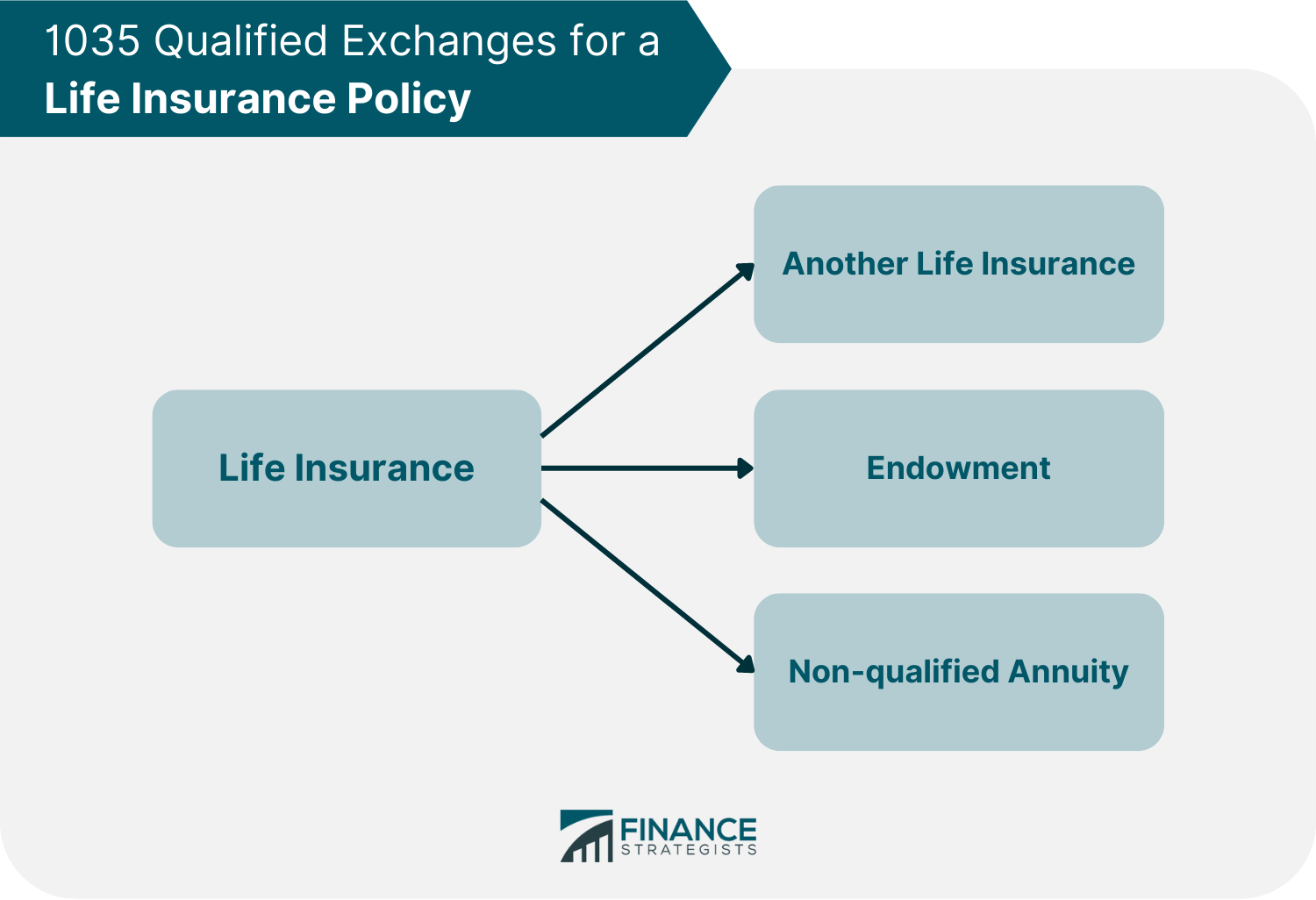

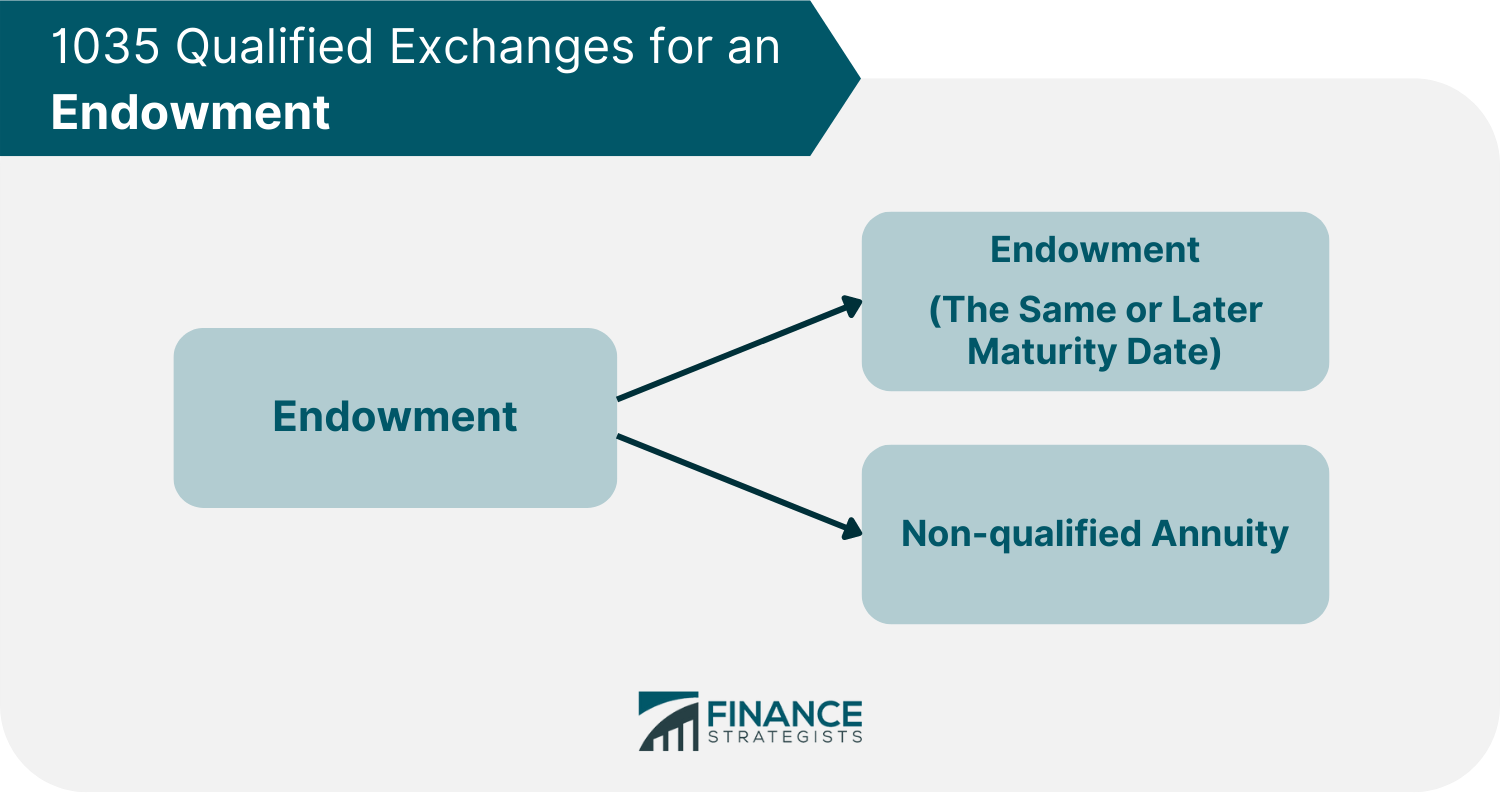

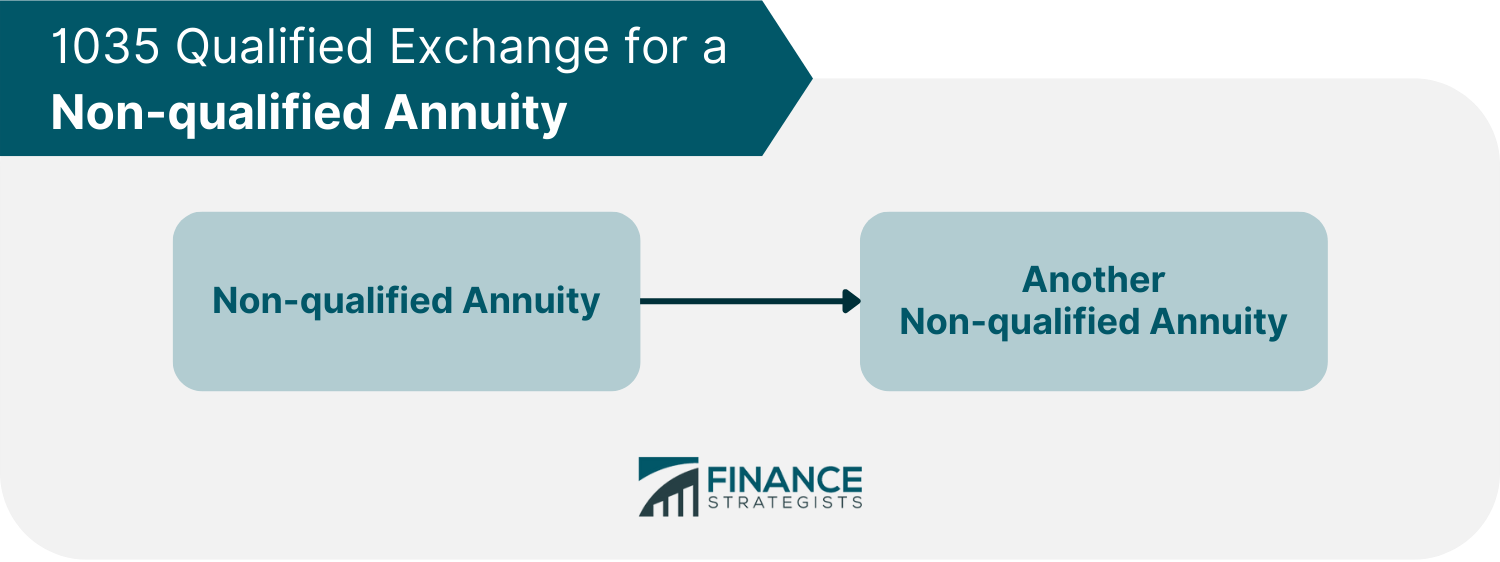

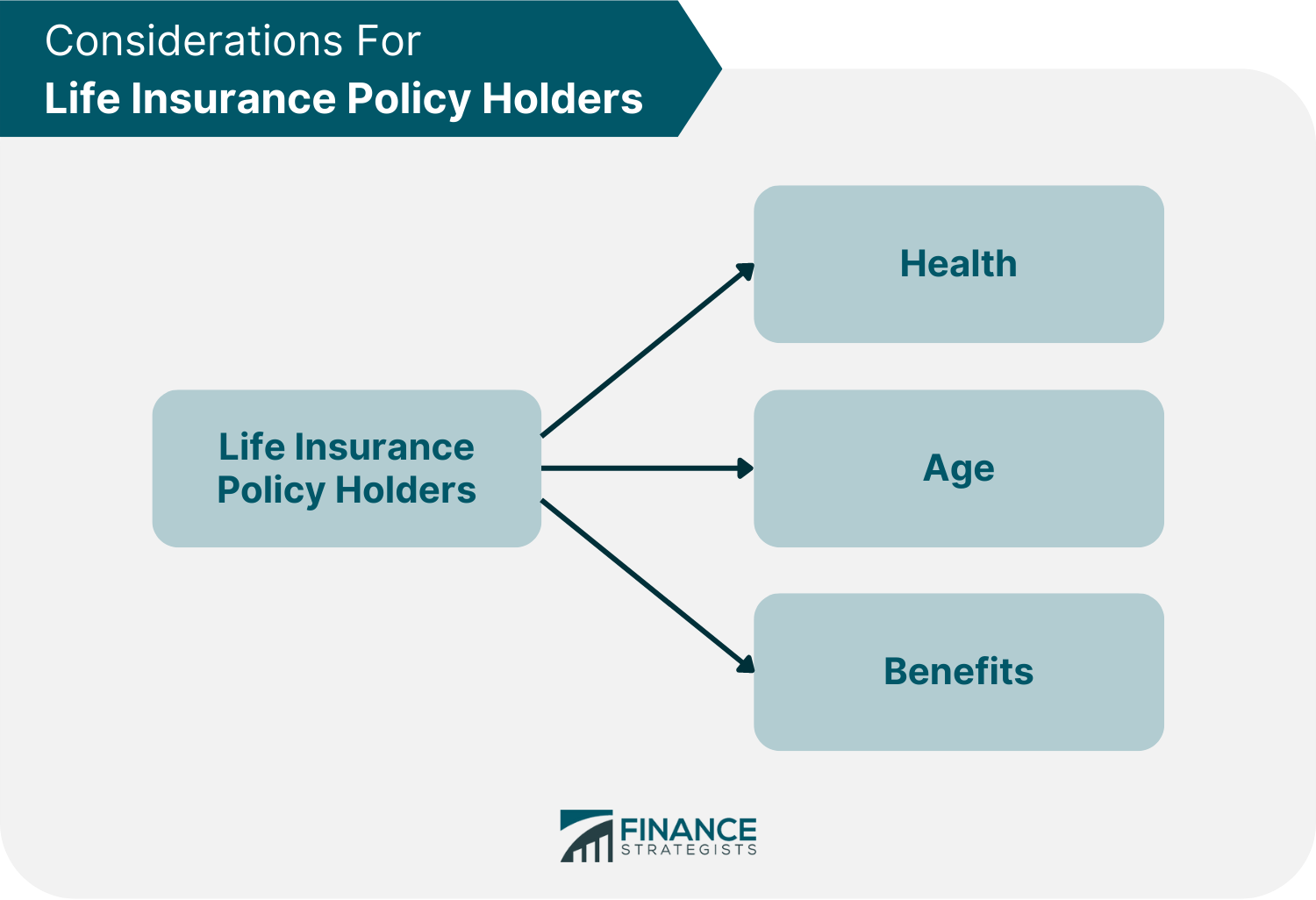

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance, endowment, or annuity policy to a new one without tax consequences. The Internal Revenue Service (IRS) permits these like-kind trades under Internal Revenue Code section 1035, where this process takes its name from. These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later. Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account. A 1035 exchange is a straightforward method for ensuring that you have the most appropriate annuity or life insurance plan for your needs. If you own an annuity or life insurance policy that you want to replace with a new one, you can apply for one with a new company. The new insurance company will communicate with the old insurance company to request funds from the old policy. You will also have to sign and submit some paperwork. Then the old insurance company will transfer the funds from your previous policy directly to the new company. Depending on the agreements outlined in the previous policy's contract, individuals may have to pay surrender charges or penalty fees when transferring from one company to another. Another option would be to perform a 1035 exchange from one product to another within the same company. With this option, individuals may be exempted from surrender charges. Regardless of whether the transfer was made within one company or to another, and even trade should be implemented. This means that the exchange can only be