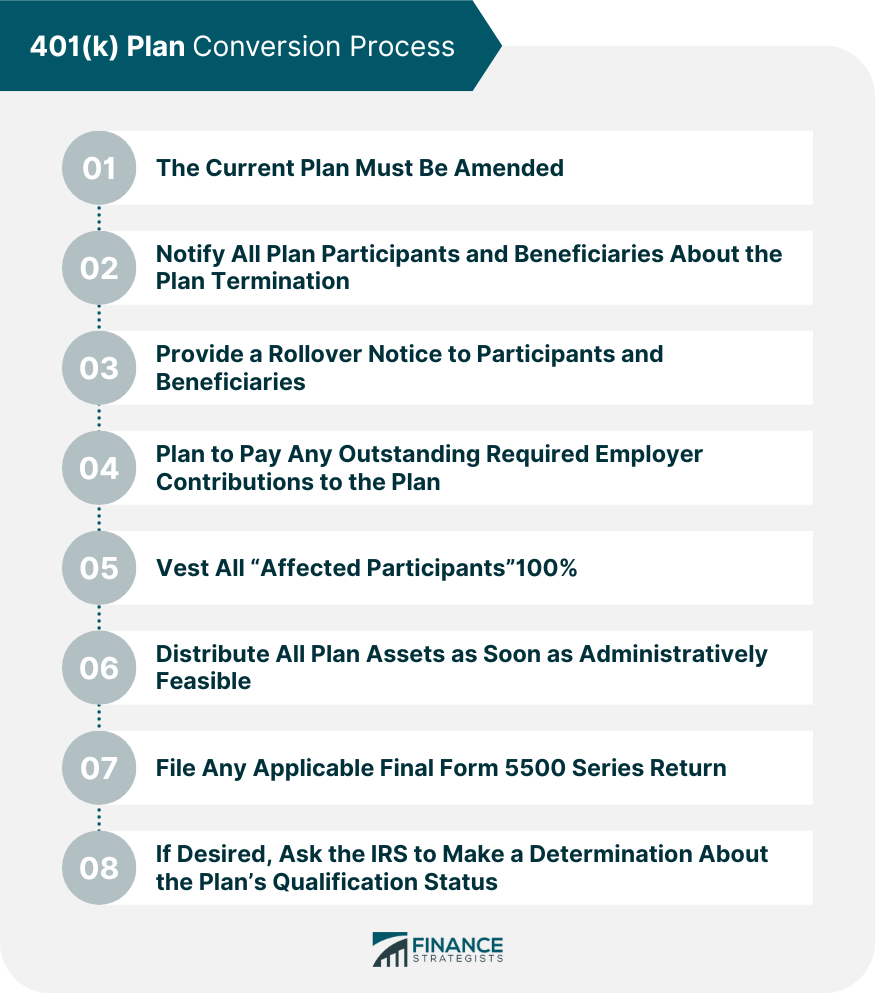

When an employer becomes dissatisfied with the 401(k) plan that it has established for its employees, it has the option of changing to a new (k) provider that may have more streamlined administration processes, better investment choices or lower fees. The IRS considers a 401(k) plan terminated only if: A 401(k) plan that has not distributed its assets as soon as administratively feasible is considered an ongoing plan and must continue to meet the qualification requirements, including amending the plan document for law changes. If you maintain another plan, you may have to transfer employees' elective deferral accounts to the other plan rather than distributing them to employees. The procedure for doing this as mandated by the IRS can be broken down into the following steps: 1. The current plan must be amended to include: 2. Notify all plan participants and beneficiaries about the plan termination 3. Provide a rollover notice to participants and beneficiaries 4. Plan to pay any outstanding required employer contributions to the plan 5. Vest all "affected participants"100% (applies to any employees or former employees with an account balance as of the termination date) 6. Distribute all plan assets as soon as administratively feasible (generally within 12 months) after the plan termination date to participants and beneficiaries 7. File any applicable final Form 5500 series return 8. If desired, ask the IRS to make a determination about the plan's qualification status at termination by filing a determination letter request: You must notify interested parties about your determination application. Check with your plan's financial institution or a retirement plan professional to see what further action is necessary to terminate your plan. You should document all actions taken to terminate the plan. Once the current plan has been discontinued, the employer can create a new document for the new plan, go through the employee onboarding process, request a plan representative to make a presentation to the employees about the features of the new plan and finally transfer the assets. Employers should notify their employees of any plan freeze period that may be necessary during the replacement process. The employer may or may not use the same plan administrator that it used with the previous plan, depending upon the reasons why the employer decided to change plans. If the same administrator is used, then it will be responsible for sending out the notification to all employees that the plan is changing and describe the impact that this may have on all plan participants.

Have questions about 401(k) Plans? Click here.

401(k) Plan Conversion Process FAQs

A 401(k) plan is a retirement plan offered by an employer designed to help employees save for retirement.

Amend the plan to include certain elements, vest the employees 100%, and file any relevent series 5500 forms with the IRS.

With a Roth 401(k), taxes are paid as money is put into the retirement account. With a traditional 401(k), taxes are paid as money is taken out.

Alternatives to 401(k) plans include traditional IRAs, Roth IRAs, pension plans (if your employer offers one), and 403(b) retirement plans for employees of non-profit organizations.

To convert your 401(k) plan, you typically need to contact the administrator of your current plan and request a rollover. Once you have completed the paperwork, the funds will be transferred from your current plan to the new IRA or other investment accounts.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.