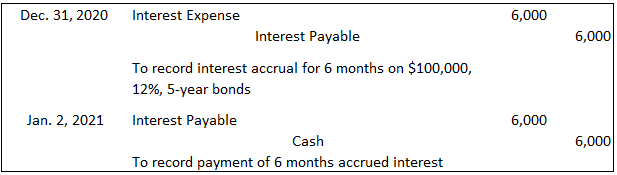

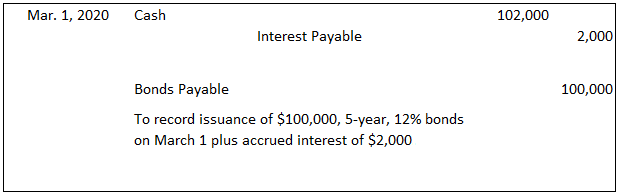

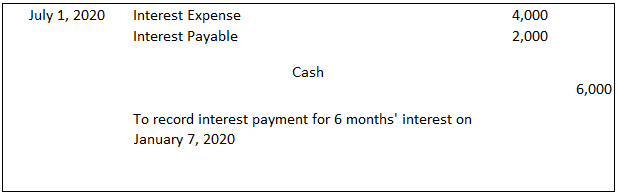

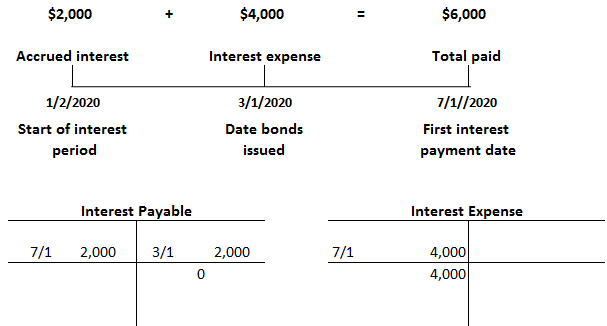

Bonds are issued at par or face value if the stated interest rate equals the prevailing rate for similar investments at the issue date. Because bonds can be issued on an interest date or between interest dates, both cases will be discussed. If bonds are issued at par or face value on an interest date, the entry is straightforward: Cash is debited and Bonds Payable is credited for the total dollar amount of the bond issue. Suppose that on 2 January 2020, the Valenzuela Corporation issues $100,000, 5-year term bonds with a stated interest rate of 12%. The bonds pay interest every 2 January and 1 July. The bonds were issued to yield 12%, which is another way of saying that they were issued at par, and thus the company received the full $100,000. The journal entry to record this bond issue is: The Valenzuela Corporation is required to make semiannual interest payments of $6,000 or $100,000 x 6%. The entry on 1 July 2020 is: The next interest payment is due on 2 January 2021. The corporation's year-end is 31 December, and the firm must make an adjusting entry to record interest expense for the 6-month period from 1 July to 31 December. This adjusting entry and the entry to record the subsequent payment are: In this case, the interest accrual is for the entire 6-month period because the last interest payment was on 1 July. If the year-end was any date other than 31 December, the interest accrual would be for 6 months or less. Bonds are often issued between interest dates. When this occurs, investors pay the issuing corporation for the interest that has accrued since the last interest date. This is because investors receive the entire 6 months' interest on the next interest payment date, regardless of how long they have held the bonds. This procedure has definite record-keeping advantages for the issuer, whether or not the bonds are registered. If the bonds are registered, the corporation does not have to maintain records concerning when each of the particular bonds in the bond issue was purchased or to compute individual partial interest payments. Interest on unregistered or coupon bonds is paid by authorized banks upon presentation of the coupon. Banks, however, will not honor a partial coupon. These problems are alleviated by the fact that the accrued interest is collected from the investors when the bonds are sold. This allows the corporation to pay all of the investors the full 6 months' interest. Suppose that the Valenzuela Corporation issues $100,000, 5-year, 12% bonds on 1 March 2020. The bonds, dated 2 January 2020, pay interest semiannually on 2 January and 1 July. In this situation, the investor must pay the Valenzuela Corporation for 2 months of accrued interest (from 2 January to 28 February), or $2,000 ($100,000 x .06 x 2/6 = $2,000). The entry to record this transaction is: Several points should be emphasized about this entry. Bonds Payable is always credited for the face amount of the issue, and so the accrued interest element must be accounted for separately. This is done by crediting Interest Payable for the 2 months of accrued interest, or $2,000. Interest Payable is credited because these funds will be repaid on the next interest date. Cash is debited for the entire proceeds. When the next interest payment is made on 1 July, the following entry is recorded: In this entry, Cash is credited for $6,000, Interest Payable is debited for $2,000, and Interest Expense is debited for $4,000. The result is that there is a zero balance in the Interest Payable account and a $4,000 balance in the Interest Expense account. This $4,000 balance represents the actual interest expense that the Valenzuela Corporation incurred from 1 March 2020 to July 1, 2020 ($100,000 x .06 x 4/6). These relationships are shown in the diagram below and the relevant T-accounts.Bonds Issued on an Interest Date

Example

Bonds Issued At Par Between Interest Dates

Example

Bonds Issued At Par or Face Value FAQs

Bonds are issued at par when they are sold for their face value. This means that if a firm were to issue $3 million in bonds with a 10% interest rate, it would receive $3 million and pay back the amount in future interest payments.

Issuing a bond on an interest date means that you issued a bond with a coupon of the current interest rate, which would be paid to the investor every year.

Companies can avoid paying any interest by issuing bonds at par or face value. This means they are selling them for their face value and this will be the amount they will pay to the investor.

When a company issues bonds between interest dates, they are selling those bonds for their par value or face value. This means that they will receive that amount from investors and they do not have to pay them any interest until the next payment date.

Companies would issue bonds between the interest payment dates if they do not have enough funds to pay them on that date. This means they need more time for people to buy their bonds and that will allow them to pay back investors when it is due.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.