done with two like-kind products, such as from one insurance policy to another. This also means that individuals cannot use the 1035 exchange as a way to cash in on their old policy and pocket the money. The transfer must be passed directly from one provider to the other, with the same cost basis as the previous policy, plus gains, if any were acquired. In addition, a section 1035 exchange allows policyholders to maintain their original basis, even if there are no gains. An illustration of this is the following scenario. Anne Marie initially invested $150,000 into a non-qualified annuity and did not take out any loans or withdrawals. However, the value of her investment dropped to $100,000 due to poor performance. She was unhappy with this result and decided to transfer her funds into another annuity offered by a different company. In this case, the original contract's cost basis of $150,000 becomes the new contract's basis even though only $100,000 was moved. Any exchanges of endowments, life insurance, or annuities that do not comply with IRS regulations would not qualify for the tax benefits of a 1035 exchange. Like-Kind Exchanges That Qualify for 1035 Exchange A 1035 exchange only allows a like-kind of exchange. This means that you can exchange a life insurance policy for another life insurance policy, an endowment, or a non-qualified annuity. The code also allows exchanging one endowment for another with a maturity date not later than the original or for a non-qualified annuity. A non-qualified annuity, on the other hand, can only be exchanged with another non-qualified annuity. A replacement decision should be either economically or personally reasonable to policyholders. If they believe their current policy is not in their best interest anymore, they should consider making a 1035 exchange. There are multiple instances where swapping policies or annuity contracts might make sense. Policyholders often make an exchange when they need more life insurance coverage or when their current policy no longer fits their needs due to a change in health, family, or employment situation. An exchange might also make sense for those who are looking for contracts with lower fees. For as long as the exchange adheres to the guidelines, a policyholder can focus on finding contracts that best match their needs. Before making an exchange, a policyholder must consider the big picture and its consequences on their financial situation. When a life insurance policy owner's health has changed, or a policy has undergone changes, a 1035 exchange may be beneficial. However, the owner might be required to pay an extra premium or be denied coverage with the new policy. A policyholder should also consider their age and how that will change their needs for life insurance. If a policyholder is getting closer to retirement, they might want to trade their life insurance for an annuity that can provide them with income during retirement. Moreover, if a policyholder finds additional benefits or more attractive terms, they should consider making a 1035 exchange. For example, if the new policy offers an accelerated death benefit when the old one does not, the policyholder might want to switch. An annuity owner might consider