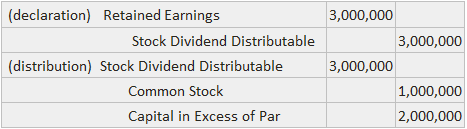

Accounting practices are not uniform concerning the actual sequence of entries made to record stock dividends. A formal procedure would recognize the dividend at the date of the declaration with the following entry for a large dividend for a par value of $1,000,000: Then, on the date of distribution, the following journal entry would be made: If a financial statement date intervenes between the declaration and distribution dates, the Stock Dividend Distributable account should be disclosed as part of Paid-In Capital. Modifying the above example slightly, consider that the dividend is classified as small and the market value of the stock is $3,000,000. In this case, the journal entries would be made under the following formal approach: As an alternative, the more expedient approach of deferring any entries until the date of distribution is often used. For the large dividend above, the following journal entry would be recorded on the distribution date: For the small dividend, the journal entry would be made as follows: If a balance sheet date intervenes between the declaration and distribution dates, the dividend can be recorded with an adjusting entry or simply disclosed supplementally.

Journal Entry Sequences for Stock Dividends FAQs

A stock dividend is a distribution of shares of a company's stock to its shareholders. The number of shares distributed is usually proportional to the number of shares that each shareholder already owns.

When a company declares a stock dividend, the par value of the shares increases by the amount of the dividend. The number of shares outstanding does not change. The cash received is recorded as a reduction of Retained Earnings.

A dividend is a liability on a company's balance sheet. It is a payment that a company owes its shareholders.

A stock dividend is a type of dividend distribution in which additional shares are distributed to shareholders, usually at no cost. A Stock Split is the division of outstanding shares into several new ones. These new shares are then traded on the same exchange at current market prices.

Like Stock Splits, stock dividends dilute the share price, but since a company's value does not depend on the money it distributes but rather on its ability to earn profits, stock dividends have no effect on a company's worth.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.