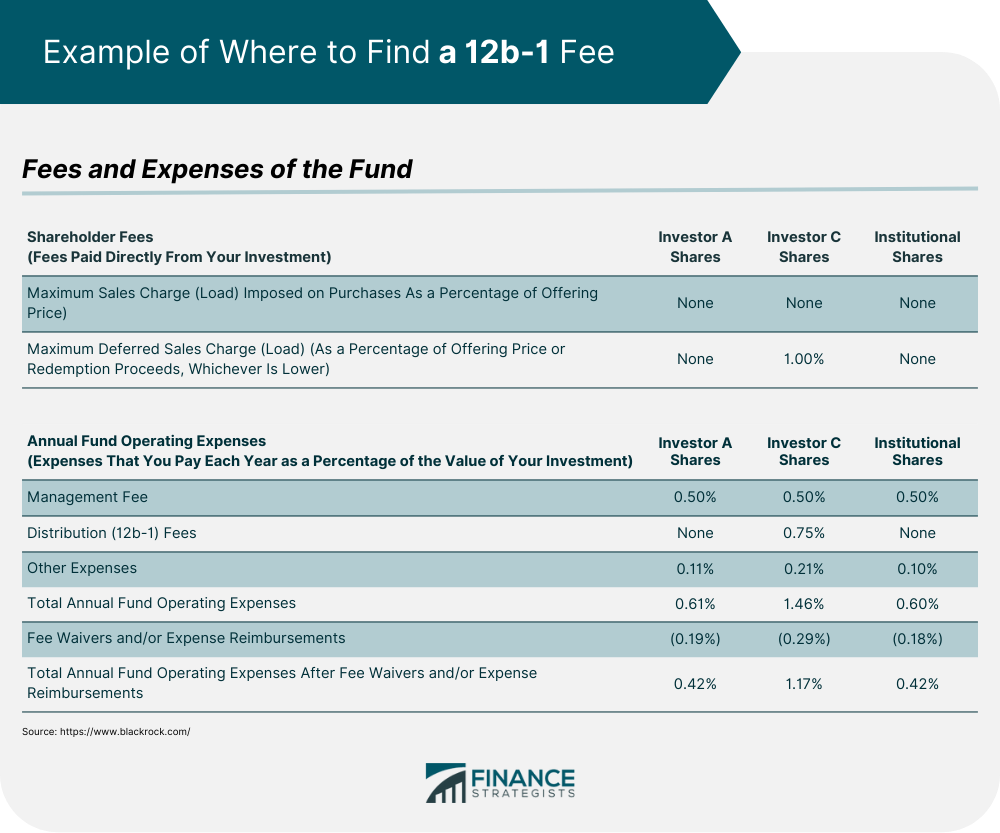

Named after Rule 12b-1 of the Securities and Exchange Commission (SEC), 12b-1 fees are additional payments charged to mutual fund investors. They cover costs related to promoting and selling the fund’s shares and are billed as part of a mutual fund's expense ratio. 12b-1 fees are typically deducted from a shareholder's investment balance annually. They do not cover the fund’s other operating expenses, such as administration or management fees. It is wise for investors to be aware of these fees because they are charged on an ongoing basis and may eat into any of the fund’s expected gains. Thus, these additional charges can be a crucial factor when deciding whether to invest in a mutual fund. 12b-1 fees can be divided into distribution fees and shareholder service fees. Distribution fees cover advertising costs and compensate those who sell the fund’s shares. Meanwhile, shareholder service fees cover the costs involved in answering investor inquiries. According to a previous SEC press release, charging 12b-1 fees was first allowed in the 1970s. Mutual funds were less popular then, and investors were losing money. These fees helped investment companies raise investors’ awareness and appreciation of mutual funds. Unfortunately, since mutual funds are more popular these days, the continued charging of 12b-1 funds has been questioned. The SEC regulates an investment company’s right to charge 12b-1 fees. It also limits the maximum percentage of net assets these companies can charge for a mutual fund’s 12b-1 fees. As previously mentioned, 12b-1 fees are composed of distribution fees and shareholder service fees. Investment companies can charge up to 0.75% of a fund’s net assets for distribution fees and 0.25% for shareholder service fees. Together, that is a maximum of 1% of net assets. For example, if a client has $100,000 worth of shares in Mutual Fund ABC at the end of 2023, they can be charged 0.75% or $750 for distribution fees and 0.25% or $250 for shareholder service fees. This makes for a total 12b-1 fee of 1% or $1,000. 12b-1 fees can be found in the prospectus, a document that outlines all the mutual fund's essential details, including the costs and risks involved. It also contains information about how the fund operates and what investments it holds. Investors can request a copy of the prospectus directly from their financial advisor or download it from the potential fund's website. Knowing how much money is going toward 12b-1 fees will help investors compare the costs associated with different mutual funds. Investors can look for the 12b-1 fee disclosure in sections entitled "Fees and Expenses" or "Fund Fees." The fee amount may vary from one fund to another, so they must read through the entire document carefully and check for a line item labeled "12b-1 fee.” Below is a sample prospectus from the investment company Blackrock. Distribution (12b-1) fees are specifically mentioned under the subheading “Annual Fund Operating Expenses” in the “Fees and Expenses of the Fund” section. With increased competition in the mutual fund market, some funds do not include 12b-1 fees. Aside from these, there are other ways to avoid 12b-1 fees, including the following: 12b-1 fees are only one component of a fund’s total expense ratio. Many mutual funds offer a low overall expense ratio, including lowering the 12b-1 fees they have to pay. Sometimes, even with 12b-1 fees, other expenses are lessened or removed altogether. This is why it is crucial to read prospectuses carefully. Exchange-Traded Funds (ETFs) do not need to employ fund managers because they focus more on tracking a specific index. Thus, ETF investors are not charged for the expense of hiring a fund manager, thereby lowering their overall expense ratio. Because ETFs have a lower expense ratio, they have become an increasingly popular alternative to mutual funds, especially for those looking to avoid these types of expenses. Dollar-cost averaging involves investing the same amount of money at regular intervals over a long period of time. By employing this strategy, investors can minimize their transaction costs and lessen the impact of 12b-1 fees on their portfolios. It also helps reduce the risk associated with investing in volatile markets since investments are spread out over an extended period. Finally, many online brokers offer low-cost services and can help investors avoid 12b-1 fees. They often provide access to a wide range of mutual funds with no minimum investment required. These brokers also typically have lower trading commissions than traditional brokers, allowing investors to save on transaction costs. In addition, they may also offer other benefits, such as research tools and educational resources. Adopted by SEC to increase investors’ awareness and appreciation of mutual funds, 12b-1 fees cover a fund’s marketing and distribution costs. Since 12b-1 fees are charged annually, they can significantly impact the performance of a mutual fund and should not be overlooked. 12b-1 fees are composed of distribution fees and shareholder service fees. Investment companies can charge up to 0.75% of a fund’s net assets for distribution fees and 0.25% for shareholder service fees. Together, that is a maximum of 1% of net assets. Potential investors can locate a fund’s 12b-1 fees in its prospectus, a document that outlines all its essential details. Before investing in any fund, it is important to read the prospectus carefully to understand the fees involved and how they affect your returns. For budget-conscious investors, there are ways to avoid 12b-1 fees, such as considering funds with low overall expense ratios, investing in alternative products like ETFs, employing dollar-cost averaging, and working with low-cost online brokers. Understanding these options helps you maximize your returns while minimizing costs. For additional information on mutual funds and 12b-1 fees, it is best to consult a qualified financial advisor.What Are 12b-1 Fees?

