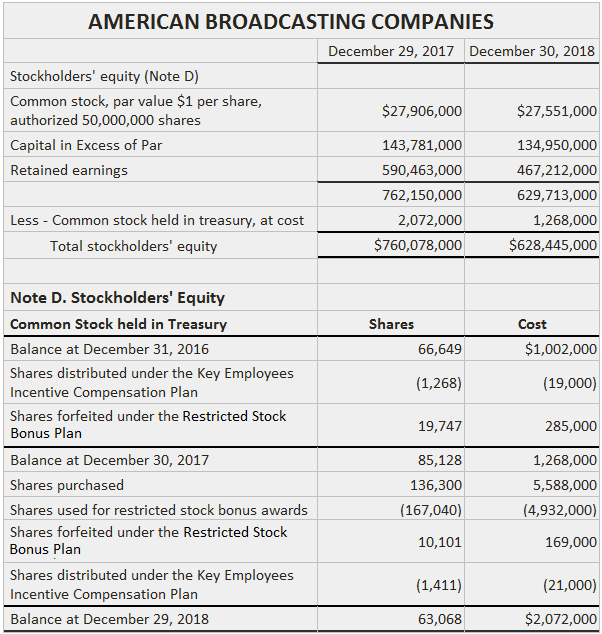

Accounting for treasury stock involves two general approaches: It is important to note that precise rules do not exist for either method. The following discussion focuses on the most straightforward types of transactions. Further, the equity accounts used are consistent with the simplified concept. That is to say, the general Additional Paid-In Capital account is used instead of more detailed accounts. Unless the amounts are especially material, this approach will produce satisfactory disclosures. If the amounts or circumstances are material, then it is unlikely that account titles will convey all the information that the statement user needs. In this case, note disclosure should be provided. GAAP allows the use of either the cost or par value methods. When management does not intend to reissue shares but also does not desire to formally retire them, it is recommended that the par value method be applied. When shares are acquired for later re-issuance or when ultimate disposition has not yet been decided, the cost method is used. Thus, a firm can use both methods if it has acquired shares for different reasons. Choosing between the methods, as well as the different ways of implementing the chosen method, rarely has a material impact on the presentation of the firm's financial position on the balance sheet. While they do produce different amounts within the subcategories of equity, the alternatives do not produce different measures of total stockholders' equity. This result should not justify haphazard or inconsistent treatment of treasury stock transactions. The following table presents a financial statement disclosure made by American Broadcasting Companies related to treasury shares.

Choosing a Method

Accounting Methods for Treasury Stock FAQs

Treasury stock method is an accounting approach in which the cost or par value of shares bought back, if any, is deducted from the additional paid-in capital account.

Treasury stock at cost method is an accounting approach by which the actual price paid for treasury shares are debited to APIC and credited to treasury stock at cost. The difference between the actual price paid and the par or stated value of treasury shares is recorded in an account known as gain or loss on purchase and sale of stock.

The amount of additional capital contributed by the shareowners in excess of the par or stated value of the shares is recorded in an account called APIC.

If treasury stock method is used, any purchase of treasury shares results in a credit to APIC and a debit to treasury stock at cost.

No, APIC account records all paid-in capital that is not considered to be part of the par or stated value of issued shares. This includes additional paid-in capital from other sources such as employees and suppliers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.