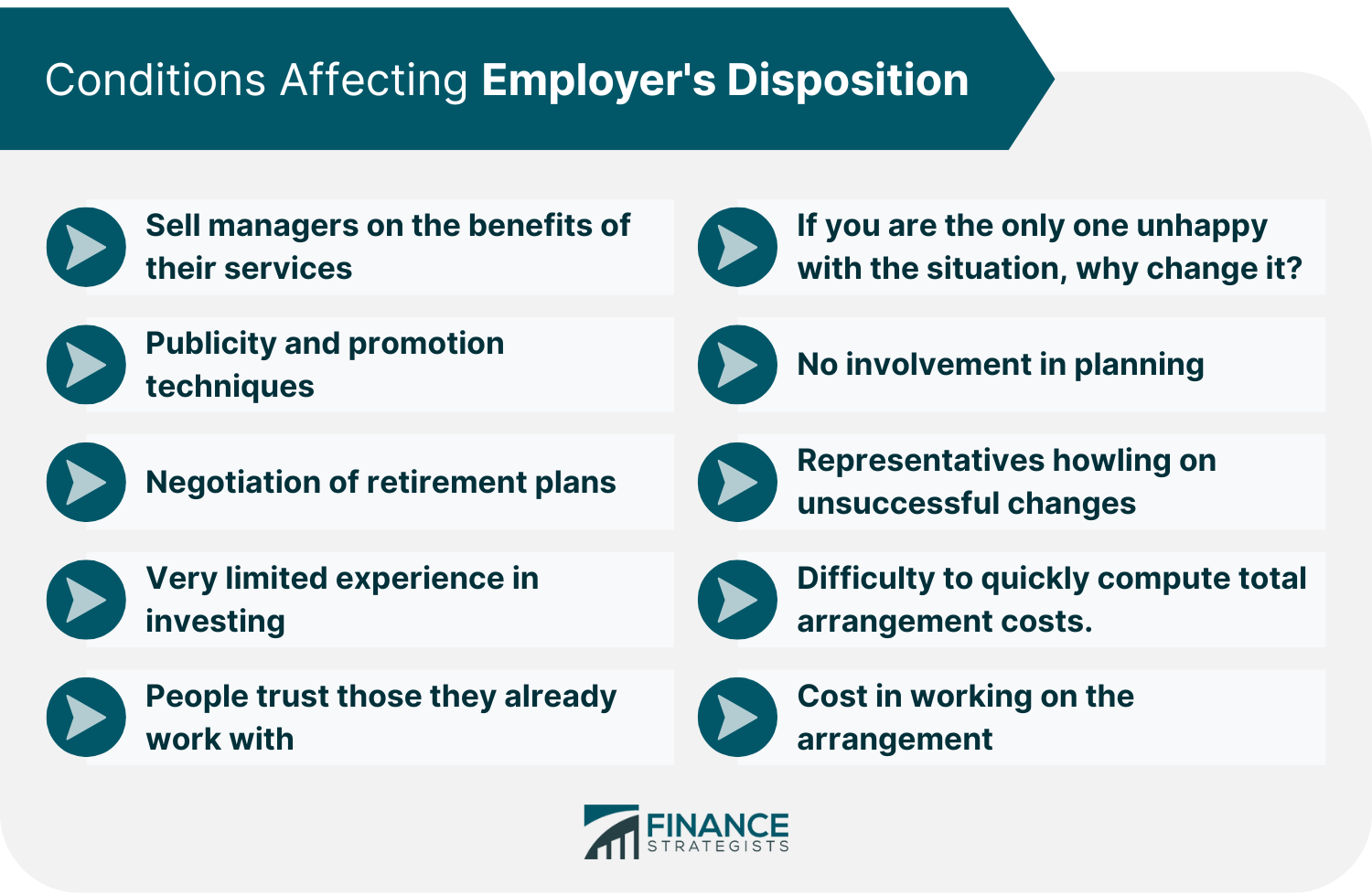

An employer 401(k) plan is a retirement savings plan that is sponsored by an employer and offered to employees. Employers may choose to make contributions to the plan on behalf of their employees (often matching a certain percentage of employee contributions), and employees can make pre-tax or after-tax contributions to the plan. Employer 401(k) plans are typically managed by a financial institution, and employees can choose how their money is invested. There are many benefits to employer 401(k) plans. Employers can use them to attract and retain talented employees, and employees can use them to save for retirement. Employer 401(k) plans often have lower fees than other types of retirement savings plans, and they may offer tax advantages. This article will provide an overview of employer 401(k) plans, including how they work and the benefits they offer. Moreover, it will help employees evaluate whether an employer 401(k) plan is right for them. Have questions about 401(k) Plans? Click here. You might already be aware, or you may have a feeling, that your plan is not working (or is really awful), but you are not sure what to do or where to begin. The first step in our approach will assist you in assessing and comparing your arrangement and current expenditures. You would then be able to take the extra steps necessary to enhance your arrangement. In any case, would it not be nice if we looked at some other thoughts before getting into specifics? The "lucky" individual at your company who is responsible for the retirement plan is called the Plan Fiduciary. In smaller organizations, this could be anyone. Give some thought to the conditions this individual (or individuals) faces. They might have little experience in investments, little interest in being a plan trustee (it is something that falls within their scope of work), and have a lot of other work to keep them busy. So use caution when discussing an evaluation of your retirement plan. If your organization has an investment committee that includes fiduciaries, it should be easy to discuss your concerns about the company's retirement plan with them. They should be working to develop a good plan for employees and willing to listen to your ideas. We suggest that you meet one of the members of the committee in an informal setting and ask them for a meeting with the rest of the committee. The goal of this meeting is for you to raise issues concerning your plan and see how they respond. Here is how we suggest conducting this with your employer. Approach the individual (or individuals) responsible for the arrangement and inquire, "When was the last time we compared our arrangement to three other choices? The goal of the inquiry is documented. If this has been done in the most recent four years, youl wil have a hard timechanging it, regardless of how terrible your current arrangement is. But do not give up yet. Simply accept that you may encounter more resistance. If your manager has already conducted an investigation and can produce the results, ask to review the data to understand why they chose the current supplier and plan. The language below is what we recommend you use when talking to your employer. I am concerned that our current arrangement may not be as aggressive as it could be. I have done some research and found that smaller companies are more likely to have pointless expenses in their budget. However, there are some specific steps we can take to further develop our arrangement. Since we have not done a serious audit of the arrangement in quite a while, I want to talk about this issue and see if others feel the same way. Can we investigate this? I would be eager to help with, or even lead, the process. Obviously, expect some opposition on this. However, you might also be shocked to discover that you may get assistance. Your arrangement support may be grateful that a worker with a well-studied contract has contacted and requested assistance. When you bring up this issue, do not be nervous. You do not need a PowerPoint presentation or a three-ring binder full of statistics. Giving your employer concise and relevant information will aid them in comprehending the problems that most small managers face. Forward them links to reports or articles that explain how many plans are badly designed for smaller businesses. They may also want to view this Frontline Documentary or this Sensible Investing TV documentary. Does your manager's retirement plan reflect what you want to do in the future? This is why you and your colleagues contribute money to the plan. Although it is a valuable perk, many smaller employers never take the time to shop around for a better deal on their retirement plans. They remain with the same provider for years, even decades, without ever considering if there might be a better option out there. An arrangement survey is a conversation with the existing supplier, which might be a specialist, protection specialist, enlisted speculation counselor, or advisor to the agreement. The discussion may simply concern how the current deal "is going," as well as how it "looks at different plans." This approach isn't enough. Again, it might be stating the obvious to say that your boss may not want to investigate this further. However, if you come armed with research or information to back up your argument and let them know that you can help in the process, they may be more inclined to get on board – after all, they have money invested in the plan too. Be mindful of the following conditions which may affect your employer's disposition: As you discuss this with your boss, your main objective should be to convince them to agree on these four objectives: In the next section, we will cover the importance of these four objectives in more detail. Additionally, understanding how your plan works will give you the confidence to discuss these topics with your boss. You will make the most progress when you convince your plan trustees that these objectives are legitimate and will improve upon the current state of things. If they agree with you that it is beneficial to include these strategies in your retirement plan, they are admitting that its present structure is lacking and that there is room for improvement. Then, it is simply a process of choosing a better arrangement – which we will break down for you step by step. Take a look at the Retirement Gamble and Sensible Investing TV. You are undoubtedly enrolled in a 401(k) plan. As a result, we will refer to 401ks throughout the article even though there are numerous different retirement plans used by employers. These include 403b plans, 457 plans, SimpleIRAs, Simple 401ks, 401a plans, SEPs, SARSEPs, and Defined Benefit Plans. Additionally, there is a significant variation in plan complexity as well as certain types of cross testing that may be utilized. While there are several alternatives for businesses, these distinctions do not alter the key messages of this article; therefore they will not be discussed further. However, it is important to keep in mind that not every issue related to 401k plans applies to other types of arrangements. For example, many plans are not subject to ERISA rules, which oversee almost all 401k Plans. ERISA is the 40-year-old law governing numerous retirement plans, among other things . Some retirement plans, such as Simple IRA's, SEP IRA's, certain 403b and 457 plans, and some congregation or government plans, are not subject to ERISA. In general, these types of pans will have similar high fees and incomprehensible fine print as 401k Plans. (This is even more absurd when you consider that they have less regulatory oversight.) The board of your 401(k) has several component parts. We will look at every angle and suggest a plan for you based on that. They are as follows: Because numerous trading firms, record keepers, counsels, and specialist/sellers promote their products mutually (or sometimes together), it might appear to be complicated. How much more for the employees - as well as the trustee. The money you (and your boss) contribute is kept in your arrangement's venture choices. You decide where to contribute as you set aside money in your manager-based retirement plan, and ideally get a match or other sort of business subsidy. There are a variety of investment alternatives available, ranging from conservative accounts like a Money Market Fund or a Stable Value Fund (which promises to keep its value and not lose it), to more daring investments such as international stock funds. There may also be a self-managed money market fund (for the DIY financial backer who has to worry about their own speculations) or some company stock. Company A's Safe Harbor 401(k) Plan had 12 participants and $2.2 million in assets before making changes to the new plan. Total cost for variable investments was approximately $30,000 with an insurance contract that used mostly actively managed funds. Fees averaged 1.9% of assets and were paid separately from TPA services. The new plan's total cost is $6,700. The advisory and record-keeping fees are now flat charges, totaling around $4,900. With Vanguard funds in the mix, their total fund fees come to $1,800. This employer paid for employees' advisory and record keeper charges upfront—so the only costs workers have are those associated with Vanguard funds. By switching to this new plan, employees saw a more than 90% reduction in overall costs! The average 401k plan is composed mostly of shared assets, which are case funds that store stocks and/or bonds, or a combination of the two. They are viewed as proper choices for retirement plans, which are by and large long haul in nature, since they furnish opportunity for development with decreased risk because of the enhancement you get by claiming a few stocks or securities in each asset. Financial backers will in any case be dependent upon different types of hazard in common assets, however they are believed to be much safer than any stock or security that you could buy individually. Mutual charges a fee for their executives' administrations. This charge is known as the Expense Ratio and covers a monthly fee, which is updated on a daily basis. You should be able to view the cost for each asset in your arrangement. There can be many different fees charged by asset to fund. Index assets from an organization like Vanguard have low expenses, as do Exchange Traded Funds (ETFs) which your arrangement may also suggest. A common issue with retirement plans is that the fees to manage the plan are mixed in with the mutual fund or investment fees. When these charges are bundled together, it can be hard to tell how much each provider costs. The cost of the retirement plans can make up a significant percentage of what the participants pay in total. When you join most plans, you can choose from a range of sizes, anywhere from 8 or 9 on the lower end to 50 or 60 for large set-ups. You would typically select your investments when first joining, but you can change them without charge at any time. There may be limits placed on how often you are allowed to exchange though without issue in manager-based plans. Many plans offer a default option for employees who do no want to pick their own assets, or for employees who are automatically enrolled by their employer. Many plans carefully use Target Date Funds - which get slowly more cautious as employees approach what might be their normal retirement date - as the default election. Model or oversaw portfolios are another type of portfolio that some insurance plans may provide. They are generally comparative, although they might differ from one arrangement to the next. The benefit of these portfolios is that the financial backer simply chooses a model based on their company's approach. For instance, you would apply the Aggressive Model if you were a powerful financial backer while you would use the Conservative Model if you are a moderate financial backer. The arrangement's warning company will distribute the member's cash among different common assets based on the model portfolio's goal. The age at which the member will resign also affects how a plan can provide model portfolios. In light of the financial supporters' present age, the portfolio will be figured out how to provide a suitable resource assignment as the member approaches their usual retirement date. These are also known as Target Date Funds. Over time, how these model portfolios are managed will change from company to company. Some portfolios may rebalance, redistribute, or alter their holdings on a regular basis, such as every month or every three months. The idea is that the company managing these portfolios provides some incentive to the executives through either increased returns, decreased risk, or a combination of these benefits. Generally speaking, but not always, these types of portfolios are more expensive. These additional fees occasionally can be substantial. The elimination of income sharing is one of the main improvements your arrangement can make. This is the first of the four major goals for your plan. Income sharing is when an expenditure is taken from one source, usually the common asset or speculation, and given to another provider of administration services, such as a record manager or counsel. Having income sharing in retirement plans is like having a general contractor on a homebuilding or renovation project who gathers payments and distributes them to subcontractors. We believe this is potentially the worst