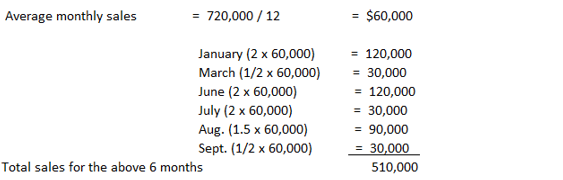

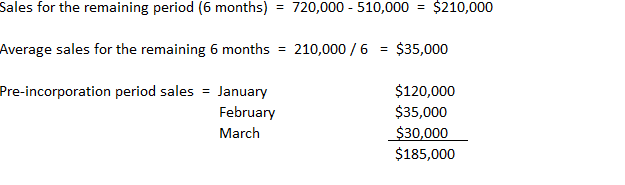

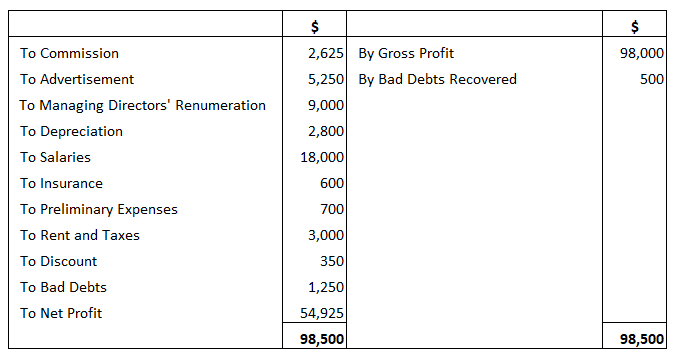

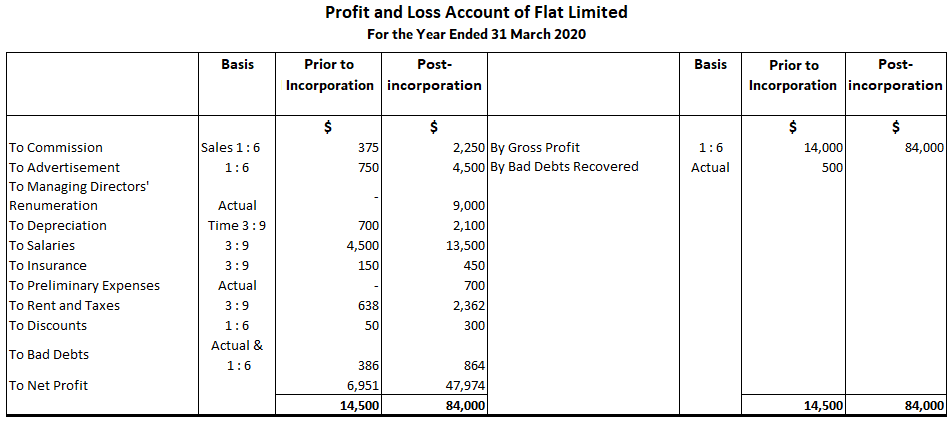

A company was incorporated on 30 April in order to acquire the business of a private firm as of 1 January. The company closes its books on 31 December. The gross profit for the whole period was calculated at $120,000. The sales for the month of August were 3 times the average, 2 times the average for January and July, 1.5 times for October and December, and it 0.5 times for November. Estimate the gross profit earned prior to incorporation. Let the average monthly sales be equal to 1. Therefore, sales for the 6 months are shown as follows: Total sales for the remaining 6 months: February, March, April, May, June, and September = 12 - 10.5 = 1.5. Therefore, average sales for the 6 months = 1.5 / 6 = 0.25, i.e., 1/4 of the average. As such, sales for January to April = 2 + 1/4 + 1/4 + 1/4 = 2, 3/4. In turn, sales ratio = 2 3/4 : 9 1/4 or 11/4 : 37/4 or 11 : 37. With this in mind: A company was incorporated on 1 April to acquire the running business of a partnership firm from 1 January. The account year ends on 31 December. Using the information shown below, calculate the sales ratio for the pre-incorporation and post-incorporation period. Post-incorporation period sales = $720,000 - 185,000 = $535,000 Therefore, the sales ratio of pre-incorporation and post-incorporation period is equal to 185,000 : 535,000 or 37 : 107. Flat Limited was incorporated on 1 July 2019 to take over the running business of Mr. Round, which would come into effect on 1 April 2019. The following profit and loss account was drawn up for the year ended 31 March 2020. The following details are available: Find the gross profit prior to incorporation and describe its treatment in the company's books.Question 1

Solution

August

3

January

2

July

2

October

1.5

December

1.5

November

0.5

Total sales for 6 months

10.5

Question 2

Solution

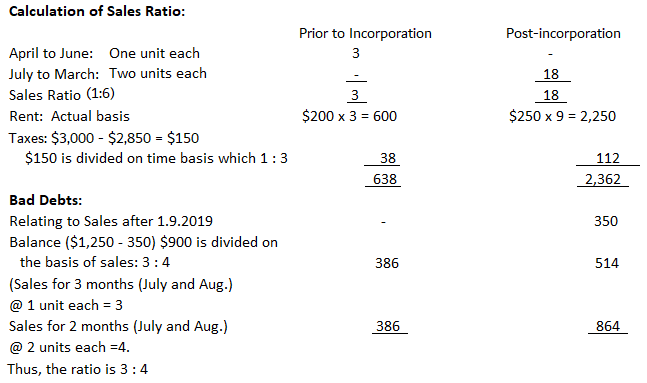

Question 3

Solution

Working

Profit or Loss Prior to Incorporation FAQs

Pre and post-incorporation have the same problems as those of the start and end of the financial year. For example, we cannot report sales on an accrual basis if we close books one day prior to incorporation. Also, there may be issues with depreciation and inventory valuation.

The term "profit prior to incorporation" refers to an entity's profits earned before it was formally registered as a company.

You can use the assessment method and the closing down method.

The assessment of tax on the prior period's profits depends upon whether it was earned within a separate legal entity before its incorporation or not. If the earnings were not earned within a separate legal entity, then they are attached to the owner.

Any adjustment to pre-incorporation debtors and creditors would have to be made on a case-by-case basis, taking into account the particular facts and circumstances of each situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.