Purpose of 12b-1 Fees

Average Cost of 12b-1 Fees

Example of 12b-1 Fees

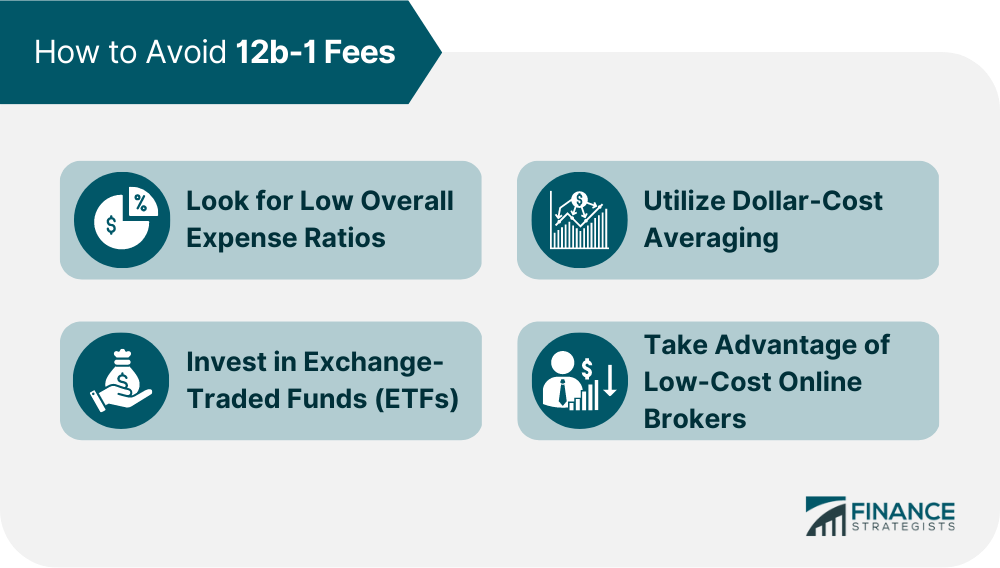

How to Avoid 12b-1 Fees

Look for Low Overall Expense Ratios

Invest in Exchange-Traded Funds (ETFs)

Utilize Dollar-Cost Averaging

Take Advantage of Low-Cost Online Brokers

The Bottom Line

12b-1 Fees FAQs

The 12b-1 fee is paid by the mutual fund's shareholders. It covers advertising costs and compensates those who sell the fund's shares. It also covers the costs involved in answering investor inquiries.

12b-1 fees are usually charged annually as a percentage of the fund's net assets. The amount of the payment can vary from fund to fund. However, the maximum amount investment companies can charge yearly is 1% of net assets.

Some mutual funds do not charge any distribution or service charges at all. Meanwhile, other mutual funds only charge small administrative or transaction costs instead of 12b-1 fees. Thus budget-conscious investors may select funds that do not carry these fees.

12b-1 fees are typically paid annually, although some mutual funds charge them quarterly. Regardless of payment structure, investment companies can only charge a maximum of 1% in net assets in 12b-1 fees.

The best way to avoid 12b-1 fees is to search for funds that do not charge a distribution or service fee. You may also invest in alternatives such as ETFs, look for low overall expense ratios, apply the dollar-cost averaging strategy or work with online brokers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.