feature of retirement plans and should be eliminated. There may be no protection against income sharing at this time. We are past the point when revenue sharing made sense because of technological advancements. One strategy to make income sharing work is by using the most costly offer classes for assets accessible in retirement plans. Most venture companies offer diverse offer classes for each asset, and usually, each class has a different cost proportion. In other words, a single asset can be made available to investors at completely different prices. Not to mention, the scope of expenses can be overwhelming. For example, we have included an asset that is very well-known in many retirement plans: the American Funds Growth Fund of America. As you can see, there is almost a full percentage difference in the expense ratio of this fund from the least expensive share class, R6 at 0.49%, to the most expensive share class, R1 at 1.44%. Make it a goal of your plan that each asset in your setup would use the cheapest share class for which you can qualify. Even the smallest employers can access these lower costs shares through most recordkeepers. Other investment products or fees you should exclude from your plan are variable annuities, commissions, broker/dealer charges, and marketing dollars. Many trading companies pay consultants, advisors, or conveyance companies to help them promote their bets. The consultant's or dealer's advertising expenses are partially funded by a venture firm they recommend. This is a common practice in the industry that undoubtedly affects how financial advisors recommend assets to their clients. Providers that receive compensation from investment firms for marketing support are common, but that doesn't make it right. You should avoid working with any provider that receives this type of compensation and always get this agreement in writing. The second key goal for your plan is to use a lineup of primarily index funds from Vanguard. For example, we prescribe the following arrangement to our customers. We suggest Vanguard because their expenses have been among the least in the business for many years, they are seldom guilty of promoting hot assets or investment ideas. Additionally, Vanguard is owned by its investors (unusual in the business), and they have never participated in income sharing. It is recommended that you use a minimal expense record asset setup, with delegate assets in each resource class, along with a steady value asset, and be done with it. This is the right thing to do for your organization, plan, and employees. However, before we continue, we must address a typical problem that affects many plans. Most managers make an effort to identify assets who perform better than list reserves. Additionally, they acknowledge that doing this is the right thing to do for their arrangement and their representatives. Many firms that assist retirement plans will often tell you that they only want what's best for you by finding the funds that outperform other records. By using their self-proclaimed “restrictive” and “powerful” screening process, they claim to always have your organization at the top of their list. They also state that these Funds are constantly monitored and, if ever replaced with new ones, it is because those newer options are better in some way. However, do not be fooled. The most typical technique for choosing the finest assets, checking them, and then replacing them later is time-consuming and ineffective. Create a portfolio of low-cost index funds, with representative funds in each asset class, as well as a stable value fund, and be done with it; this is the right thing to do for your organization, plan, and employees. Investors are often uneasy about being examined, but there is a large body of evidence that suggests that actively managed funds with higher fees have difficulty outperforming cheaper index funds over the long term. If you want a company that will give you the resources to succeed, you need to research their past and see how they have performed over time. Having an noteworthy conversation is not enough. Every consultant that uses this methodology should be able to show you how their additional expenses have benefited their customers in the long term. They should also be able to show you each of their suggestions, both successful and unsuccessful ones. Obviously, we outperformed effectively managed assets. However, if you decide to keep them for your asset arrangement, we recommend that you search for ones with cost ratios less than 0.55 percent. Charges matter, and minimal expense effectively managed reserves have a better chance of outperforming minimal expense list assets over time. Regardless of whether you use all record reserves or a mix of dynamic and list, your arrangement should provide a display (perhaps 15 to 25) of the least offer classes available for each asset. You should also have a consistent worth fund. We'd also urge you to check out whether oversaw or model portfolios are available for your plan. Our opinion is that most financial supporters will be fine with Vanguard's Target Date or Life Strategy Funds, which provide considerably more expanded and low-cost resource options covering a broad range of risk levels. If you are going to use oversaw or model portfolios, we suggest that the board charge be no more than 0.25 percent. Our suggested approach offers more trustee assurance for plan supports and the chance for better returns over time for the representatives, which is an incredible combination. The way your arrangement works is through record keeping as well as Third Party Administration (TPA). The TPA is the person who handles all of the arrangement's administrative tasks. They handle dispersions and finance, manage the site, finish yearly filings as needed (when required), test the agreement, create an arrangement archive, issue proclamations, validate support, and give other exchange or mechanical assistance sort of capacity for the arrangement. As a result, they are the machine that drives your employer-based retirement plan. There are numerous record managers that operate independently. They may also provide some of their expertise to other trading firms that need assistance with certain aspects of record keeping. Usually, a record attendant will use the services of another firm for trust or custodial services. It is possible that, in some plans, there could be a record keeper who completes some of the tasks required by the plan and another party to administer other aspects of the plan. Some employers- especially smaller employers- may hire an outside firm to file their Form 5500 or use the services of a CPA. Many plans do not require all of a record manager's services, yet they may need some of them. IRA managers that provide SEP or Simple IRA accounts have less stringent record keeping requirements. Also, other ERISA-exempt plans, such as certain church plans, government plans, or 403b plans in which only the workers contribute, or 457 Deferred Compensation arrangements in which the employer makes payments, are not required to have each of the administrative services of a record attendant or TPA firm. If you use one of these options, this is excellent since it indicates that the overall costs of your arrangement should be lower. Set up your agreement so that you have a free record manager that charges on an equivalent expenses basis. Suppliers will change how they compute their expenses, but the majority will bill their services after adding all costs together. You do not need your record manager to be a venture supplier or a caution firm. An unbundled administration solution is what this suggested method is called. If you choose to pay on a flat fee basis, you will avoid paying your record keeper (and advisor) on a percentage of assets basis. This is the third of the four major goals for your plan. Most independent record keepers usually price their services per eligible employee or per participant. They could also have charges for other service expenses, like a Plan Document, completing the Form 5500, and so forth. The point is that you should be able to pay for this kind of work with one flat fee instead of racking up miles on your credit card every time something needs fixing. Here is an example: if there are 55 participants in total, annual costs (with all services provided by said record keeper) might come out to $3,000 - $4,000 dollars give or take a few bucks here and there. The annual level charge for your account will be based on the number of members (or employees eligible for the plan). However, it should not change dramatically from year to year. For example, if your plan assets are $2 million and your record keeper charges $3,500 for their services, this would come out to 0.175%. If your assets grow to $2.5 million but there is no real change in the number of members, you will still pay approximately the same amount -$3,500 On the other hand, if your plan is paying for recordkeeping services in a packaged way, and the expense was, for example, 0.30% of plan assets (as in our previous model), the expenses would increase from $6,000 to $7,500 even though there has been no change in how much work is required by the recordkeeper. Therefore flat fees are a particularly effective way of reducing plan costs. If your agreement is paying consistent expenses, how are the fees truly assessed to accounts? It is really simple. We should employ the method outlined above - a plan with $2 million in assets and a yearly record custodian charge of $3,500. This fee amounts to 0.175% of plan resources each year. Subsequently, every member’s quarterly charge would be 0.04375%. The record guardian ascertains your charge by duplicating the quarterly rate by your arrangement balance toward the finish of the quarter (it’s conceivable it very well may be determined day by day). Assuming your arrangement surplus was $50,000, your record saving charges for that particular quarter would have been calculated to be $21.87. These numbers will shift as time progresses and resources begin to run low or become too large in size; this also changes how much money is being charged per save. In a pure cost climate, however, a few plans may be defenseless. These are uncommon because there are fewer members and adequate equilibrium accounts. If one individual leaves the firm and takes their assets with them, the excess members should contribute more to the cost of the arrangement. Assuming this happens, it will just have an impact on the members for a brief period of time. As a rule, this won't have an impact on most plans, nor is it reason enough to pay for recordkeeping as a measure of assets. We would also recommend that you choose a record manager who accepts TPA work. These should not be different firms. Most skilled free record attendants can also provide full TPA administrations. The fiduciary for your retirement plan, and it may be multiple people, is responsible for ensuring that your goal is running correctly, is reasonably priced, offers good investment options for the participants, etc. The Department of Labor (DOL) and the Internal Revenue Service (IRS) guides employers on how their plans should operate. This would include forms that need to be filed, documents that need to be kept, and procedures that should be followed - basically, the rules under which your plan operates. As referenced before, as a rule, your arrangement is dependent upon a law called ERISA. The DOL is the government office that gives a significant part of the direction to the business on how retirement plans ought to work. The IRS additionally shares a portion of the obligation regarding this region. It’s anything but a crazy situation. Your boss has rules and revealing necessities to keep in the clear, giving a decent arrangement and aiding the employees. “A good fiduciary, first and foremost, protects the interests of the participants. The fiduciary must act in a prudent manner at all times.” As a fiduciary, your top priority is always the interests of the plan participants. This means acting reasonably and consistently at all times. Given the complexity of plan management, most employers rely on professionals for some level of assistance even for simplified plans. While a few businesses feel confident enough to handle everything themselves, most prefer not to. Two ERISA codes allude to various degrees of guardian obligation regarding your plan. A 3(21) trustee has discretionary authority over the plan or its assets and also has some liability for decisions on plan administration. In practice, a firm acting as a 3(21) would typically make investment decisions and guide the plan sponsor on fiduciary matters. On the other hand, a 3(38) guardian has full discretionary authority over the plan's investments. This means that the 3(38) is responsible for all investment decisions and faces unlimited liability for those decisions. As a result, only experienced and well-capitalized investment managers should act as a 3(38). The 3(38) fundamentally chooses and screens the venture choices for the plan. proposals are sent to a business on the speculation of contributions in the arrangement. There are several key reasons why a manager might choose to employ a warning firm as their 3(21) as well as 3(38) fiduciaries. First and foremost, doing so can provide significant peace of mind knowing that the management team's interests are being protected. Additionally, employing a professional warning firm can also help