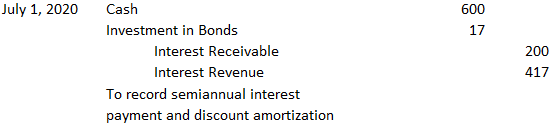

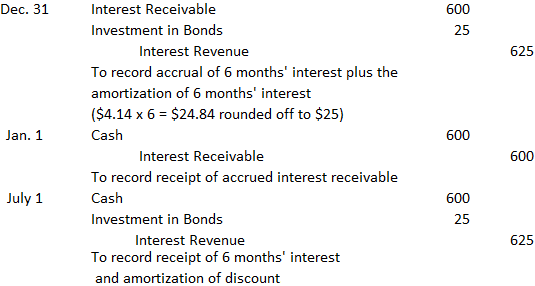

Accountants can use either the straight-line method or the effective interest method to amortize the bond discount or premium. In practice, if there are material differences between the two methods, the effective interest method should be used. However, for ease of illustration, the straight-line method is used in this article. Regardless of the method that you apply as an accountant, the discount is amortized by debiting the Investment in Bonds account. The premium is amortized by crediting the Investment in Bonds account. This procedure ensures that after the discount or premium is fully amortized, the investment account will reflect the bond's maturity value. To demonstrate these concepts, we will continue with the example of the Cinzano Corporation mentioned in another article on this website. The first interest payment day is 1 July 2020. The following entry would be made to record the receipt of the cash interest and the amortization of the discount: In this entry, Cash is debited for $600, which is the full 6 months' interest payment ($12,000 x 0.05). The Investment in Bonds account is debited for four months of discount amortization. The total discount is $240 and is amortized over the remaining 58 months of the bond's life at the time of issue. This equals $4.14 ($240 + 58 months — $4.14) per month, and 4 months' amortization from 1 March 2020 to 1 July 2020 is $16.56 ($4.14 x 4). This is rounded off to $17 in the journal entry. Interest revenue is credited for $417. This $417 consists of 4 months' cash interest plus $17 of the amortized discount. Note that from the investor's perspective, the discount increases interest revenue, and from the issuer's point of view, it increases interest expense. Cinzano Corporation should make the following set of journal entries each year until the bonds mature or until they are sold. The corporation has a year-end of 31 December. These examples illustrate the accounting procedures used for discounts. Premiums are handled in a similar manner except that the premium decreases interest revenue and is recorded by crediting the Investment in Bonds account.Example

Amortizing the Bonds Discount or Premium FAQs

One of the biggest misconceptions surrounding amortizing discounts and premiums is that they should never be negative. This is not the case; however, you must follow certain guidelines when it comes to reporting negative amounts on your balance sheet if you choose to take them into account in determining net income. You may also want to consult your company's counsel on the matter.

Amortizing a discount results in reporting more interest revenue while amortizing a premium results in reporting less interest revenue.

You should amortize the entire amount from the transaction in one period. You can also ask your company's counsel if they have any additional guidelines for this matter. As with all Accounting Procedures, there are always exceptions.

With the straight-line method, you are debiting more interest revenue each year until there is no remaining bond discount or premium. The effective interest method will allow you to record more interest revenue in early years and less interest revenue in later years.

Sellers can either accumulate the interest income in a suspense account and then close it at maturity, or they can use the proportionate method, which is to debit cash for the full interest expense on each coupon date. Paying straight-line amortization of bond discount or premium over the life of the bond is very complicated and not recommended.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.