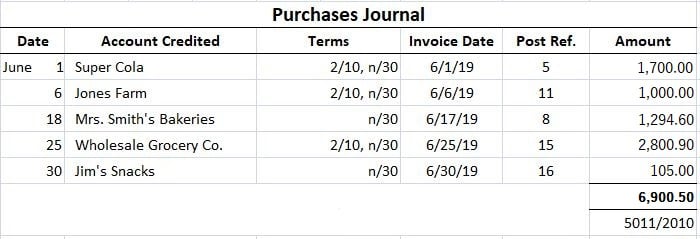

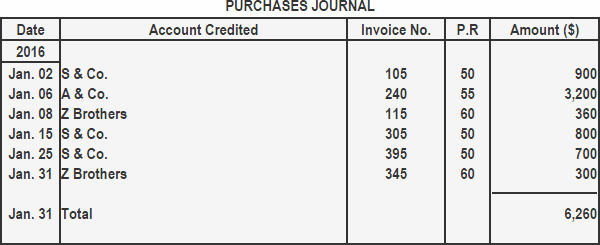

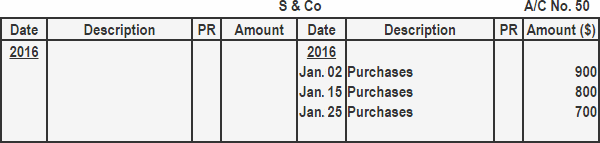

A purchases journal is a special journal used to record any merchandise purchased on account. The entries in this journal are made based on the invoice received from the supplier on the purchase date. Other names used for the purchases journal are the purchases book, purchases daybook, and the credit purchases journal. The purchases journal is mainly used to record merchandise and inventory purchases on credit. If these are the only transactions recorded in the purchases journal, then the journal is similar to the one shown in the example below. Purchase invoices are used to enter data into the journal. We are assuming that a periodic inventory system is in use and that all purchases are recorded at their gross amounts. Therefore, the amount column represents a credit to accounts payable and a debit to purchases at the full invoice price. The purchase journal has five columns, as shown in the format below. The purposes of these columns are as follows: Entries from the purchases journal are posted to the accounts payable subsidiary ledger and general ledger. The procedure for doing this is outlined below: Postings from the purchases journal follow the same pattern as postings from the sales journal. Each day, individual purchases should be posted to the vendor's account in the accounts payable subsidiary ledger. At the end of the month, the amount column in the journal is totaled, and this amount is posted as a debit in the general ledger purchases account. It is also posted as a credit in the general ledger accounts payable account. Finally, at the end of the month, a list of the individual subsidiary accounts is created. This list is often called the accounts payable trial balance (or a schedule of accounts payable). The balance in this list is compared with the balance in the general ledger accounts payable account. This procedure helps to verify that all the postings have been made correctly. Transactions from XYZ trading company for the month of January 2016 are listed below: Required: 1. Purchases journal 2. Accounts payable subsidiary ledger 3. General ledger 4. Schedule of accounts payablePurchases Journal: Definition

Purchases Journal: Explanation

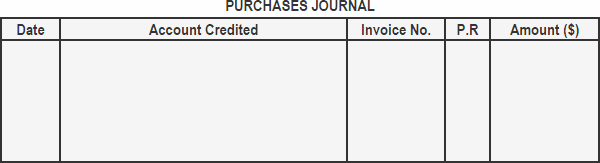

Purchases Journal Format

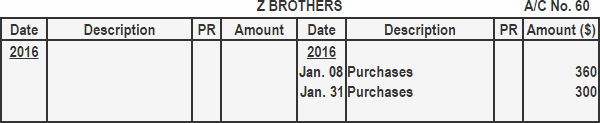

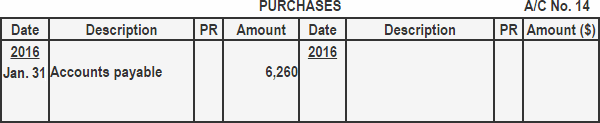

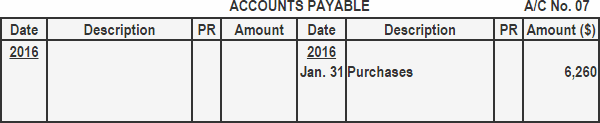

Posting the Purchases Journal

Example

Solution

Purchases Journal FAQs

A purchases journal is a special journal used to record any merchandise purchased on account. The entries in this journal are made based on the invoice received from the supplier on the purchase date.

The typical format for a purchases journal is as follows: date, supplier, invoice number, amount.

A purchases journal can be helpful in several ways. It can help you track the expenses of your business, which can be useful for tax purposes. It can also help you keep an accurate inventory of the products and services you offer. This can be helpful if you need to recall a product or service, or if you are considering expanding your offerings.

You should update your purchases journal as often as necessary to reflect the most current information. This may be daily, weekly, or monthly, depending on the type of business you run and the products and services you offer.

If you make a mistake in your purchases journal, it is important to correct it as soon as possible. This will help ensure that the journal is accurate and up-to-date. You may also want to consider using a software program or online tool to help you track your purchases. This can help eliminate the possibility of mistakes being made in the journal.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.