to ensure compliance with regulatory requirements and safeguard against any potential legal liability. When it comes to investing, there are a lot of different options out there. And with so many options, it can be tough to figure out which route is best for your company. This is where the consultants, advisors, lawyers, etc., come in. The challenge for your employer is to determine who they need to hire to get the job done without getting overcharged or purchasing unnecessary services. Plan rearrangements ought to diminish the expense for warning services. The record manager, as well as TPA, will give a business some help with meeting their trustee commitments. They ought to give the majority of the essential documentation for the arrangement. These are the Plan Document, the Summary Plan Description, and Annual Notices. In addition, it is likely that they will “test” the plan to make sure employees and the employer do not over contribute and that all eligible employees receive the money they are entitled to. As a rule, a record manager's work is additionally coordinated with a firm that gives "Trust Services." Some record guardians will give trust administrations. The most effective way to depict the job of the trust organization is that it guarantees that the cash is taken care of appropriately. Most trust organizations charge for their administrations as a level of resources. Anyway we would say, it ought to be under 0.10%. Trust administrations can incorporate investment funds and checking accounts, just as different types of ventures. Another part of a plan the executives for a guardian is the thing that we call plan structure. This is deciding the sort of plan that will turn out best for your association (401k, or 403b, Safe Harbor plan, etc.) and establishing the rules for your plan, such as employee eligibility, the funding level, schedule, availability of loans and withdrawals, vesting schedules, in-service withdrawals, and auto-enrollment and/or auto-escalation. At last, these choices are the obligation of the business although they might look for direction from a warning firm. You can do a few things to help make your arrangement more effective and reduce the amount of work for your trustees. One is to structure your arrangement so that it is easy to understand and follow. This will help trustees keep track of what is happening and ensure they are doing their jobs correctly. It will also help employees know what their options are and how to best utilize them. Another way to reduce trustee work is to have a good communication plan. This means that you should have a system for regularly communicating with trustees and providing them with updates on the status of the plan. We would urge your association to have an Investment Plan Committee. This gathering meets intermittently to ensure the arrangement is working accurately. The entire archive utilized by the speculation Committee is the IPS. We would likewise urge you to recruit a warning firm as both a 3(21) co-trustee that will share your responsibilities regarding a general arrangement with the executives and a 3(38) Investment Manager that will assume liability for your asset setup. Regardless of whether you make these strides, it is hard to take out your danger since you bear liability regarding picking capable counsel. Restricting your risk, however, is brilliant and very feasible. If you have an IPS in place, it can help reduce the need for frequent meetings. Your objectives for the meeting should be to ensure that your arrangement is securing the interests of the members, your fellow workers, and compliance with the IPS. You can review topics such as whether or not the record keeper is doing their work, the seriousness of plan expenses, organizational changes that could affect the retirement plan, and industry trends. That may affect the arrangement and any arrangement changes that may expand interest or plan understanding. You can likewise examine the direction and schooling for staff and how it may be improved. As a small business owner, you may feel that you need to have your investment committee meet more often than once a year. However, we would recommend that you stick to meeting once a year, unless something comes up that warrants more frequent meetings. One of the most effective ways to work on your arrangement and trustee obligation is to go through a line of minimal expense record and Target Date Funds from Vanguard. You can compose your Investment Policy Statement with the goal that it says the accompanying: “Our objective is for our workers to acquire near market based returns less any arrangement charges they need to pay.” This will help you keep away from potential missteps, for example, picking singular stocks or putting excessively in a specific venture. There are several reasons why index funds are a great choice for many investors. There are a few reasons why this approach is especially savvy, and could potentially lead to higher returns for investors. In order to ensure that retirement plans are able to outperform similar private funds, it is important for there to be an effective oversight mechanism in place. Unfortunately, this is not always the case, and as a result some retirement plans can end up lagging behind their private counterparts. One of the biggest issues facing retirement plans is the fact that many of them are run by employees who act as trustees for other workers' investments. This can lead to problems down the line, as these individuals may not have the necessary expertise to make sound investment decisions. Here are a few circumstances where it may be permissible to advance a supplier. For example, if the advancement is made in good faith and there is no actual or potential conflict of interest. However, as a trustee, you must always be aware of your fiduciary duties and act in the trust's best interests. If there is any doubt as to whether advancement is in the trust's best interests, you should seek professional advice. Bid your arrangement more much of the time than once like clockwork. Assuming you archive your bid cycle and have helpful yearly Investment Committee gatherings, an audit each four to five years is fine for a more modest employer. Arrangement structure is something that a smaller employer should keep in mind when setting up a benefits plan. The goal should be to create a plan that is easy to administer. This can be accomplished by working with a benefits firm that has experience in this area. However, it is important not to spend too much time on this task. The arrangement should not be overly complicated. We have more information on our experience with this here. Plans are important for giving employees a clear understanding of their roles and responsibilities. By taking the time to develop a plan, representatives can better comprehend their part in the organization and be more prepared for their future. Additionally, having a plan in place can help reduce stress and anxiety about the unknown. Essentially not sure about their venture choices for their arrangement and battle to make monetary arrangements for what’s to come. They have a threatened outlook on enlistment interaction and aren’t sure about the amount to contribute and where to contribute. Great direction can be a significant part of your arrangement and help the workers utilize the retirement plan as viably as possible. There are a few key reasons why we believe that direction is important in business-based retirement plans. This is the fourth of our four Key goals for your plan. A good deal of attention is given to the importance of providing excellent guidance regarding employee development. This usually consists of numerous brief, personal talks with your workers. Instructional sessions that last anything from 5 to 30 minutes are typically included, except in the case of retirement or financial planning meetings, which can go as long as 1 hour. Given their brevity, the expense for assistance should not be prohibitively high. Here are some ideas for offering excellent advice to your employees: Personal Assistance at The Time of Enrollment Advisor Availability Personal Check-in Meetings (set at regular intervals) Financial Planning for Employees Personal Consultation When Employees Depart Seminars Web-based Educational or Planning Tools Let's discuss this critical problem before we go through our procedure to improve your plan. It's a horrible plan conversion that no one wants to deal with. Many organizations believe changing from one service supplier to another is a time-consuming and unpleasant process that could fail. What's more, they will be held responsible for it. There are a few reasons why some people may not want to consider a new software conversion. They may have had other conversions that did not go well, or they have heard from colleagues or peers at other firms about nightmare conversions, or they don’t like the idea of taking on any additional projects that might be a risk. Whatever their thinking, specific individuals probably shouldn’t rule out new choices just because they would rather not deal with the conversion. We understand businesses' concerns when considering changing their retirement plans; however, these complaints should not dissuade anyone. This change will help improve the working conditions for our employees so they can have a better future. Sometimes, the improvement may be slight, but it could be significant in other cases. It's worth going through some hardships along the way. There are, however, some potential pitfalls to be aware of. One is that people generally don't like change, even when it's for the better. It can be disruptive and stressful, and it can take time to get used to new procedures and systems. That's why it's so important to communicate the reasons for the change clearly and concisely and to provide employees with the training and support they need to make the transition smooth. There will always be a few complainers who will find something to protest about, regardless of the advantages. Don't let them dissuade you. We believe that smaller organizations should be proud of their efforts to further develop their benefits and can confidently speak about how they did this and why it is really great for employees. An uneven change can feel like a daunting obstacle, but it's essential to address it head-on rather than trying to ignore or work around it. Every organization faces the potential for an uneven change at some point, but that shouldn't be a reason to wait or hesitate. You'll make your decision based on other factors, so don't let this weak excuse derail your efforts to develop your advantage further. Don't let the fear of transition prevent you from considering all of your options. “We believe smaller organizations should be proud of their efforts to improve their benefit and can communicate with confidence how they did this and why it is good for the employees.”. Now that you have a better understanding of how to set goals and what goes into a good action plan, let's get started on making some improvements. If you're looking for a way to streamline the request for proposal (RFP) process, then you should consider using PlanVision's Automated RFP System. With this system, you can fill out an online form with your RFP requirements, and then our software will generate a customized RFP document for you. This not only saves you time but also ensures that all the necessary information is included in your RFP. This interaction will assist you with saving time and a large number of dollars you may spend for a specialist or counsel. We have given all the guidance and devices you want to take care of business. Since you don’t have the resources of a larger organization to devote to projects such as this, it has to be straightforward and simple! We know it might not be easy (which is different than simple), but it doesn’t have to be so difficult that you don’t get it done. Assuming that you accomplish the four key objectives we have illustrated previously, you can have an awesome arrangement. However, if you only achieve two or three of them, that could still be a huge improvement in your plan. It's best if three people are involved in the process. You should split the tasks and share your progress. Two people can do most of the research and the third person can attend the presentations and assessment conversations. However, your approach will ultimately be determined by your organizational factors. We have provided an estimate of how much time each step of the process will take from start to finish. “Smaller firms may be able to cut their costs by 50% to 75%,and we have seen some reduce theirs by around 85%! While it is typical for the primary goal of a meeting to be cost reduction, this isn't always the employer's motive. In some cases, the review exists to solve another problem with the current plan that could include anything from poorly managed administration to a lack of employee understanding about available options. During these reviews, employers often realize they're paying too much and can save their employees money by switching to more competitive vendors. When choosing a vendor for your business, there are many factors to consider. One of the most important objectives is to find a colleague with similar or comparable qualities in providing support, guidance, and an overall approach to investments and risk. We help you evaluate how each vendor will work with you and your staff so you can determine if