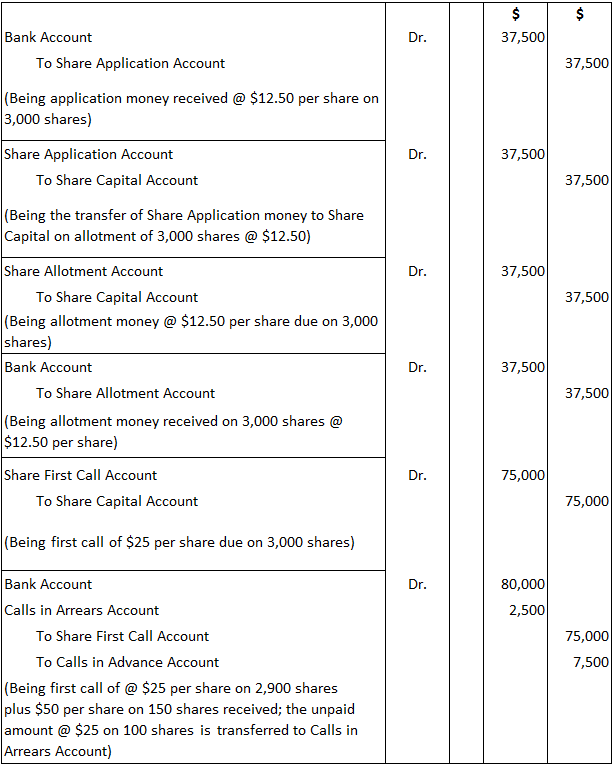

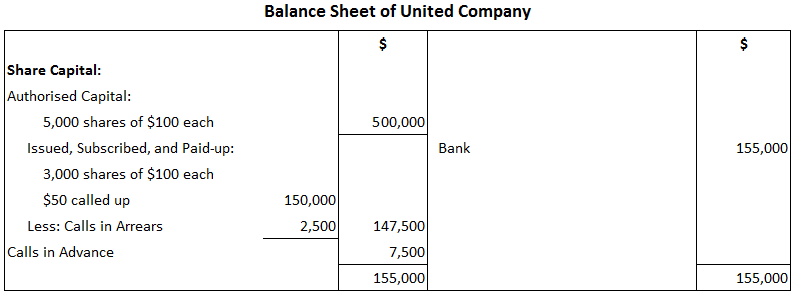

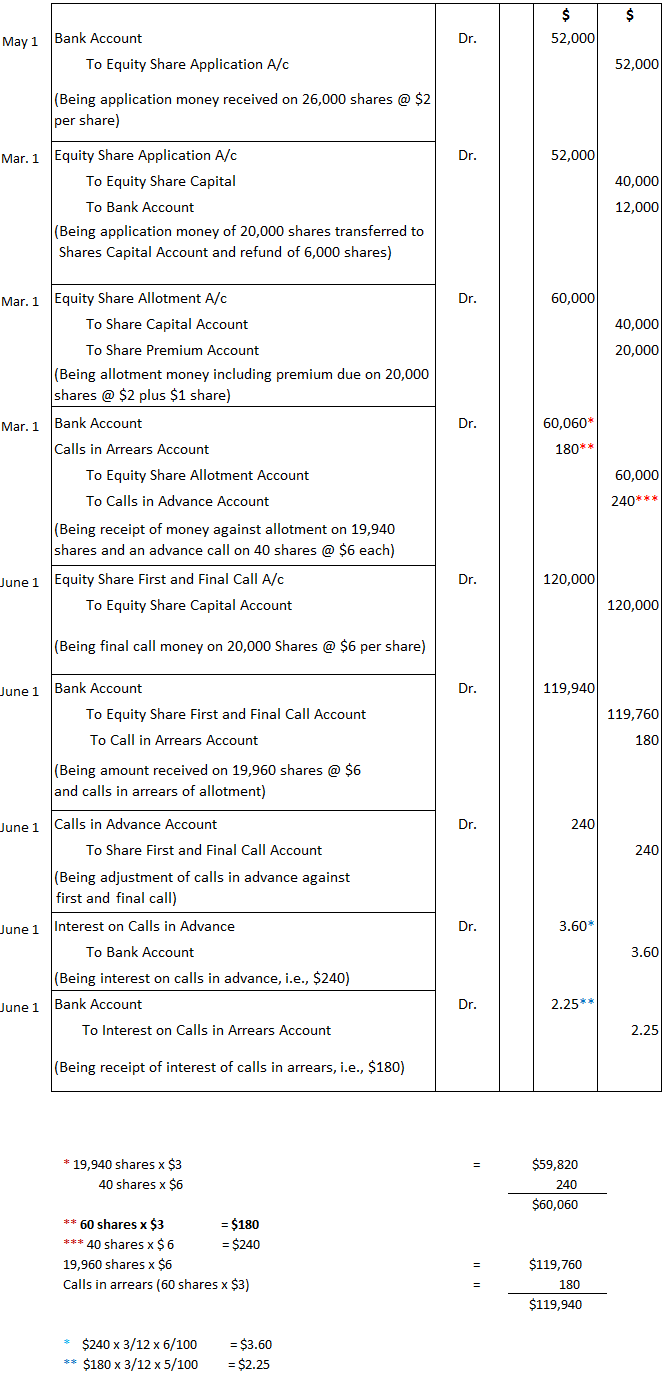

If any amount that is called in respect of a share is not paid before or on the date fixed for payment, such an amount is known as calls in arrears. The amount may be called by a company either as allotment money or call money. Thus, any default arising due to the failure to send the call money is known as calls in arrears. A separate account is opened for calls in arrears. Companies can charge interest on all such calls in arrears for the period that the amount remains unpaid. The rate used is 5% p.a. The total of calls in arrears is shown in the balance sheet as a deduction from the called-up capital. The money received by a company in excess of what has been called up is known as calls in advance. A company, if authorized by its articles, may accept calls in advance from shareholders. If such an amount, which has not been called, is received, the amount should be credited to a separate account known as the calls in advance account. However, the amount that is not called should not be credited to the capital account. A company may pay interest on such amounts received in advance at the rate of 6% p.a. No dividend is payable on this amount. The amount that is received will be adjusted toward the payment of calls as and when they become due. United Limited was registered with a nominal capital of $500,000 in shares of $100 each. 3,000 shares were issued for subscription and payable as to $12.50 on application, $12.50 on the allotment, and $25 three months after allotment, with the balance to be called up as and when required. All money up to allotment was duly received, but regarding the call of $25, a shareholder holding 100 shares did not pay the amount due. Another shareholder who was allotted 150 shares paid the entire amount of the