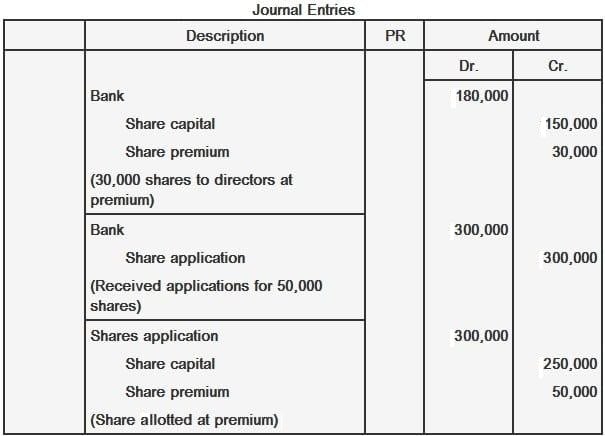

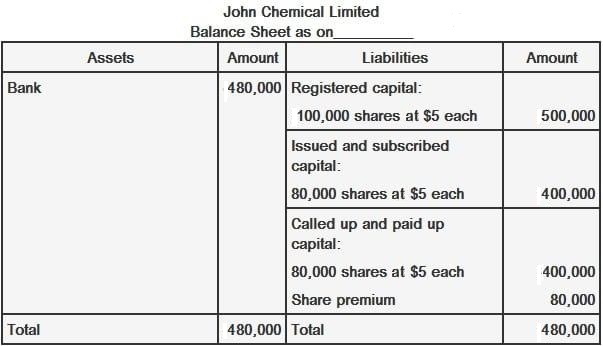

A company may issue its shares at a premium (i.e., a higher price than the face value), provided there is demand for such shares at a higher value. The premium received on issued shares must not be mixed with the share capital. Instead, it must be credited to a separate account known as the share premium account and shown as a separate item on the liability side of the balance sheet. If shares are issued to the directors or underwriters at a premium and the amount is received in a lump sum, the following entries should be made: If shares are issued at a premium to the public after the receipt of application money through the bank, the entries should be: John Chemical Limited has an authorized capital of $500,000 divided into 100,000 shares valued at $5 per share. 30,000 shares were issued to the directors and 50,000 shares to the general public at a premium of $1 per share. Subscriptions were received in full and these shares were allotted. Required: Give general entries and the balance sheet of the company.Definition and Explanation

Journal Entries for Issuance of Shares at a Premium

Bank ---------------------------- Dr

Share Capital ---------------------------- Cr.

Share Premium ---------------------------- Cr.

Share applications ---------------------------- Dr

Share Capital -------------------------------------- Cr.

Share Premium ------------------------------------- Cr.

Example

Solution

Issue of Shares at Premium FAQs

A company may issue its shares at a premium (i.E., A higher price than the face value), provided there is demand for such shares at a higher value.

The premium received on issued shares must not be mixed with the share capital. Instead, it must be credited to a separate account known as the share premium account and shown as a separate item on the liability side of the balance sheet.

Demand is an economic principle that refers to the willingness and ability of consumers to make discretionary purchases at a given price.

A liability is a debt or other obligation owed by one party to another party. In more direct terms, it is a payment or obligation for which a company is held liable by another party.

The term underwriter refers to a person or a group of people who are responsible for assessing different items that require taking on some sort of risk.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.