they are the best overall choice for your arrangement and the lowest cost option. This project will take an estimated 3weeks to complete. Yes, it should only be on one page. Many businesses, big and small, think this is not easy to do. However, we are providing you with a one-page fee sheet that you can use to collect the necessary information for your business. Try not to think you must obtain all this information - your arrangement won't include them. Small businesses typically use a few types of financial statements. The balance sheet is one of the most important, as it provides a snapshot of the company's assets and liabilities at a given moment. The income statement shows how much revenue the company has generated over a period of time, and the cash flow statement tracks the movement of cash in and out of business. There are two vital expense measurements for your arrangement. These will be significant targets. The first is the complete expenses paid. This is an annualized number. For instance, your absolute arrangement expenses may be $15,000. If your total costs are $15,000 and your arrangement resources are $1 million, then the cost of a level of resources is 1.5%. You must also consider whether or not the members or the company pays the charges. A few plans combine all the fees into one big sum that employees from their bank accounts later pay. Packaging may make it more difficult to sort out your expenses unless they are highly exposed. To start, you gather the total plan assets at a specific time. For example, what were the plan assets as of December 31, 2014, or June 30, 2014? You can find your latest year-end balance on Form 5500--this doesn't include any personal member data. Alternatively, you could ask your service provider for a report that provides information about every member and their account balance. This latter option is probably best if you're hoping to sell because potential buyers will want to know how many current and previous participants there are. Planned sellers will probably need to know the absolute number of current and previous participants. To get an accurate estimate of your arrangement expenses, start by looking at the cost disclosure. This is a document that you should request from your employer or service provider. The cost disclosure will list all of the fees associated with your arrangement, as well as any other charges that may apply. It is likely accessible on the site where you access your record. In any case, many of these are difficult to sort out and may give instances of conventional costs that are not explicit to your arrangement. Assuming you can’t decide your expenses from the charge divulgence, your subsequent stage is to converse with somebody at your arrangement record manager, consultant, merchant/seller, or whoever else may deal with your arrangement. Please clarify that you are using a one-page sheet to figure out the total costs of our arrangement. If they refer you back to the Fee Disclosure, say, "I need some help. We're your customer, so shouldn't you be able to guide us through this process quickly?" If they don't assist, then call someone else. Make a concerted effort to contact 4 distinct people. Start a log and note the hour of each call, including who you spoke with and how they responded (don't record the conversations). If you're only getting nonsense from your suppliers, it's time to reevaluate their charges. They should be reasonably compensated for their work, but you shouldn't have any trouble understanding their fees. Additionally, confirm any transactional fees such as shipping charges so you know what they are with your current provider and can compare them to other firms' transaction fees. By being an informed consumer, you can make the best decision for your business. It is important to realize that there are two sorts of plans in which reducing expenses may be difficult. It is by no means impossible, but it can be challenging. The first kind of plans with multiple caretakers. This will complicate your situation if one or more of your arrangements' resources will not move to your new caretaker, for example, if you have a protection contract with moving restrictions. Second, plans with numerous members and low equilibrium records may believe it is challenging to decrease costs. With your finished expense sheet, you presently realize the amount you are paying and how much every supplier is made up for their work. This project will take an estimated 1 week to complete. In addition to the four main goals we discussed earlier, we will now review the specific objectives for developing your plan. When you're planning a new arrangement, there are a few things you'll need to keep in mind. What do you want out of your new arrangement? How might it be enhanced? What are the prospects for this strategy? What's the significance of this data? These may be complex tasks for a group that isn't sure what options exist. That's why it's important to take some time to really think about what you need and what would work best for your situation. With careful planning and consideration, you can find the perfect arrangement for your needs. We've given you six classes to help you identify the overall layouts of plan the board. Also, keeping these classifications in mind as you develop your plan allows you to improve it. You should set goals (or aims) for each classification to improve its performance. The classifications are general; however, your objectives are explicit. The following are test objectives you could use for every type. (We provide goals you can select when you complete PlanVision’s RFP Goals and Questions tool). Eventually, you will decide how well every merchant will meet your objectives by responding to the inquiries in each category. We will only pay for services on a flat fee basis. All plan providers will be paid straight - no revenue sharing will occur. Plan payments, except for advisory fees, will be paid by the plan members. We are looking for an advisory firm to take on the role of both a 3(21) co-fiduciary and a 3(38) investment manager. Our ideal Investment Policy Statement would be short and sweet. Additionally, we only require that our Investment Committee meet once per year; everything else can be handled by the chosen advisory firm. When enrolling in your retirement plan, you will receive personal assistance to help you make the best choices for your situation. We offer our employees individual retirement and financial planning services to ensure you are on track to reach your goals. Our employees will not be sold any other investment products. We want our record keeper to be a different firm from our investment options and advisor. This way, you can be confident that you are getting unbiased advice and service. Their fee will be presented in a format that is easy to understand so that you know exactly what you are paying for. Our line-up will be almost exclusively low-cost index funds. We will offer Target Date Funds and Lifestrategy Funds. We will offer a range of investment options that including most conventional asset classes with value and growth Conversion Overall options in each asset class and a stable value fund. As we approach the implementation of the new benefits plan, we want to make sure that everyone is as prepared as possible for the change. We will be offering group presentations to all staff members, as well as personal enrollment meetings for those who have questions or need more information. Target all in costs of 0.50% per participant. We also want full fee transparency and all fees will be easily justified. At a minimum we would like our employees to receive periodic personal guidance on their plan. Acknowledgment Letter, Meeting Checklist, Meeting Minutes, and Total Cost Sheet are some of the documents included in this collection. It would help if you double-checked that the language is appropriate for how your plan will function and that it is consistent with your objectives. It is not necessary to use an Investment Policy Statement; however, it is a good idea for virtually every plan sponsor. PlanVision's RFP Goals and Questions resource is an essential tool for your committee in order to compile all relevant information into one, easily accessible online document. Your committee should use this resource to meet for 1-2 hours. After you've entered your plan information, you may evaluate how well each area of plan management is working with a slider evaluation tool in the program. “Are we getting good value from our service providers?” is a key question to ask throughout this process. Then you proceed from one category to the next, selecting arrangement goals and RFP questions. We have a wide range of objectives and questions, but the framework outlines twenty specific inquiries. By using them, you will improve your communication skills. However, this is your plan and if you have different needs in mind, don't worry! You can always select other questions or add your own inquiries to the mix. Take into account that since you have established objectives before receiving any suggestions, it is natural for your assumptions to change. Ideally, the proposal you receive will correspond to your goals, but you may need to reconsider specific arrangements or aspects. After you have completed the RFP Goals and Questions, you will receive a copy of your document as well as a link to your RFP. This connection is ready to use! It has all the necessary data and instructions every caretaker needs in order to respond. You will send this out to the vendors you have chosen to bid on your project. (We are happy to provide personal guidance and assistance to businesses completing this information). The first and second steps are key to continuing to develop your arrangement. Determining your expenses and what you need is crucial. If this does not seem to work, we advise against moving forward. Why put yourself through the hassle if you have no clue what you pay now and what you'll need? Of course, you may luck out and expand your agreement, but contributing time to the front end will help prepare you for the process. Employers that don't lay a solid foundation will most likely be late in conducting an effective arrangement investigation. Once you've completed these two stages, you may continue forward with a solid foundation to improve your strategy. This project will take an estimated 10 days to complete. Before you proceed with any changes to your current arrangement, it's always best to check in with your provider first. You can let them know over the phone that you are considering switching, but we recommend sending a formal letter as well. This way they won't be caught off guard if/when you do switch providers. They may try to talk you out of it or ask for a meeting, but just politely decline and move forward with your plans. Before you discuss your proposal with your supplier, require them to email you a list of their questions. Depending on how you feel about your current supplier, consider letting them respond to your proposal. (You could finish stage 3 before starting stages 1 and 2; however, most plans won’t have any issues that would stop a conversion from happening.) This project will take an estimated 45 days to complete. Assuming you have no transformation issues, you currently need to distinguish merchants for your RFP. This could be the most troublesome aspect of the cycle! You could send it to enlisted speculation counselors; record-keeping firms; banks; insurance agencies; specialists/sellers; or some other firm you run over or are alluded to. You can involve these assets also: www.plansponsor.com has a number of firms but typically for larger employers’ plans; and http://www.investmentadvisorse... is a database with listings of advisory firms that you may sort by state and size in the index. We've added an extra posting of suppliers as an aside. If you obtain a reference from another company, get some details about their expenses arrangement charges if possible. How they react will reveal how savvy they are with expense management techniques. Send this RFP only to firms who you have contacted and clarified your project goals and timeline with. Using the provided script, inquire if they are interested in responding; some may decline, which will save time for everyone involved. If they want to respond, send them the link to your RFP. Some may decline, which will save time for everyone involved. An important thing to note: Your Request for Proposal should be concise with specific questions. We don't recommend using a long and drawn-out RFP. It's not that those details don't matter-- they do. However, it would be best if you made compromises as a smaller firm doing this on your own. Requests for proposal (RFPs) that are long and lack focus will not work. You don't want to be overwhelmed with irrelevant information, so it is better to have a more limited RFP that helps you identify the key characteristics you are looking for in a vendor. After you send your RFP link to up to five companies – including your current provider – allow them 30 days to respond. This should be enough time, as they will need to gather data from various sources to complete the response. As each vendor submits an answer, you will receive a PDF copy of their responses. When all responses have been submitted, you will get an easy-to-read PDF report that lists every question with every seller's answer in the same order throughout the document. This project will take an