shares. Show the journal entries needed to record the above transactions, including cash, and show how these appear in the balance sheet. X Limited issued 20,000 equity shares worth $10 each at $11 on 1 March, payable as follows: Applications were received for 26,000 shares. The directors made the allotment in full to applications demanding 10 or more shares, and they returned the money to applications for 6,000 shares. One shareholder who was allotted 40 shares paid the first and final call money along with the allotment money, while another shareholder who was allotted 60 shares did not pay the allotment money but paid along with the first and final call money. The directors decided to charge and allow interest, as the case may be, on calls in advance and calls in arrears. Give journal entries in the company's books.Calls in Arrears and Calls in AdvanceCalls in Arrears

Definition

Explanation

Calls in Advance

Definition

Explanation

Example: Calls in Arrears and Calls in Advance

Solution

Journal Entries

Balance Sheet

Illustration 2

Solution

Journal Entries

Calls in Arrears and Calls in Advance FAQs

Calls in arrears are money that is called up but has not been paid.

Calls in advance are money that is called over and above what has been called for.

If a call isn't paid then the company can charge interest on the amount of unpaid money.

Calls in arrears and advances are important because they give the company more flexibility to collect funds that may be needed. This can also help manage Cash Flow within a business.

Companies record these items with the journal entry of debit to the amount due, then credit cash or account receivable. If interest is being charged then a separate account called "interest in arrears" or "interest in advance" should be debited and credit to the capital accounts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.