switching to a new annuity if it is more cost-friendly and has lower fees. Freedom to make changes in the payment structure of an annuity can also be a factor when deciding whether to make a 1035 exchange. For example, an annuity holder might want to change from monthly payments to yearly payments. Another aspect to look into is finding other annuities with better potential investment returns. Changing annuities might mean the policyholder could make more money in the long run. Most importantly, a policyholder might need to consider if their existing annuity still fits their estate and retirement planning needs. A 1035 exchange can be an excellent way for individuals to upgrade their life insurance policy or annuity without paying tax burdens on the gains. However, they should do it for the right reasons, fully understanding the possible consequences of an exchange. An exchange can only be done with certain products—for example, an insurance policy with another insurance policy or an annuity with a new annuity policy. Furthermore, individuals also cannot use the 1035 exchange as a way to cash in their old policy and pocket the money. Instead, funds must be transferred directly from one provider to another. Individuals must compare the new policy or annuity with the old one to ensure that it is truly an upgrade, especially since making an exchange might change their financial situation in the short and long term. Other factors like age, health, estate planning needs, and investment potential must also be considered before deciding to do a 1035 exchange. Individuals are encouraged to only make an exchange if it is genuinely in their best interest to do so.What Is a 1035 Exchange?

How a 1035 Exchange Works

Who Uses a 1035 Exchange?

What to Consider Before Doing a 1035 Exchange

For Life Insurance Policy Holders

For Annuity Owners

The Bottom Line

1035 Exchange FAQs

A 1035 exchange permits owners of life insurance policies, endowments, and annuity contracts to exchange an old policy or contract for a new one from a different insurance provider without additional taxes.

There are several like-kind trades allowed in a 1035 exchange. For instance, life insurance policies can be exchanged for another life insurance policy, an endowment, or a non-qualified annuity. Meanwhile, endowments can only be traded for another endowment with a maturity date not later than the original or a non-qualified annuity. However, non-qualified annuities can only be exchanged with another non-qualified annuity.

It depends on the situation. Factors like age, health, estate planning needs, and investment potential must be considered when deciding to do a 1035 exchange. Individuals are only encouraged to make an exchange if it is truly the best option.

Changing endowments for a life insurance policy or another endowment with an earlier maturity date is not permitted in a 1035 exchange. Also not allowed is changing a non-qualified annuity into anything other than the same product type.

No, a change of ownership is not permitted during a 1035 Exchange. Depending on the specifics of the exchange, income tax and gift tax liabilities may be collected in this scenario.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.