estimated 3 days to complete. After receiving the feedback, plan for your panel to meet for 1-2 hours to discuss the results. However, each council member should review the feedback before the group meeting. These individual reviews have a different dynamic than the upcoming group discussion and could generate questions or conclusions that may not come up in the social setting. Your individual evaluation should only take 25-30 minutes. Hold your group meeting after you individually review the recommendations. Once you have compared each supplier's accounting page reaction, discuss the data with your team. Did they answer all of your questions? How does their structure compare to your current plan? Did they make a lot of promises without any substance? Was it difficult to understand the total fees from their bid? Does one vendor cost more but offer more value or service to your organization? With these factors in mind, you should be able to choose 2-3 preferred vendors. You should have received your link to the evaluation notes and decision resource by now. This will come in handy at the meeting. The board of trustees keeps all notes and remarks on every cycle and merchant in this archive. During the meeting, somebody will take note of all the important points from your discussion. You could even ask somebody with great secretarial skills to sit in on the meeting specifically for this purpose. Once the committee reaches its final decision, you will receive full documentation detailing all aspects of the process and reasoning behind your selection. This project will take an estimated 2 weeks to complete. This is a significant screening step. You'll get a sense of every vendor's thinking and strategy. This is your strategy. Plan three questions depending on each supplier's response to your RFP, and forward the inquiries to them before the meeting if you like. Here is a sample question for you to consider. You may make up your own with ease. They should respond to each address as soon as possible. Give them another ten minutes to answer the following question: “What value does your contribution hold for our company?” This investigation aims to determine why you haven't given the merchants a chance to sell you their services. Give them an opportunity now. You would never know and learn something new. You may also obtain a sense of the professionals' expert style and methods, allowing you to analyze the research with your company. End your conversation by requesting that they provide references to you within three business days. This project will take an estimated 1 week to complete. Before the presentation, do this. You can address it at the presentation if anything out of the ordinary pops up during these calls. Call two of their customers and have three specific questions, so you're in control of how much time each call takes—around 20 minutes total. Don't ask vague questions like "What are your thoughts on your current vendor?" Your questions should make their clients think harder than usual. Keep in mind that you're looking for both confirming and new positive or negative information that hasn't come up yet. It might be during these calls. This project will take an estimated 1 month to complete. Keep presentations to 55 minutes in length. Tell the moderators what you need to cover, including your time span. We do not see a good reason to be obscure about your goals for your meeting. Have an open mind while watching and look for creative ideas during the show. This is another opportunity for a merchant to put their sales pitch on you; therefore, be ready to listen to them. As a result, you are doing these things because of this. A moderator might establish a positive connection or take a step back. Pose questions throughout the program so you can learn more about it. Get it out there; knowledge is power. Make sure you are clear on a simple aspect of motivating your employees. The advice from the consultant who works with your staff may impact how fast they are paid. It's reasonable for the instructor to wind up discussing additional monetary concerns and ideas with your workers. For example, your financial advisor could suggest different protection-based investment products or periodically encourage your employees to rebalance their portfolios for better performance. Does this type of advice sound good to you? Would it be beneficial for your workers? Be sure to understand and agree with your advisor’s reasoning and direction. Misleading investment advice is everywhere these days. Make sure your team doesn’t get it through your plan. You might want to consider a discussion-style design for merchants to respond to queries. In contrast to individual introductions, this is an out-and-out oddity. It has some advantages and may lead to unforeseen difficulties. The discussion style presentation has another advantage: it would most likely improve clarity for contrasts between the merchants. You may notice that each option you're considering appears to be valuable in its own right, and separate descriptions can cause confusion or vulnerability about the entire benefits of each offer. However, with this discussion approach presentation, it will be simpler to identify the differences between merchants. Tell each moderator that you do not expect anything less than an expert, common conversation. Expect to spend around one hour and a half on this activity. Company C, which employs 13 people, is starting a new retirement plan. The old plan was a Simple IRA that used loaded mutual funds. The new 401k Safe Harbor plan will use Vanguard funds instead. Record keeping for the employers costs around $1,700 annually, and participants will be responsible for an advisory fee of $1,000 annually. On average, participants will pay Vanguard 0.12% annually and an advisory fee of 0.25%. Combined, this totals to around 0.27%. While savings per participant varies, employees are no longer subject to sales loads, and their expense ratios have decreased by 80% to 90%. Keep in mind that this could be tough for some moderators who can't rely on conventional methods like PowerPoint. They should also have extensive knowledge of other industry items and services to respond to ideas brought up by other sellers. From our perspective as an upcoming seller, we would wholeheartedly endorse this approach. Although we can't speak definitively since we haven't participated in this organization ourselves, it has great potential. Innovation is the key to this last idea's success. By conducting finalist introductions via video conference, smaller organizations can save time. This may also give you a larger pool of potential vendors to choose from for your project. This project will take an estimated 3 days to complete. Once you have met with your advisory group and reviewed everyone's initial reactions, survey the notes you took from the meeting. Discuss how each merchant looks at pricing, offers investment opportunities and services, as well as if they align with your goals. There may be additional features or benefits that were not initially considered which could impact your decision making process. You do not need to use a numeric rating system to measure your assessment models. You also don't need an evaluation process to choose the best supplier; simply talk it through and select the merchant and option that works best for your company. After you have narrowed down your choices, it's time to ask more specific questions so you can make your final decision. Go back to your sellers with a list of questions and get their responses so you can finish this process. At this point, finish your Evaluation Notes and Decision resource to document your decision. You will need to show the explanations behind your change. We recommend only 2 to 3 sections that clarify how you have developed your arrangement further and why the new organization is a better choice for your association. Your entire process should be documented. What if, while it's hard to believe, you may still be with your present vendor in the future? This may not be the outcome you wanted, but don't change suppliers because of this effort or because you completed it. If you had the option to confirm that your current supplier is still the finest choice for your business, now YOU know why! You could wind up choosing the lowest-cost retailer for your arrangement. You might discover an organization that charges more yet provides support or an approach that is important to you. Many financial investors are aware of the Morningstar Star Rating framework, which gauges the exhibition of individual shared assets and asset families. However, it appears that there is no method to rate consultants who advise common asset substitutions for defined commitment plans in terms of how well they are presented. (We are not interested in warning firms' cycles; we're interested in their outcomes.) You should, therefore, ask any consultant who promises to monitor and advise you on the best resources for your portfolio to provide evidence of the following: (It could be argued that the charged amount would still have been used as a contribution to their workers' accounts.) If you are paying for a service that is supposed to result in improved outcomes, then shouldn't the company providing that service be transparent about its process and results? Advisors should be required to provide this information and keep track of all fund replacements they have recommended over the years. It's only fair that a firm promoting itself as adding value through monitoring your fund lineup and replacing underperforming funds with better ones reveals its performance. We think companies should post all their results on their website for customers to see. If they are good at what they do and offer value to their customers, there is no reason why they wouldn't want to promote their results. Record keeping includes a variety of tasks related to the bookkeeping process. Despite this, it can be easy to consider retirement plan record keeping as a commodity. It can seem difficult to distinguish from one supplier to another. Cost can easily become the main driver in vendor selection. However, we do not feel that you should consider record keeping as an item. While price is clearly a factor, some record keepers are actually superior. They have developed more efficient cycles that allow them to provide virtually identical records for less money. Your record keeper's level of customer service and attentiveness will have a tremendous impact on the success of your plan. Each organization has their own way of handling customer requests, so it is important to find one that meets your needs. A recordkeeper that is unresponsive and makes frequent mistakes can be a source of ongoing frustration for sponsors and participants alike. Record attendants should be known for providing quality service and handling customer exchanges in a timely and efficient manner. They would also be able to address deadlines for finance, plan testing, annual filings, and other tasks. Although a part of your account manager's productivity (and expenses) will be dependent on the size and complexity of your company, many smaller businesses don't present the same challenges as larger businesses. Their account managers shouldn't have much difficulty in handling them. Of course, there are always exceptions to every rule, but a good account manager should be able to deal with most customers without too much trouble. Finally, companies may choose whether they require a record guardian or TPA as a 3(16) trustee. 3(16) refers to the ERISA code that regulates plan formation requirements. The arrangement support, also known as a manager, ensures that the agreement functions appropriately as the 3(16) guardian. Just like previously mentioned 3(21)s and 3(38)s, businesses can also contract with firms to act as their 3(16) trustee. If a business contracts with a record keeper/TPA for 3(16) services, they should keep in mind that they are still responsible for choosing a qualified fiduciary. Date: Contact at Current Firm, Hi there. We are currently evaluating our current retirement plan specialist companies to see if changing providers would be a good option for our organization. Would you mind answering the following questions so that we can get your thoughts? Thank you. The first step is to call the potential merchants and have a brief discussion with them. Make sure you explain what you are looking for, and determine if they could be a good match. It's perfectly fine to be very upfront about what you want-- there's nothing wrong with that. You can eliminate those companies that just won't work for your plan by using this script: We are currently evaluating our current retirement plan and will seek the services of a professional business. We heard about your company through XXXXXX. We have the RFP ready and a contact that sellers may use to respond to the offer. We might want to get feedback from your company's appropriate individual on whether or not we should send you the proposal. Is it possible for us to conduct this?" Explain how you intend to accomplish your objectives and how the plan will be structured, among other things. Then go through the major aims of your strategy and the process by which it will be carried out. Then inquire if this opportunity is a potential match for their company. For example, you could say: “Is there a possibility your firm would be interested in partnering with us?”What Is an Employer 401(k) Plan?

