open Books of Partnership FAQs

All accounting transactions are recorded in the book of accounts. The first transaction that occurs when a firm which is not registered with any authority or agency is formed, or when a firm decides to form a Partnership, this will be recorded as an opening transaction in the defined books of accounts for this purpose.

The balance of each partner’s capital account after the opening transaction is equal to his original investment. The total assets and liabilities of the firm are equal to the sum of assets and liabilities of all partners after this transaction.

The book value or cost of any asset, if not sold, is its original purchase price. The costs incurred to buy an asset are added up to determine this sum. Assets whose costs have been amortized are valued at net liquidation value which is always lower than the amortized cost. Book value of a firm is the sum of cost values of all its assets and any total liabilities as stated in its books of accounts.

When a Partnership is formed, each partner contributes capital either in cash or non-cash asset form. Separate capital accounts are opened to record this.

If a partner contributes cash, his capital account is increased by that amount and it is decreased if he gives away non-cash assets such as land or building.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.