Getting Started

Getting the Conversation Started

Pursuing a More Suitable Plan

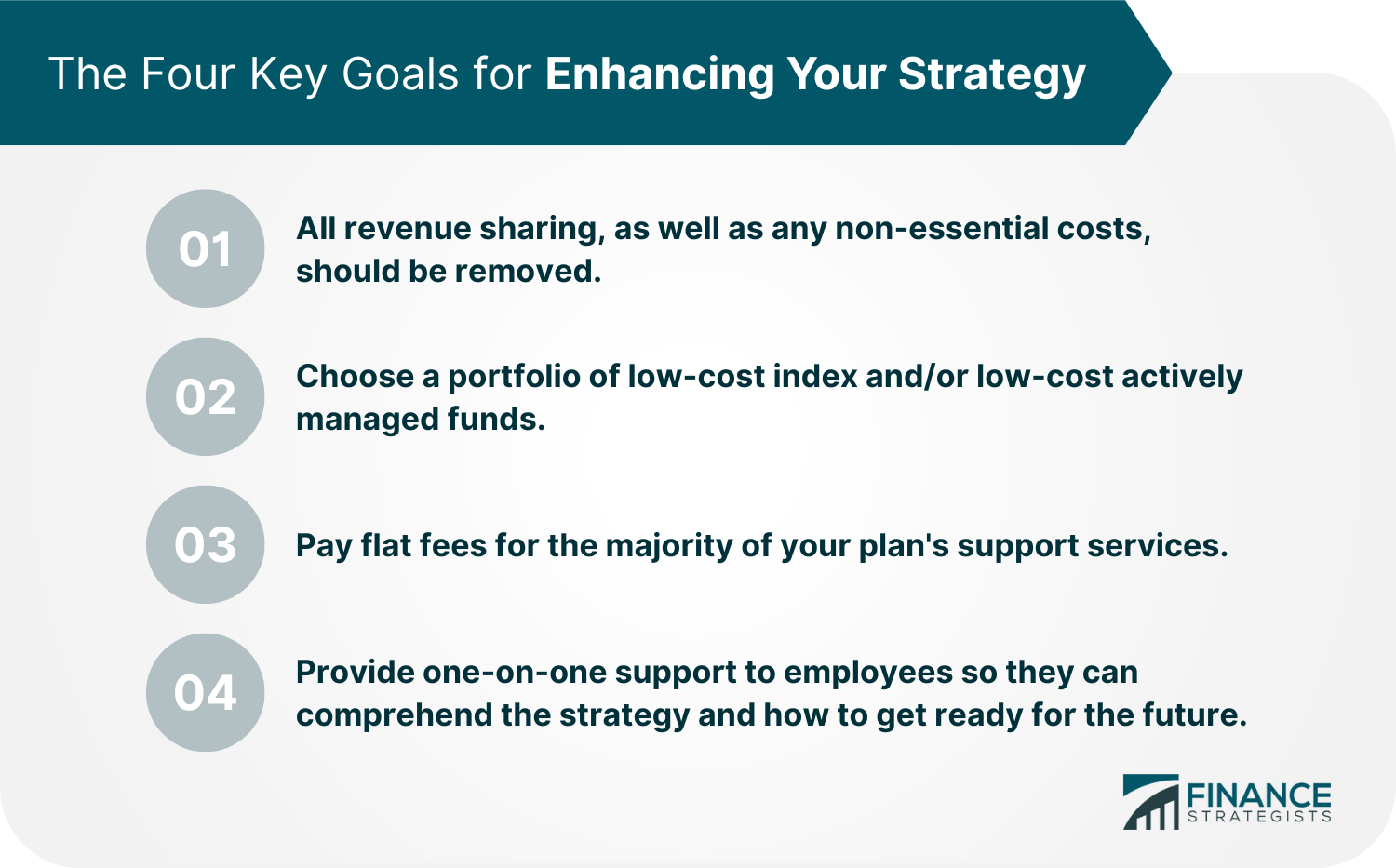

Four Key Goals

Summary

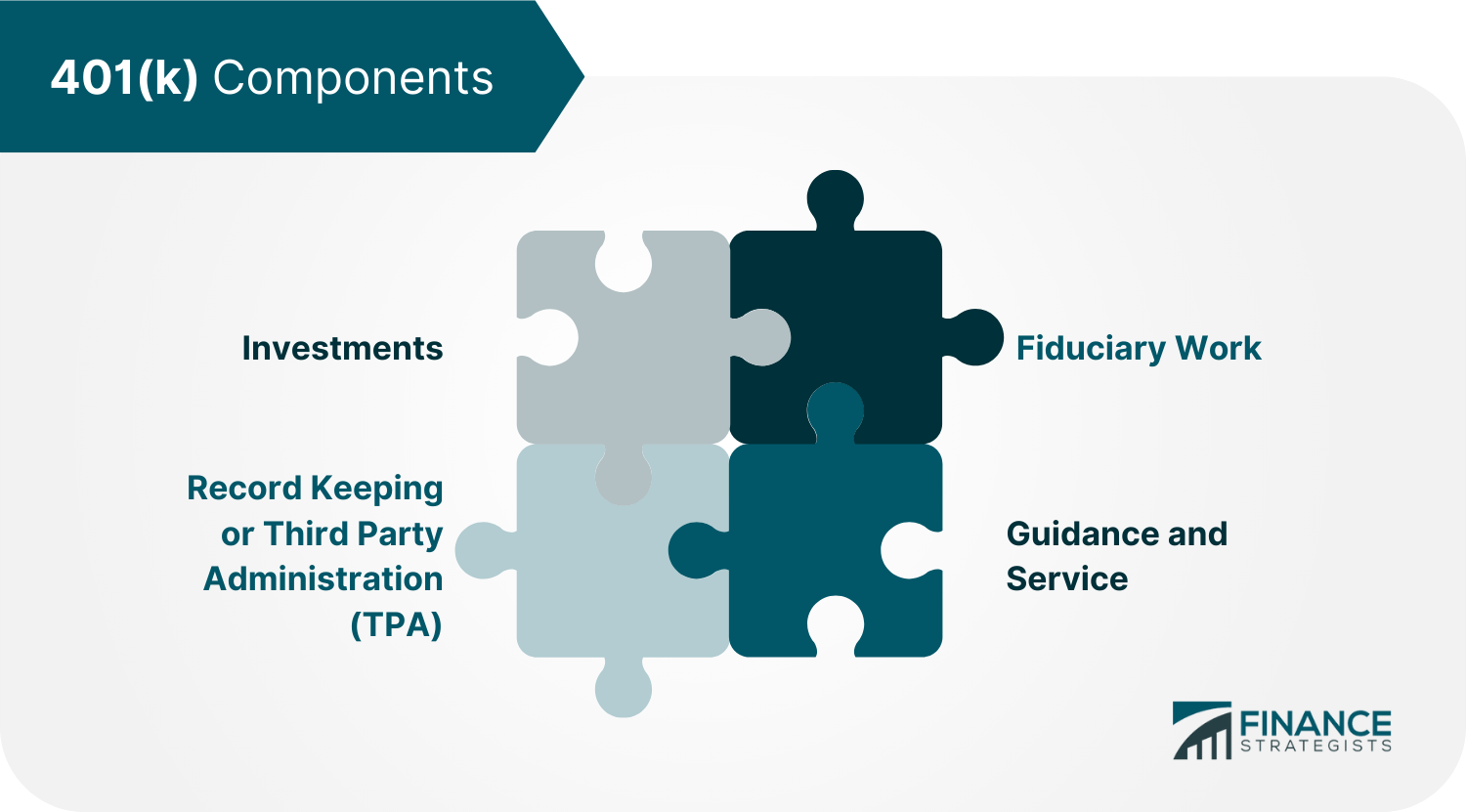

Plan Details

Investments

Company A Case Study

Mutual Funds

Default Investments

Model Portfolios

Target Date Funds

Investments: Your Strategy

Defining Marketing Dollars

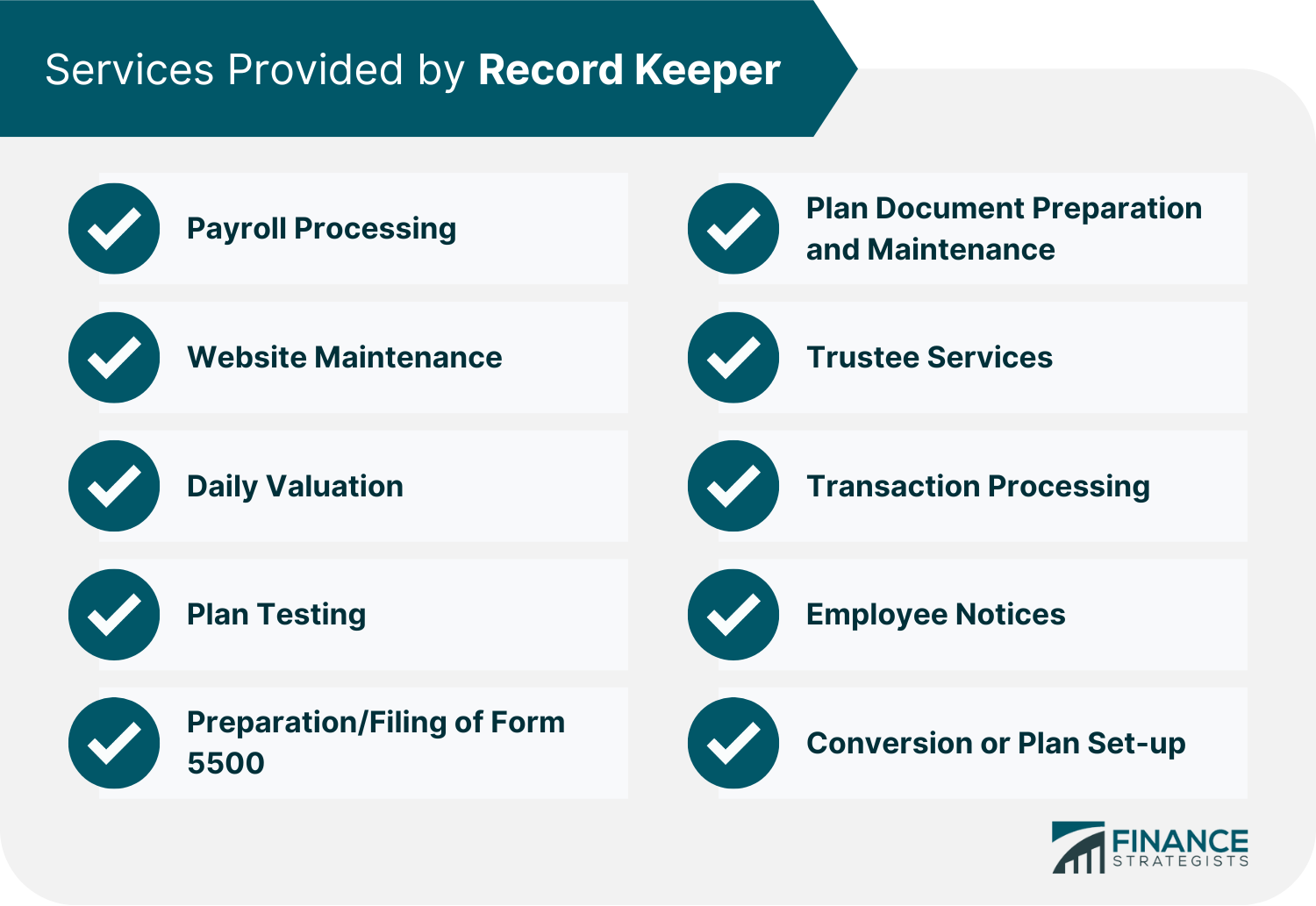

Record Keeping and TPA Work

Services Provided by Record Keeper

Record Keeping: Your Strategy

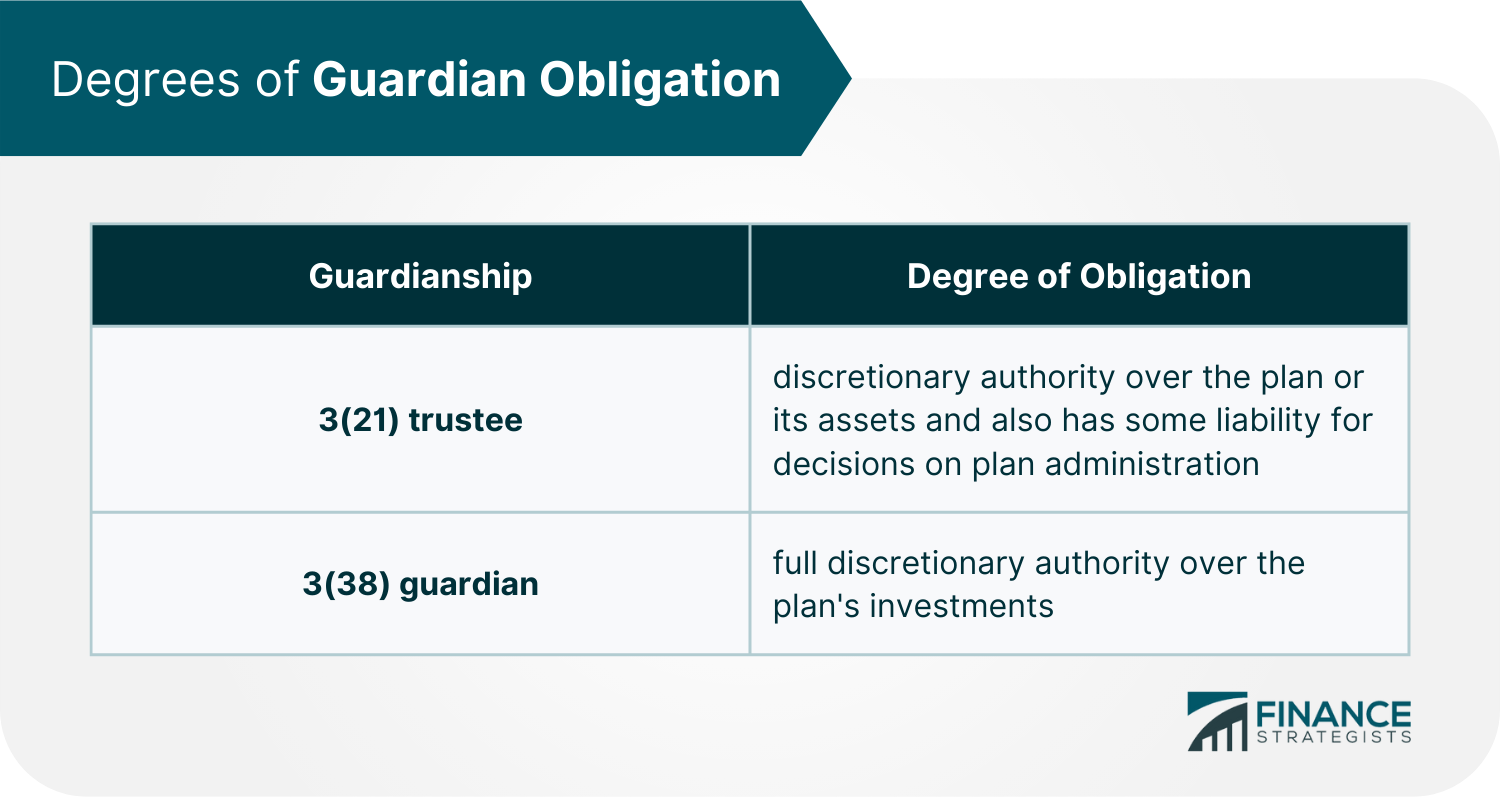

Fiduciary Work

Fiduciary Work: Your Strategy

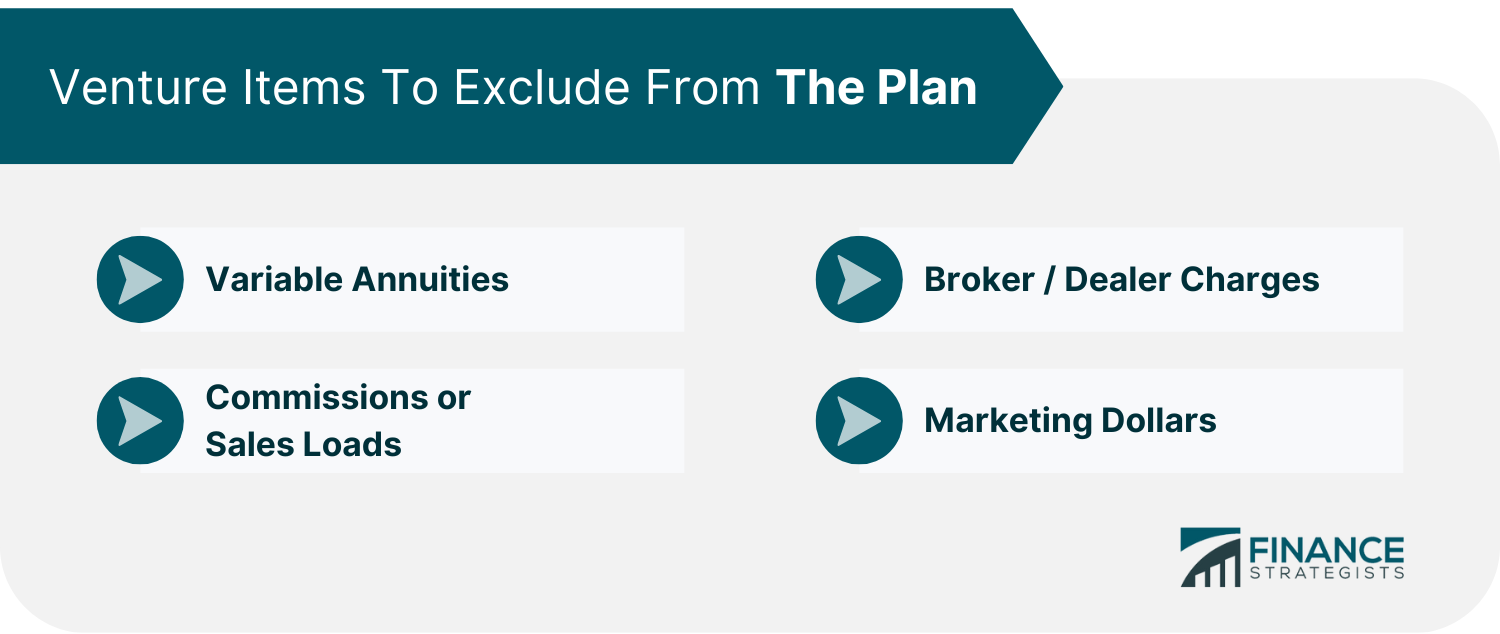

No Dispute of Interest– No Self-Dealing

Guidance and Service

Guidance and Service: Your Strategy

This guidance helps employees understand the basic plan features, review investment options, and explains how to successfully complete their account set-up.

A good enrollment is a great way for employees to appreciate the benefit. However, some employees may be fine enrolling on their own.

Giving workers direction on the more extensive picture can be exceptionally useful. Workers that probably won’t profit from this include:

This is important work and your guide should be compensated fairly for their time, effort, and expertise. However, the advisor should also generate his or her income based upon the time committed to your organization.

Much like the record keeper, they should be able to charge their services on a flat fee basis. Once more, this is the third of our four Key goals for your plan.

Many merchants/vendors and consultants utilize the business-based arrangement as a stage to develop their business. It would help if you kept an eye out for this when negotiating your agreement.

You don't need your workers to be focused on arrangements that are not in their best interest or that will cost the organization more cash over the long haul.

On the one hand, some people argue that it is perfectly fine for employees to choose their own counselors, as long as they trust and want to work with that particular consultant.

On the other hand, others argue that this could potentially impact how the consultant provides guidance to the employees. Ultimately, it is up to you and your boss to decide what is best for your company.

However, if you do allow employees to choose their own counselors, be sure to have a written agreement in place that they will not allow this to happen with their warning firm.

This will help to ensure that the counseling process is not impacted by any personal relationships between employees.

This is an important step in ensuring that your employees receive the best possible coaching and development opportunities.

Including this provision in your service agreement will help to ensure that your employees are receiving coaching that is truly beneficial and supportive.

It will also help to protect your investment in employee development by ensuring that the coach you select is able to provide quality services.

Financial advisors can provide more personalized advice and guidance, and they may be more able to answer specific questions about your financial situation. Usage rates for online resources tend to be lower than for meeting with an advisor in person.

Auto-escalation means that employees' contribution levels are automatically increased over time, typically on an annual basis.

Both auto-enrollment and auto-escalation can help to ensure that employees are saving enough for retirement and that they stay on track to reach their goals.

And with auto-escalation, employees can automatically increase their contributions to their plans on an annual basis. Both of these features can help workers save more for their future.

Enlisted Investment Advisers (RIAs) are dependent upon a guardian standard. An RIA should consistently put the interests of their customer in front of their own advantages.

They may not really be a guardian for your arrangement, assuming you don’t contract with them for this assistance; however, a RIA should consistently act in a judicious way, with practically no irreconcilable situations, on your sake.Summary

The Change

The transformation process could be somewhat uneven, and a few workers may complain loudly, but the consequences of not changing are too severe to ignore.Step-By-Step Process to Improve Your Plan

Starting the Plan Improvement

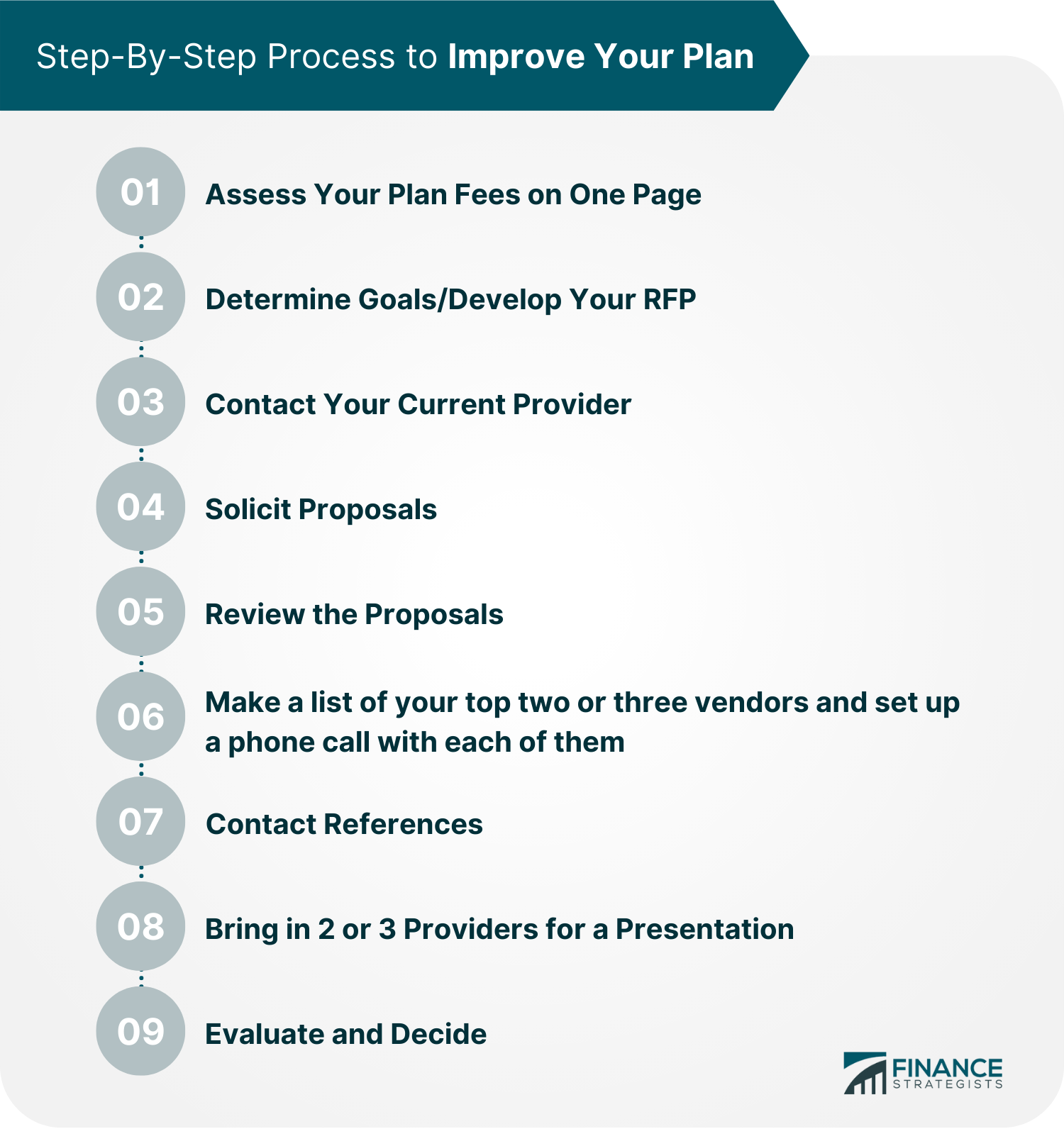

By taking the time to assess these key factors, you can be confident that you are making the best decision for your business.Step 1: Assess Your Plan Fees on One Page

Your new record manager should control access to resources at two different caretakers.Step 2: Determine Goals and Develop Your RFP

Step 3: Contact Your Current Provider

Step 4: Solicit Proposals

Step 5: Review the Proposals

Step 6: Make a list of your top two or three vendors and set up a phone call with each of them for a 25-minute Q&A.

Step 7: Contact References

Step 8: Bring in 2 or 3 Providers for a Presentation

Company C Case Study

Step 9: Evaluate and Decide

Questions to Ask Advisory Firm on Fund Replacement

Then, compare these findings with same 3-, 5-, and 10-year performance figures from an index fund that would have been available during Vanguard's indexed time frame in the same asset class.

Include a short explanation for why these assets were advertised and the fund's performance results for 3, 5, and 10 year periods before and after implementation.

This isn't required if their costs are paid straight by the company.Thoughts on Record Keeping

Appendix B - Supplemental Guides

Letter to Current Firm

Script to Contact Prospective Vendors

Questions for Vendors for the Follow-up Phone Interview

Questions for Client References

401(k) Employers Guide FAQs

An employer 401(k) plan is a retirement savings plan sponsored by an employer. Employers can choose to make contributions to their employees' accounts, and employees can elect to have a portion of their paychecks deducted and deposited into their accounts. Employer 401(k) plans are tax-advantaged, meaning that employees can save for retirement on a pre-tax basis and any employer contributions are also tax-deferred.

There are many benefits to an employer 401(k) plan. Employers can get a tax deduction for their contributions, and employees can save for retirement on a pre-tax basis. Employer 401(k) plans also have the potential to attract and retain good employees.

You'll need to choose a provider for your plan and then follow their instructions for setting up the plan. Employers will need to make sure that they meet the legal requirements for offering a 401(k) plan.

The investment options for an employer 401(k) plan will vary depending on the provider and the plan. Employers should compare providers and plans to find the best investment options for their employees.

No, not all employers offer 401(k) plans. Employers should consider their business needs and goals when deciding whether to offer a 401(k) plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.